Based solely on performance, Wall Street has been thrilled to have President Donald Trump in the White House. During Trump’s first, non-consecutive term, the mature-stock-driven Dow Jones Industrial Average (^DJI 0.56%), benchmark S&P 500 (^GSPC 0.11%), and tech-stock-inspired Nasdaq Composite (^IXIC +0.35%) rallied 57%, 70%, and 142%, respectively.

While these major indexes have risen under most presidents since the late 1890s, the annualized returns under Trump are among the best.

President Trump delivering remarks. Image source: Official White House Photo by Daniel Torok.

But this doesn’t mean the stock market has moved from Point A to B in a straight line, or that this Trump bull market can last indefinitely. Headwinds are mounting on Wall Street, with one, in particular, standing out as particularly troublesome for a historically pricey stock market.

Thanks to the president’s own actions, the Trump bull market appears set to end this year at the Federal Reserve’s hand.

A flurry of catalysts has sparked the Trump bull market rally

Before digging into the details of how this bull market ends, we first have to understand what made equities fly in the first place.

To begin with, investors can’t get enough of the artificial intelligence (AI) revolution. The arrival of AI is on par with the advent and proliferation of the internet three decades ago, in terms of what it can do for corporate America. Empowering software and systems with the tools to make split-second decisions without human oversight is an addressable market that can top $15 trillion by 2030, according to PwC analysts.

However, AI isn’t the only trend that’s piquing investors’ interest. The advent of quantum computing, the rise of the space industry, and ongoing stock-split euphoria are all playing roles in sending the Dow, S&P 500, and Nasdaq Composite to new heights.

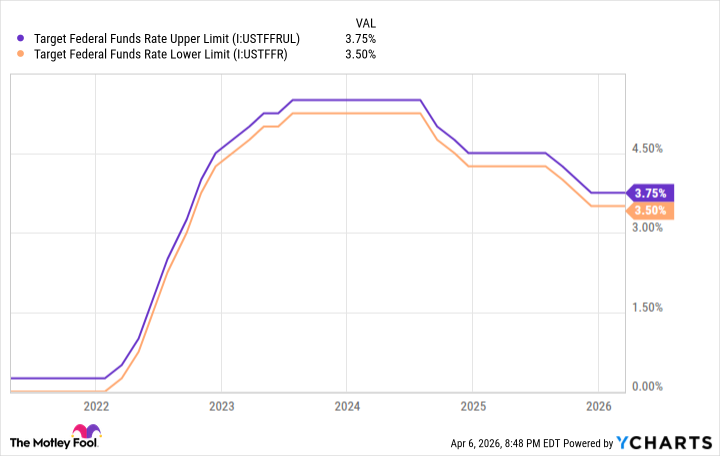

Target Federal Funds Rate Upper Limit data by YCharts.

Investors have also been excited about the Federal Reserve’s rate-easing cycle. Since September 2024, the Federal Open Market Committee (FOMC) — the 12-person body, including Fed Chair Jerome Powell, responsible for setting the nation’s monetary policy — has lowered the federal funds target rate six times. Lower lending rates make it more attractive to build AI data centers and spend aggressively on innovation.

But President Trump’s fingerprints are on this rally, too. While the rise of AI and interest rate cuts have nothing to do with Trump, the president’s signing of the Tax Cuts and Jobs Act (TCJA) into law in December 2017 has had a positive impact on the stock market.

The TCJA permanently lowered the peak marginal corporate income tax rate from 35% to 21% — the lowest level since 1939. Businesses retaining more of their earnings have led to a significant increase in share buyback activity among S&P 500 companies. Share repurchases can increase earnings per share for companies with steady or growing net income.

Fed Chair Jerome Powell speaking with President Trump. Image source: Official White House Photo by Daniel Torok.

One decision by President Trump can upend Wall Street’s bull market

While plenty has gone right for the stock market, one headwind, by Trump’s own doing, appears insurmountable.

On Feb. 28, at Trump’s command, U.S. military forces, along with Israel, began military attacks against Iran. Shortly after these military operations commenced, Iran virtually closed the Strait of Hormuz to oil exports. Approximately 20 million barrels of petroleum liquids, equating to 20% of the world’s demand, pass through the Strait of Hormuz daily.

While Iran partially reopened the Strait of Hormuz on April 5, we’re still talking about the largest energy supply disruption in history. This energy supply chain monkey wrench has sent crude oil prices soaring.

Although the most immediate impact of higher crude oil prices is sticker shock at the fuel pump, there are bigger issues at hand. Namely, the prevailing U.S. inflation rate and the Federal Reserve’s monetary policy.

As of April 6, the Federal Reserve Bank of Cleveland’s Inflation Nowcasting tool was projecting an 85-basis-point increase in the trailing 12-month (TTM) inflation rate in March from February (3.25% from 2.40%). The TTM inflation rate for April is estimated to climb 13 basis points to 3.38%.

A nearly one-percentage-point jump in TTM U.S. inflation over two months could halt the Fed’s rate-easing cycle in its tracks. Even more worrisome, it may encourage the FOMC to shift its strategy entirely and point to rate hikes before the end of this year. Keep in mind that this rapid uptick in inflation comes at a time when the price stickiness of Donald Trump’s tariffs is still being felt in the goods sector.

S&P 500 Shiller PE Ratio hits 2nd highest level in history 🚨 The highest was the Dot Com Bubble 🤯 pic.twitter.com/Lx634H7xKa

— Barchart (@Barchart) December 28, 2025

Normally, a monetary policy about-face by the nation’s central bank wouldn’t be devastating for the stock market. But it’s not every day that the stock market enters the year at its second-priciest valuation since January 1871. The few times that the S&P 500’s Shiller Price-to-Earnings Ratio has surpassed 40 throughout history have been followed by peak-to-trough declines of 49% (the dot-com bubble) and 25% (the 2022 bear market) for the benchmark index.

Though the FOMC tends to be reactive to economic data rather than proactive in its monetary policy decisions, President Trump’s actions in Iran have kick-started a domino effect that seems destined to culminate in the Fed raising interest rates before the end of 2026. Higher borrowing costs would effectively crush a historically expensive stock market that’s been counting on rate cuts, not hikes.

Even if the Iran war wraps up in the next couple of weeks, the inflationary effects of this conflict will linger for several quarters to come. It’s a worst-case scenario for the Trump bull market.