LPG/ethane demand from the petrochemical sector is driving US consumption growth. For 2025 overall, petrochemical feedstock demand is expected to grow by around 110,000 b/d, supported by rising petrochemical consumption and higher residential/commercial usage from the winter.

US jet fuel demand is expected to rise further in 2025 compared with 2024 but remain below the pre-pandemic level. Recent data from EIA indicates that during first-half 2025, jet fuel demand increased by nearly 3% compared with first-half 2024.

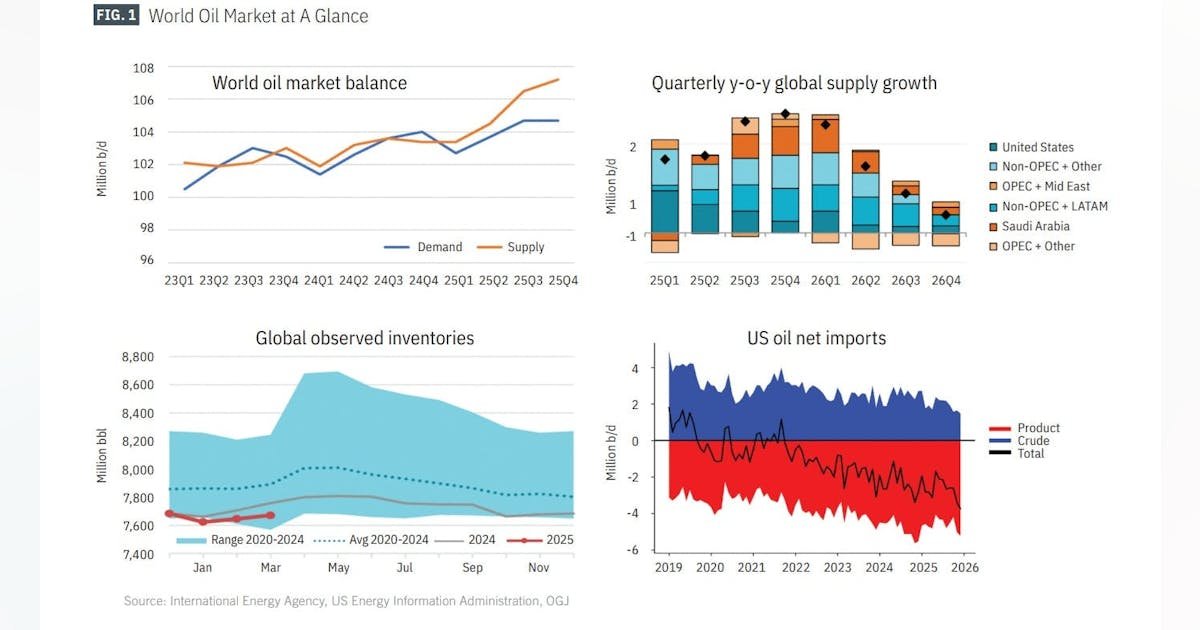

US oil production

US crude oil production growth is expected to slow in 2025 as lower oil prices and heightened trade frictions take a toll on investment and drilling activity.

The downward trend follows a sharp drop in oil prices, with WTI crude briefly falling below $57/bbl in early April—well under the average price needed by US shale producers to profitably drill new wells, according to the Dallas Fed Energy Survey. Rising costs for equipment and steel, exacerbated by the latest wave of US import tariffs, are further pressuring drilling economics.

Nonetheless, US oil output is still on track to reach record levels in 2025, driven by existing projects and a modest rebound from earlier weather-related disruptions. However, growth in LTO production is forecast to decelerate for the third consecutive year, increasing by just 260,000 b/d in 2025 and a further 110,000 b/d in 2026.

US Lower 48 tight oil well costs are under upward pressure from new tariffs, though overall cost increases are expected to be tempered by price declines in key service categories.

Analysis by Wood Mackenzie shows tariffs on consumables—including imported steel, oil country tubular goods (OCTG), cement, and drilling fluids—are driving near-immediate cost increases that will be passed directly to operators. Although operators are experiencing increased costs in certain areas, these will largely be balanced out by deflation in others.

Falling prices for proppant, drilling rig services, and pressure pumping are expected to lower

expenses this year.

As oil prices fluctuate, shale oil producers are seeing deteriorating profit expectations, leading to reduced willingness to increase production. According to the Dallas Fed’s energy survey at the end of the year’s first quarter, producers expect the average breakeven price for new wells this year to be around $65/bbl WTI. At lower price levels, shale producers may adopt a more cautious approach to capital expenditures, which could hinder production growth.

Independent producers are beginning to cut back on 2025 capital spending plans.

Diamondback Energy Inc. has cut its original 2025 capital spending plans by $400 million, or 10% of the previous midpoint estimate, and similarly lowered the target for wells drilled and completed. The company also is dropping three of its 15 rigs.

