As European markets experience a positive shift, with the STOXX Europe 600 Index gaining 3.00% amid hopes of geopolitical de-escalation, investors are increasingly focused on growth opportunities within the region. In this context, companies with high insider ownership and robust earnings potential stand out as attractive prospects, especially as they navigate the current economic landscape marked by inflation concerns and revised growth forecasts.

Top 10 Growth Companies With High Insider Ownership In Europe

Let’s dive into some prime choices out of the screener.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Pharma Mar, S.A. is a biopharmaceutical company engaged in the research, development, production, and commercialization of bio-active principles for oncology across multiple regions including Europe and the United States, with a market cap of approximately €1.75 billion.

Operations: The company generates revenue primarily from its oncology segment, amounting to €221.93 million.

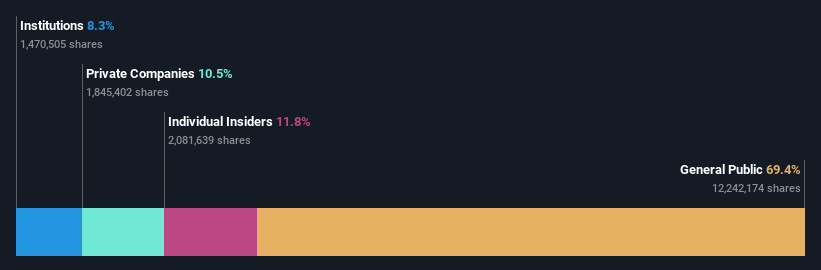

Insider Ownership: 12%

Earnings Growth Forecast: 31.7% p.a.

Pharma Mar demonstrates strong growth potential with expected annual earnings growth of 31.7%, surpassing the Spanish market average. The company’s revenue is forecast to grow at 17.6% per year, and it trades significantly below its estimated fair value, suggesting potential undervaluation. Recent approvals for ZEPZELCA in Australia and Singapore enhance its oncology portfolio, while a strategic AI collaboration aims to expedite drug discovery processes, bolstering Pharma Mar’s innovative edge in cancer treatment development.

BME:PHM Ownership Breakdown as at May 2026

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Holcim AG, with a market cap of CHF40.84 billion, is a company that offers building materials and solutions across Europe, Latin America, and Asia, Middle East, and Africa through its subsidiaries.

Operations: Holcim’s revenue is primarily derived from its Building Materials segment, which accounts for CHF11.56 billion, and its Building Solutions segment, contributing CHF5.85 billion.

Insider Ownership: 10.2%

Earnings Growth Forecast: 25.7% p.a.

Holcim’s strategic alliances, particularly with SaltX Technology, highlight its commitment to innovation in sustainable cement production. The collaboration aims to develop a fully electrified clinker manufacturing process, marking a significant step toward fossil-free cement. Despite recent dividend decreases and slower revenue growth forecasts of 5.5% per year compared to the broader market, Holcim’s earnings are expected to grow significantly at 25.7% annually, indicating strong potential for future profitability amidst industry challenges.

SWX:HOLN Ownership Breakdown as at May 2026

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Straumann Holding AG offers tooth replacement and orthodontic solutions across various countries including Switzerland, the United States, and China, with a market cap of CHF14.33 billion.

Operations: The company’s revenue segments are comprised of Operations at CHF1.34 billion, Sales Asia Pacific (APAC) at CHF630.17 million, Sales North America (NAM) at CHF753.93 million, Sales Latin America (LATAM) at CHF309.11 million, and Sales Europe, Middle East and Africa (EMEA) at CHF1.11 billion.

Insider Ownership: 32.3%

Earnings Growth Forecast: 16% p.a.

Straumann Holding is poised for growth with earnings forecasted to rise 16.03% annually, outpacing the Swiss market’s 10.9%. Revenue is expected to grow at 8.5% per year, exceeding the market average but below high-growth benchmarks. Trading at a significant discount to estimated fair value enhances its investment appeal, though recent board changes may impact strategic direction. The company’s return on equity is projected at a robust 22.2% in three years, indicating strong operational efficiency prospects.

SWX:STMN Earnings and Revenue Growth as at May 2026

Next Steps

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include BME:PHM SWX:HOLN and SWX:STMN.