FireFly Metals Ltd (ASX:FFM, TSX:FFM, OTC:FFMFF) has delivered another strong batch of drilling results from the Green Bay Copper-Gold Project in Newfoundland and Labrador, Canada, with assays reinforcing the continuity and grade of the project’s high-grade core zone.

The latest results, including 42 metres at 6.1% copper equivalent (CuEq) and 51.5 metres at 4.9% CuEq, will be incorporated into an updated resource model underpinning economic studies for the potential upscaled restart of mining at Green Bay.

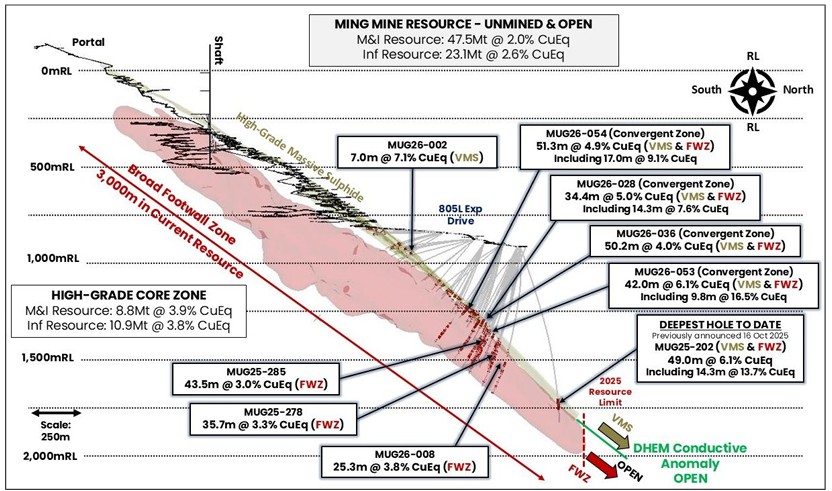

High-grade core strengthens early production case

FireFly’s infill drilling continued to demonstrate broad, high-grade copper-gold mineralisation across the convergent core zone, where upper volcanogenic massive sulphide (VMS) lenses meet the footwall stringer-style copper zone.

Key results from the core zone included 42.0 metres at 6.1% CuEq, including 9.8 metres at 16.5% CuEq, in hole MUG26-053, and 51.5 metres at 4.9% CuEq, including 17.0 metres at 9.1% CuEq, in hole MUG26-054.

Other notable core zone hits included 50.2 metres at 4.0% CuEq and 34.4 metres at 5.0% CuEq, supporting the company’s view that the zone could become an important part of future mine planning.

Isometric view of the Ming Mine 805L Exploration Drive showing the location of drill platforms and drilling reported in this announcement. Assay results greater than 0.5% Cu are shown in red.

Resource upgrade to feed economic studies

The Green Bay resource currently stands at 50.4 million tonnes at 2.0% CuEq in the measured and indicated category, with a further 29.3 million tonnes at 2.5% CuEq inferred. The high-grade core zone contains 8.8 million tonnes at 3.9% CuEq measured and indicated, plus 10.9 million tonnes at 3.8% CuEq inferred.

FireFly’s latest results will be included in a mid-year mineral resource estimate, which will support the preliminary economic assessment and scoping study now expected in July-August 2026.

Managing director Steve Parsons said the results showed “extremely high grades over substantial widths” and demonstrated strong continuity, providing a positive indicator for the upcoming economic studies.

“These are exceptional results with extremely high grades over substantial widths. They also demonstrate the strong continuity of this mineralisation. This is an outstanding combination of grade and width. The continuing of this mineralisation is a very positive indicator for the upcoming economic studies, which will assess the potential development scenarios for Green Bay.

“These results will be included in the economic studies, which are in the process of being completed, enabling us to demonstrate the financial benefits of such a rich core of mineralisation.

“With six rigs drilling underground, as well as regional exploration in progress, we intend to keep growing and upgrading the resource in parallel with economic and technical studies”.

Green Bay growth program continues

Six underground rigs are operating at the Ming Mine, split between resource conversion and step-out drilling, while regional exploration is also advancing. Two surface rigs are testing geophysical anomalies at Green Bay and maiden drilling has started at the Tilt Cove project.

FireFly remains well funded, with about A$219.9 million in cash and liquid investments as of March 31, 2026.

What’s ahead

FireFly’s Near-term work will focus on:

- upgrading inferred resources into the measured and indicated category;

- growing the resource through down-plunge drilling;

- completing the PEA/scoping study;

- advancing permitting and engineering, and

- pursuing new discoveries through underground and surface drilling