EOG Resources Inc. has recently taken $200 million out of its 2025 capital spending plan and lowered its production growth guidance. ConocoPhillips also revised its 2025 capital expenditure budget downward, to $12.3-12.6 billion from the previously planned $12.9 billion, due to ongoing economic uncertainty and volatile oil prices. Permian Resources reduced its capital budget by $50 million. Devon and Occidental Petroleum also trimmed spending plans.

Shale wells experience significantly higher initial decline rates compared with conventional wells, which means that maintaining production levels in a basin requires a substantial annual volume of new wells. These replacement volumes depend on the level of drilling activity and the productivity of each well.

Last year, there were notable efficiency improvements in well productivity, including application of AI technology, reduced drilling time, and shortened hydraulic fracturing processes, which offset the effects of lower-than-expected drilling activity. However, for 2025 and 2026, the pace of efficiency gains will likely begin to slow, creating challenges for production growth.

Between January 2024 and April 2025, the number of drilled but uncompleted wells (DUCs) declined to 5,332 from 5,977, reflecting a continued drawdown in the inventory of previously drilled wells, according to EIA’s Drilling Productivity Report.

Meanwhile, the Gulf of Mexico is projected to experience a strong increase in crude oil production in 2025, thanks to major new projects coming online. US offshore production capacity is projected to rise by over 275,000 b/d this year with the startup of four significant projects, including Shell’s newly launched 80,000 b/d Whale field. The initial phase of Beacon Offshore Energy’s 120,000 b/d Shenandoah development is expected to contribute 60,000 b/d to the market.

Additionally, Chevron’s 75,000 b/d Ballymore and LLOG Exploration’s 60,000 b/d Leon/Castile projects will also support a total supply increase of 120,000 b/d in the Gulf this year, followed by another 60,000 b/d next year.

Overall, OGJ forecasts that US crude oil production will average 13.4 million b/d for full-year 2025, a 1.6% rise from the 2024 level.

US natural gas liquids (NGL) production is projected to rise by 2.7% in 2025, reaching a total of 7.13 million b/d. In first-quarter 2025, the composite price of NGL at Mont Belvieu, Tex., increased by 10% from the previous quarter, reaching an average of $8.10/MMbtu. This rise was largely fueled by increases in the prices of ethane and propane.

In late April, China lifted a 125% retaliatory tariff on US ethane imports, which had been imposed earlier that month. With this tariff eliminated, robust growth will continue in US ethane production and exports. According to EIA’s projections, the US will produce 2.9 million b/d of ethane this year and 3.1 million b/d next year, an increase from 2.8 million b/d in 2024.

US refining

US refinery runs increased year over-year during first-quarter 2025, supported by strong consumption of heating fuels due to an unusually cold winter.

Since OPEC+ significantly cut crude production, heavy/sour crude differentials in North America have been relatively narrow, which have adversely affected margin capture.

However, several factors could widen these spreads over the rest of 2025, including increased production from OPEC+, Canadian production ramping up after maintenance, and refining capacity reduction.

In first-half 2025, gross inputs to US oil refineries are projected to average 16.19 million b/d, reflecting a 1.1% decrease compared with the same timeframe in 2024. Crude oil refinery inputs are anticipated to be slightly lower as well, averaging 15.87 million b/d, a decline of 0.33% from first-half 2024. Refinery utilization is estimated to average 89% during first-half 2025, compared with 89.2% in the previous year.

For the entire year of 2025, refinery utilization is expected to average 90.2%, a modest decline from the 90.6% recorded in 2024. Regionally, the West Coast saw utilization rates fall from 80-90% in January and February to below 75% by late March. This decline was primarily driven by outages at PBF Energy’s Torrance and Martinez refineries in California. On the East Coast, utilization began the year at 83% but dropped below 60% in late February and throughout March, ending the quarter at just 59%. This decline was influenced by seasonal spring maintenance and a major turnaround at Phillips 66’s Bayway refinery in Linden, NJ.

Refining margins have experienced considerable pressure in first-quarter 2025. However,

entering the second quarter, refining margins have strengthened significantly, led by improved Los Angeles crack spreads and gasoline margins. Market participants are replenishing gasoline inventories ahead of the summer driving season and restocking diesel supplies depleted by an especially cold winter. Throughput constraints in certain regions may also keep product markets relatively tight, supporting margins.

US refining capacity is estimated to have averaged 18.19 million b/d during first-half 2025, down slightly from 18.36 million b/d over first-half 2024. Full-year 2025 capacity is expected to decrease to 18.09 million b/d from 18.35 million b/d due to announced refinery closures.

Chemical maker LyondellBasell has permanently shuttered its 263,776 b/d Houston refinery in first-quarter 2025. Phillips 66 will shut its large Los Angeles-area oil refinery late in 2025,

citing long-term market uncertainties. This will reduce California’s refining capacity to 1.5 million b/d.

