Gold prices remain under pressure after a sharp correction this month, but RBC Capital Markets believes the sell-off is creating an attractive longer-term buying opportunity.

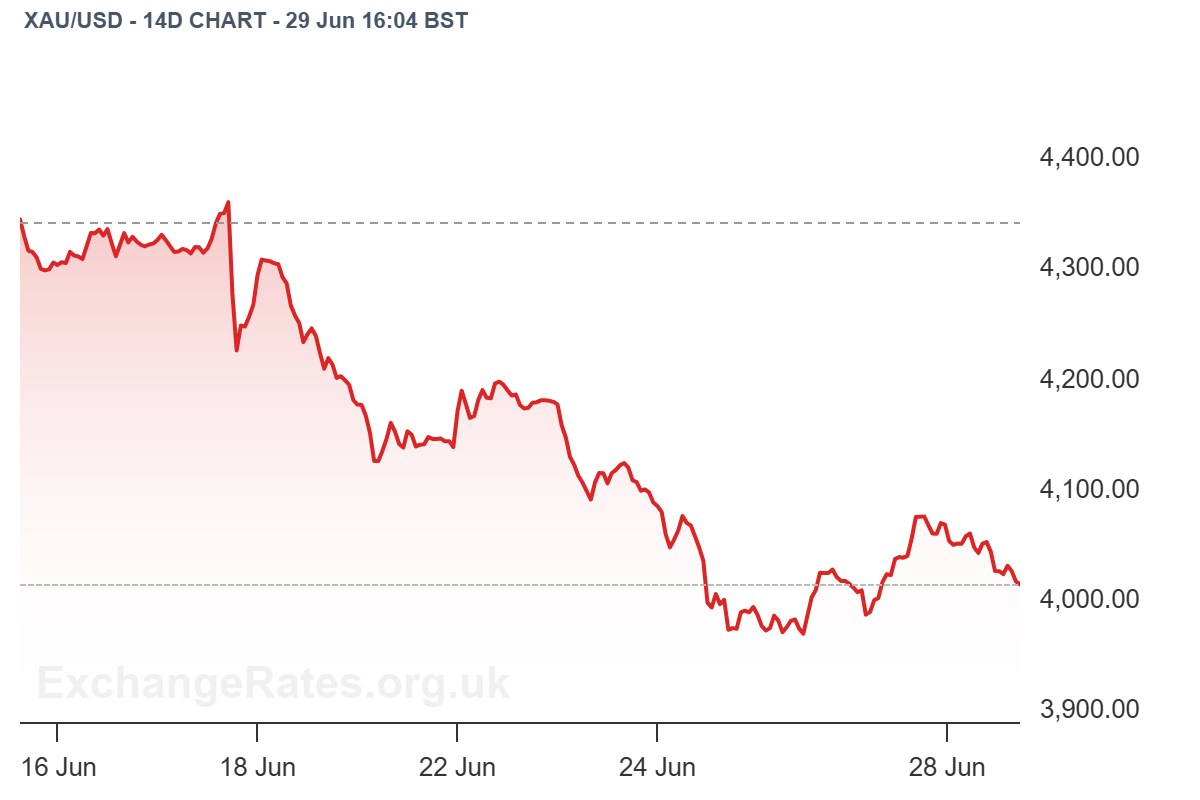

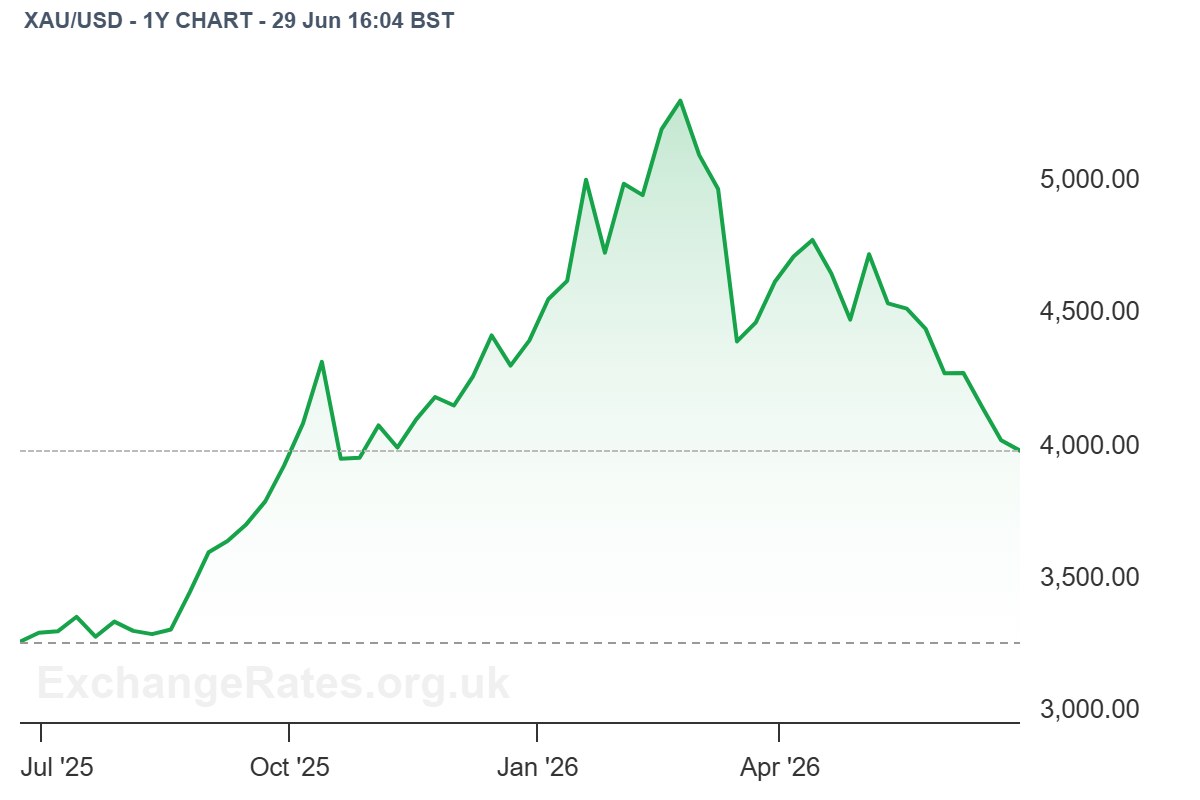

Gold (XAU/USD) traded near $4,028 on Monday, down almost 11% in June after falling from a monthly high above $4,540. The metal has now retreated by more than 25% from January’s record peak near $5,600.

RBC says higher US interest rates and a stronger Dollar have reduced gold’s appeal in the short term, as investors reassess expectations for Federal Reserve policy.

However, the bank believes the longer-term investment case for gold remains intact.

“We think that our low scenario is a mostly firm floor for gold.”

RBC argues that prices around $4,000 per ounce are likely to attract fresh buying interest.

“We think at and below the $4000/oz level, there may be incremental interest.”

While higher yields and Dollar strength may continue to cap gains in the near term, RBC says the structural drivers behind the long-running “debasement trade” remain firmly in place.

“The broader thematic underpinnings of the debasement trade are intact.”

The bank believes growing government debt burdens and long-term concerns over currency debasement should continue supporting gold prices once current headwinds begin to ease.