In 2026, the global memory chip industry is undergoing an epic reassessment of value. Samsung Electronics’ market capitalization has surpassed $1 trillion; SK hynix’s share price has surged nearly 200% year-to-date; Micron Technology’s stock has repeatedly hit all-time highs; and SanDisk has rewritten semiconductor industry history with a cumulative 12-month gain exceeding 3,000%. Fueled by AI-driven demand, this memory rally has propelled South Korea’s KOSPI index from 4,300 to above 8,000 in less than six months—an increase of over 85%, outperforming all major global equity indices.

Yet beneath the euphoria, skepticism persists. From panic selling triggered by Google’s TurboQuant algorithm and unprecedented concentration risk in South Korean equities, to seasoned industry veterans issuing stern warnings that ‘a leopard cannot change its spots,’ markets are now embroiled in a heated debate over whether this surge represents ‘structural transformation’ or merely another turn of the ‘cyclical wheel.’

Soaring Share Prices of Memory Companies Amid the AI Boom

Soaring Share Prices of Memory Companies Amid the AI Boom

Samsung Electronics: Reaching the $1 Trillion Market Cap Milestone

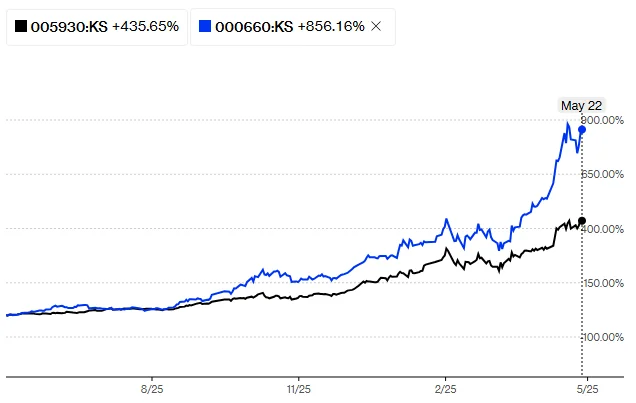

On May 6, 2026, Samsung Electronics’ share price rose as much as nearly 16% intraday, reaching a record high of KRW 270,000 per share. It closed the day up 14.41%, pushing its market capitalization past the $1 trillion mark—making it the second Asian tech company after Taiwan Semiconductor to cross this threshold.

This was only the beginning. On May 21, Samsung Electronics closed at KRW 299,500 per share, setting a new all-time high and surpassing the $1 trillion market cap—again becoming the second Asian tech firm after Taiwan Semiconductor to achieve this milestone. On the same day, buoyed by news that a union strike had been postponed, its shares briefly broke through the KRW 300,000 mark during intraday trading, peaking at KRW 300,500 and marking yet another historic milestone. By May 22, Samsung Electronics’ market cap had exceeded KRW 1,700 trillion, with its year-to-date share price gain reaching 128%.

The primary driver behind Samsung’s stock surge is the explosive growth of its semiconductor business. According to its Q1 FY2026 earnings report, surging memory chip prices and booming AI computing demand propelled operating profit to KRW 57.2 trillion on revenue of KRW 133.9 trillion—already exceeding its full-year 2025 operating profit forecast of KRW 43.6 trillion.

Multiple international investment banks have raised their target prices: Nomura Securities issued the most optimistic target of KRW 590,000—nearly doubling the current price; Korea Investment & Securities raised its target to KRW 570,000, citing structural supply shortages in memory chips; Shinhan Securities revised its target upward to KRW 550,000; NH Investment & Securities set a target of KRW 490,000; and both Mirae Asset Securities and JPMorgan raised theirs to KRW 480,000.