US oil stocks

Since the start of 2025, US commercial crude oil inventories have been consistently below year-ago and 5-year average levels. US commercial crude oil stocks are projected to be about 432 million bbl by the end of June 2025, a decrease from 440 million bbl at the same time last year.

This can be attributed to robust refinery demand, decreased net crude imports, and the replenishment of the Strategic Petroleum Reserve (SPR), all of which have collectively surpassed the modest increase in domestic crude production.

The US SPR has been gradually replenished following significant drawdowns in previous years. The 2025 mid-year volume of SPR crude oil is expected to exceed 400 million bbl, up from 373 million bbl a year earlier. A US House budget proposal seeks over $1.5 billion for SPR replenishment, including $1.32 billion for oil purchases and $218 million for maintenance.

Energy Secretary Chris Wright estimates that refilling the SPR to its maximum capacity will cost $20 billion and take several years.

US gasoline demand and inventories have also remained near last year’s levels. Distillate fuel stocks have been around 13% below the 5-year average so far this year, indicating tightening supply. After reaching a 6-year high in August 2024, US jet fuel stocks in 2025 are projected to decrease due to rising consumption and reduced refinery production following US refinery closures.

US natural gas market

In first-half 2025, the average natural gas spot price at Henry Hub reached around $3.80/MMbtu, a notable increase from the $2.11/MMbtu in the same period last year.

The annual spot price declined from $2.54/MMbtu in 2023 to $2.19/MMbtu in 2024 and is expected to rise to $4/MMbtu in 2025.

The North American natural gas market entered 2025 with heightened volatility, driven initially by a powerful polar vortex that swept down from Canada, triggering a sharp spike in residential and commercial heating and electricity demand across the central and eastern US.

This weather event also caused well freeze-offs, constraining supply and leading to a substantial drawdown in gas storage.

As a result, the Henry Hub spot price surged to a seasonal peak of $7.15/MMbtu on Feb. 19. Since then, milder spring weather has had an impact. Demand has remained stable, with increased US LNG exports driving upward demand, countered by a milder spring weather, which reduced residential and commercial demand and kept the electric power sector’s demand stable. Further, robust dry natural gas production has helped lower prices and facilitate the replenishment of gas storage. These combined factors brought natural gas inventories back to the 5-year average (2020–2024) by end-April. During March and April, total injections into storage reached 331 bcf, well above the 5-year average of 135 bcf

for the same period.

Looking ahead, the market is bracing for potentially warmer-than-normal summer temperatures. The National Oceanic and Atmospheric Administration (NOAA)’s seasonal outlook favors above-average temperatures across much of the US, likely increasing air conditioning demand and electricity generation, reducing storage injection rates. This,

along with continued strong LNG exports, could tighten the market.

In terms of domestic consumption in the US, structural growth is ongoing, especially fueled by the burgeoning data center sector and the rising demands of AI-driven computing. This trend is leading to increased electricity consumption, which in turn boosts the need for gas-fired power generation.

US natural gas consumption averaged 90.5 bcfd in 2024, up 1.2% from a year earlier, according to EIA data. US natural gas consumption in first-half 2025 is estimated to have averaged 93.5 bcfd, up from 91.7 bcfd over the same period a year ago. OGJ forecasts that US annual gas consumption will rise 1% this year, averaging 91.4 bcfd.

On the supply front, the capacity for natural gas pipelines from the Permian basin is expected to expand, allowing producers to increase natural gas deliveries from the region. This enhanced takeaway capacity could elevate prices at the Waha Hub. However, a recent downturn in crude oil prices has tempered expectations for growth in US crude oil production, which may lead to lower associated natural gas production compared with previous forecasts.

The Haynesville region is anticipated to see a rise in production, driven by higher natural gas prices and growing demand from new nearby LNG export projects.

The international demand for US LNG continues to play a vital role. US LNG maintains global competitiveness, providing gas to Europe, supported by reduced Russian pipeline supplies and depleted European storage following a severe winter.

Notably, Canada’s LNG Canada terminal is set to begin operations in mid-2025, offering Pacific basin access and reducing its reliance on the US market.

Two US LNG major projects—the Plaquemines LNG plant in Louisiana and the expanded Corpus Christi plant—have significantly increased export levels. Early data from Plaquemines LNG shows production and exports exceeding prior expectations. Two additional projects, Golden Pass and Plaquemines LNG Phase 2, are slated to come online over the next 2 years, further expanding capacity. As a result, US LNG exports are projected to grow significantly—by 22% in 2025 and by an additional 10% in 2026.

Pipeline exports are also expected to grow, with volumes rising 8% in 2025 and 7% in 2026. Taken together, total US natural gas exports are forecast to increase by 3.4 bcfd in 2025 and by 2.1 bcfd in 2026.