Tradingkey – On June 4, Israel and Lebanon officially reached a ceasefire agreement on Thursday. Coupled with positive signals from Trump that U.S.-Iran negotiations could see progress this weekend, the geopolitical risk premium previously accumulated in the crude oil market was rapidly priced out, leading to a significant correction in oil prices.

According to media reports citing U.S. officials, despite recent exchanges of fire between the two sides, President Trump has clearly stated his reluctance to restart an all-out war with Iran. Trump privately disclosed to aides that the ceasefire agreement with Iran remains in effect, and he would only consider terminating the ceasefire and taking large-scale military action in the extreme event that Iran causes the death of U.S. military personnel.

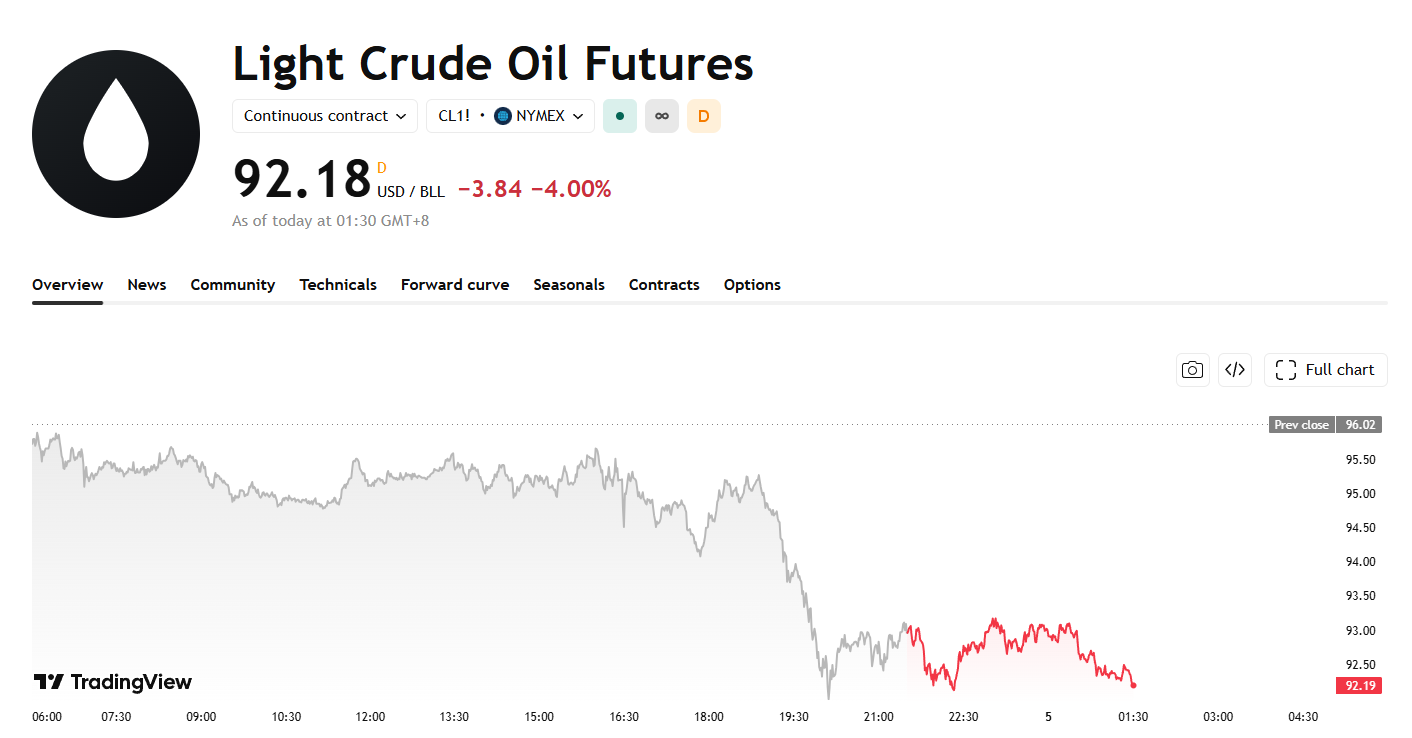

Affected by this, WTI crude oil futures fell 4% to $92.18, while Brent crude oil futures dropped 3.23% to $94.65.

[Source: TradingView]

It should be noted that the current ceasefire agreement is very fragile. Hezbollah’s Naim Qassem warned that if Israel continues its attacks on Lebanon, northern Israel will continue to face security threats.

Furthermore, Iran has deeply linked a comprehensive U.S.-Iran agreement with the Israel-Lebanon ceasefire. Although relevant conditions are progressing, they have not yet been fully met. Analysts say the market has priced in diplomatic progress too optimistically, and oil price trends face two-way volatility risks.

In addition, U.S. political pressure has become a major reason for Trump’s reluctance to expand the conflict. The House of Representatives passed a resolution on Wednesday requiring Trump to withdraw U.S. troops or seek congressional approval to continue the conflict. The resolution still needs to pass the Senate and will almost certainly be vetoed by Trump.

If U.S.-Iran negotiations can indeed achieve a breakthrough, the full opening of the Strait of Hormuz will increase crude oil supply, driving oil prices further down; if the ceasefire agreement collapses or negotiations reach an impasse, the geopolitical risk premium will quickly return, and oil prices may surge once again.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.