SK hynix: Solidifying Its Dominance in HBM

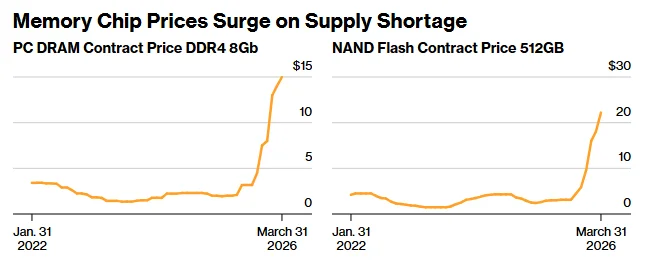

SK Hynix has seen an even more astonishing surge in its share price this year. Data shows that its stock has risen by 187% year-to-date, with the current share price at KRW 1,941,000. As NVIDIA’s primary supplier of HBM chips, SK Hynix holds an unshakable position in the AI memory market. KB Securities recently forecasted a 194% year-over-year increase in DRAM prices and a 244% rise in NAND prices by 2026, leading it to raise its operating profit forecasts for SK Hynix to KRW 277 trillion for 2026 and KRW 428 trillion for 2027—10.2% and 25.1% above consensus estimates, respectively.

Nomura Securities has set a target price of KRW 4 million for SK Hynix, implying more than double the upside potential from the current level. Macquarie, citing ‘worsening memory shortages,’ raised its target price by 61% to KRW 2.9 million, expecting the shortage to persist beyond 2027 and anticipating a significant spike in HBM prices.

Micron (MU.US) and SanDisk (SNDK.US): The Twin Stars of U.S. Memory Stocks

Across the Pacific, U.S. memory chip giants are also writing their own wealth legends. Micron Technology’s share price hit a record high for the seventh consecutive trading day on May 11, 2026; although it has since pulled back slightly to USD 751, it remains up over 160% year-to-date, with a market capitalization approaching USD 850 billion. Citi sharply raised its target price from USD 425 to USD 840, citing expectations of a 200% year-over-year surge in DRAM prices in 2026 and further increases in HBM prices in 2027.

Even more astonishing is SanDisk. After surging 580% in 2025, SanDisk has soared another approximately 523% so far in 2026, resulting in a cumulative 12-month gain exceeding 3,800%. Its latest earnings report showed quarterly revenue of USD 5.95 billion, up 251% year-over-year, with a staggering gross margin of 78.4%. Bullish analysts have even called for a target price of USD 3,000, implying nearly double the upside from the current price of USD 1,479. Citi also significantly raised its target price for SanDisk to USD 2,025.

“Beyond the Cycle” or “The Cycle Is Just Delayed”?

Bulls’ Core Thesis: Structural Transformation

The core argument underpinning the bull case for memory stocks is clear: AI has fundamentally rewritten the operating dynamics of the memory industry. This thesis rests on three pillars:

First, structural shortages in HBM. In an interview, Micron CEO Sanjay Mehrotra explicitly warned that the global memory chip shortage could persist beyond 2026, as AI-driven demand continues to vastly outpace the industry’s capacity expansion. He emphasized that even though new wafer fabs are being actively built, the current supply-demand imbalance represents a long-term structural issue rather than a traditional cyclical fluctuation, with meaningful large-scale new capacity unlikely to come online before 2028.

Second, the irreversible shift of capacity toward HBM. In terms of bit volume, HBM still accounts for only single-digit percentages of the total DRAM market, leaving substantial room for increased penetration. TrendForce forecasts HBM shipments will exceed 30 billion gigabits (Gb) in 2026. UBS Group has revised its 2026 HBM end-market bit demand upward from 31.5 billion Gb to 32.9 billion Gb (an 88% year-over-year increase) and significantly raised its 2027 forecast to 58 billion Gb (a 76% year-over-year increase). Analysts project that by the end of 2026, as much as 70% of globally produced memory chips will be consumed by data centers, and by 2027, global HBM capacity will meet only about 60% of total market demand.

Third, industry structure is being reconfigured. An increasing number of manufacturers are shifting their focus toward AI-specific memory products. Micron Technology has already begun scaling back its consumer-grade memory business, reallocating resources to the more profitable enterprise market. UBS Group forecasts that by 2027, Samsung will rival SK Hynix in HBM bit shipments, with each capturing approximately 40% of the market share. This signals a shift in the industry from ‘scale-driven cyclical competition’ to ‘technology-driven value competition.’

Warnings from Bears and the Cautious Camp

However, not everyone is convinced. A growing number of market observers have started issuing warnings. The most representative comment came from William de Gale, portfolio manager at BlueBox Asset Management. He noted that the industry tends to experience ‘huge swings’ and added, ‘In the long run, it’s a rather terrible industry. I suspect that every time people claim the memory cycle is over and that the memory sector has become a long-term value-creation industry, the same pattern holds true—right before everything goes terribly wrong.’

Andrew Lapping, Chief Investment Officer at Ranmore Fund Management, offered a cautionary African proverb: ‘A leopard rarely changes its spots.’ He emphasized that investors must exercise caution when investing in an industry ‘historically characterized by mediocre returns on capital but currently promising exceptionally high future returns.’

These warnings are not unfounded. During the previous memory chip price upcycle, Samsung Semiconductor and SK Hynix aggressively expanded capacity, only to suffer severe losses in 2023 when demand receded and prices fell below cost. Whether history will repeat itself remains the biggest unanswered question in today’s market.

Notably, funds managed by hedge fund titan Paul Tudor Jones have established bearish put option positions on Micron—a signal that stands out starkly amid the prevailing bullish sentiment. The market interprets this move as a top macro trader preparing for a scenario of extreme downside.

Rise of ‘Affordable AI’ Fuels Concerns Over Compute Oversupply

On March 24, 2026, Google Research published an article introducing TurboQuant, a vector quantization compression algorithm, claiming it reduces critical memory usage during large model inference to one-sixth of the original—without sacrificing accuracy—and delivers up to an 8x performance improvement.

Following the announcement, global memory chip giants collectively lost over $90 billion (approximately RMB 620 billion) in market capitalization within a single day. SK Hynix’s share price dropped 6.23%, erasing roughly $29.38 billion in market value; Samsung Electronics fell 4.71%, losing about $38.45 billion; Micron declined 3.4%, while SanDisk一度 plunged as much as 6.5%.

The Comfort of Jevons’ Paradox?

However, the market quickly calmed down. Several foreign investment banks pointed out that TurboQuant only affects the KV cache during the inference phase, whereas the strong demand for HBM stems from weight storage and gradient computation during the training phase, which remains unaffected; NAND Flash is not involved at all in long-term storage of underlying data.

More importantly, there is the logic of the ‘Jevons Paradox’: when technological efficiency reduces memory requirements per unit of compute, the significant drop in inference costs lowers the barrier to AI deployment, thereby stimulating much larger aggregate compute demand and expanding—rather than shrinking—the memory market size.

However, Deutsche Bank cautioned investors in its report to ‘remain prepared for the ongoing disruption caused by artificial intelligence,’ citing TurboQuant as a prime example: its release led to a sharp decline in the share price of the largest memory supplier. Although it remains ‘to be seen’ whether this technology will trigger a structural shift in demand, it has exposed a deeper risk: in an era of rapid AI iteration, any breakthrough in software-level efficiency could undermine assumptions about hardware demand.

TurboQuant directly addresses a core cost pain point of large models—the KV cache. During inference, a 70-billion-parameter model serving 512 users with a 2,048-token input requires approximately 512 GB of memory just for the KV cache, roughly four times the size of the model itself. TurboQuant achieves an 83% reduction in memory footprint by compressing the KV cache to 3 bits through two-step optimization: PolarQuant polar-coordinate quantization and QJL residual correction.

Model Efficiency Gains

Moreover, cutting-edge artificial intelligence is becoming abundant and inexpensive. Chinese labs charge only a fraction of what U.S. labs do for similar work. Meanwhile, competitors such as NVIDIA (NVDA.US), Cohere, Reflection, and Mistral are developing cheaper, smaller, and more efficient alternatives for enterprise use.

Artificial Analysis, an AI benchmarking firm, evaluates all major models on the same set of 10 assessments and tracks total cost. For the most powerful models from each lab: Anthropic’s Claude costs $4,811; OpenAI’s ChatGPT costs $3,357; DeepSeek costs $1,071; Kimi costs $948; and Zhipu AI’s GLM costs $544. Claude’s cost is nearly nine times that of the cheapest Chinese alternative for the same workload.

Moreover, these low-cost alternatives are no longer lagging behind. DeepSeek, the Chinese AI lab whose emergence last year triggered a sell-off in U.S. tech stocks, released a preview of its next-generation model last month. This model performs on par with—or nearly identically to—the latest offerings from OpenAI, Anthropic, and Google across coding, agent, and knowledge benchmarks. Over the past four months, other Chinese labs—including Beijing-based Moonshot AI, Xiaomi, and Zhipu AI—have also released models with comparable performance levels.

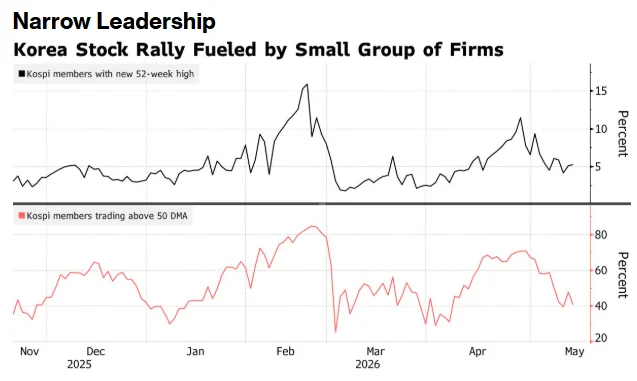

A Special Bull Market Risk—Korea’s Concentration Risk: A ‘Two-Headed Monster’ Stock Market

The KOSPI index closed just above 4,300 points on its first trading day of 2026, but within less than six months surged past 8,000 intraday—an increase of over 85% from the start of the year, outperforming all other major global indices. However, the structure of this bull market is highly distorted. Although the KOSPI comprises more than 800 constituent stocks, Samsung Electronics and SK Hynix—the two semiconductor leaders—account for nearly 50% of the index’s weighting. This means the index is almost entirely driven by the performance of just two stocks, with more than 600 individual stocks underperforming the index, highlighting a severe imbalance in underlying market fundamentals.

Calls for Profit-Taking

On May 13, Steve Brice, Global Chief Investment Officer at Standard Chartered Bank, stated in an interview that he believes the bullish sentiment in the South Korean equity market is “not too far off.” He revealed, “I was in Korea last week, and we advised clients to take profits on part of their portfolios and rotate those investments into globally diversified portfolios.”

This risk became starkly evident on May 15. The KOSPI plunged 488 points, or 6.1%, closing at 7,493. The two largest weighted stocks, Samsung Electronics and SK Hynix, fell by 8.6% and 7.7%, respectively. Although the market rebounded somewhat afterward, this “stock market crash” fully exposed the vulnerability of South Korea’s equity market stemming from its excessive concentration.

Geopolitical risks are equally significant. Analysts have noted that against the backdrop of heightened global geopolitical tensions, structural imbalances and sector-specific cyclical issues in the South Korean equity market introduce substantial uncertainty into its outlook.

Bull Market Champions Remain Confident

Despite this, some international investment banks remain highly optimistic about the prospects for South Korea’s equity market. On May 21, Nomura Securities significantly raised its 2026 KOSPI target range from the previous 7,500–8,000 points to 10,000–11,000 points, citing factors such as the ongoing supercycle in conventional memory and high-bandwidth memory (HBM), as well as South Korea’s inclusion on MSCI’s watchlist for developed markets, which could serve as additional catalysts. UBS Group also revised upward its earnings per share (EPS) growth forecasts for the KOSPI in 2026, 2027, and 2028 to 258%, 46%, and 9%, respectively. The 2026 figure exceeds the market consensus estimate of 235%, making it the strongest among Asia-Pacific emerging markets.

Risk Landscape: Undercurrents Beyond the Bull Market Narrative

The Consumer Cost of Supply-Demand Imbalance

Soaring memory chip prices are triggering ripple effects downstream across the supply chain. In the first quarter of 2026, smartphone sales in China declined by 6% year-over-year, primarily due to memory shortages and new device price increases of 10% to 30%, which have extended consumer replacement cycles to over 36 months. The cost of the mainstream smartphone configuration—8GB RAM + 128GB storage—has surged by as much as 290%. The PC market is similarly under pressure; IDC forecasts that by 2026, high component costs will make “AI PCs” unaffordable for many consumers and enterprises, potentially reducing PC shipments by 9%.

In niche markets, MLC NAND flash memory prices have risen approximately 300% year-over-year, with 16Gb MLC NAND surging from around $3.20 in Q1 2025 to roughly $12.90 in Q2 2026, posing potential disruptions to industries such as automotive electronics, industrial control, and medical devices.

The Sword of Damocles Hanging Over the Capacity Expansion Cycle

In June 2025, Micron Technology announced plans to invest $200 billion in capacity expansion over the coming years, while Samsung and SK Hynix are also accelerating their investments. Although large-scale ramp-up of new capacity will not occur before 2028, once production begins, the supply-demand balance could shift rapidly. Historical experience shows that once a memory industry capacity expansion cycle starts, the transition from shortage to oversupply often happens faster than market expectations.

As one analyst noted, “If Micron and its competitors’ new capacities come online between 2027 and 2028, the duration of this price rally becomes the central variable underpinning the entire bullish thesis.”

Uncertainty from Technological Disruption

The TurboQuant incident illustrates that rapid AI iteration can disrupt hardware demand assumptions at any time. From a broader perspective, large model architectures themselves are undergoing transformation—trillion-parameter models employing dynamic parameter activation mechanisms can reduce inference costs by 73% and cut cache usage by 90%. While such efficiency gains may expand total demand in the long run through the Jevons paradox effect, they undoubtedly exacerbate market volatility in the short term.

Jon Cunliffe, Head of the Investment Office at wealth management firm JM Finn, remains prudently pragmatic. He pointed out that there is significant room for output growth over the next three years, which could alleviate supply constraints, “especially if AI demand grows at a more normalized pace.” He added, “Current share prices assume prolonged high valuations, strict investment discipline by companies, and substantially improved profit margins relative to the past. We must also emphasize that the sector has recently experienced intense momentum-driven positioning, making it vulnerable to market corrections.”

Outlook: The Party Isn’t Over Yet—But Fasten Your Seatbelts

Fundamentals in the memory market remain robust heading into Q2 2026. According to TrendForce, contract prices for commodity DRAM are expected to rise 58% to 63% quarter-over-quarter, while NAND flash contract prices are projected to increase 70% to 75% sequentially. South Korea’s semiconductor exports during the first ten days of May neared a record high of $8.5 billion, still up 150% year-over-year.

Bullish positions from top-tier investment banks such as Nomura Securities and UBS Group, Micron CEO’s view that supply shortages will persist until 2028, and incremental demand driven by the wave of AI agents are all supporting the current high-valuation narrative.

Yet history teaches us that when market consensus is strongest, risk is often most underestimated. Signals ranging from William de Gale’s cyclical warnings and Paul Tudor Jones’s bearish options positions to unsettling concentration levels in South Korean equities all remind investors that even the most powerful bull markets require due respect for risk.

“The memory cycle is over”—this statement has been repeated far too many times throughout the history of the memory industry, and each time it has ultimately proven wrong. Will this time truly be different? The answer will unfold over the next few years. Regardless of the outcome, however, the debate between cyclical dynamics and structural shifts has already become one of the most compelling narratives in global capital markets in 2026.