When inflation, interest rates and growth signals are all pulling in different directions, a portfolio’s foundation matters more than ever. With central banks in Europe and the US keeping policy data dependent and energy prices feeding into inflation and bond yields, many investors are looking for stocks that can hold up across a wide range of scenarios. Our Low-Risk Leaders screener focuses on companies with strong balance sheets and the lowest risk scores in our model, aiming to reduce portfolio swings. In this article, you will see three of the stocks from this screener that fit that brief.

Griffin Mining (AIM:GFM)

Overview: Griffin Mining is a London headquartered mining and investment company focused on extracting zinc, gold, silver, lead and other precious metals, with its key operation being the Caijiaying mine in Hebei Province, China.

Operations: Griffin Mining generates all its revenue of about US$137.5 million from the Caijiaying Zinc Gold Mine in China.

Market Cap: £526.2 million

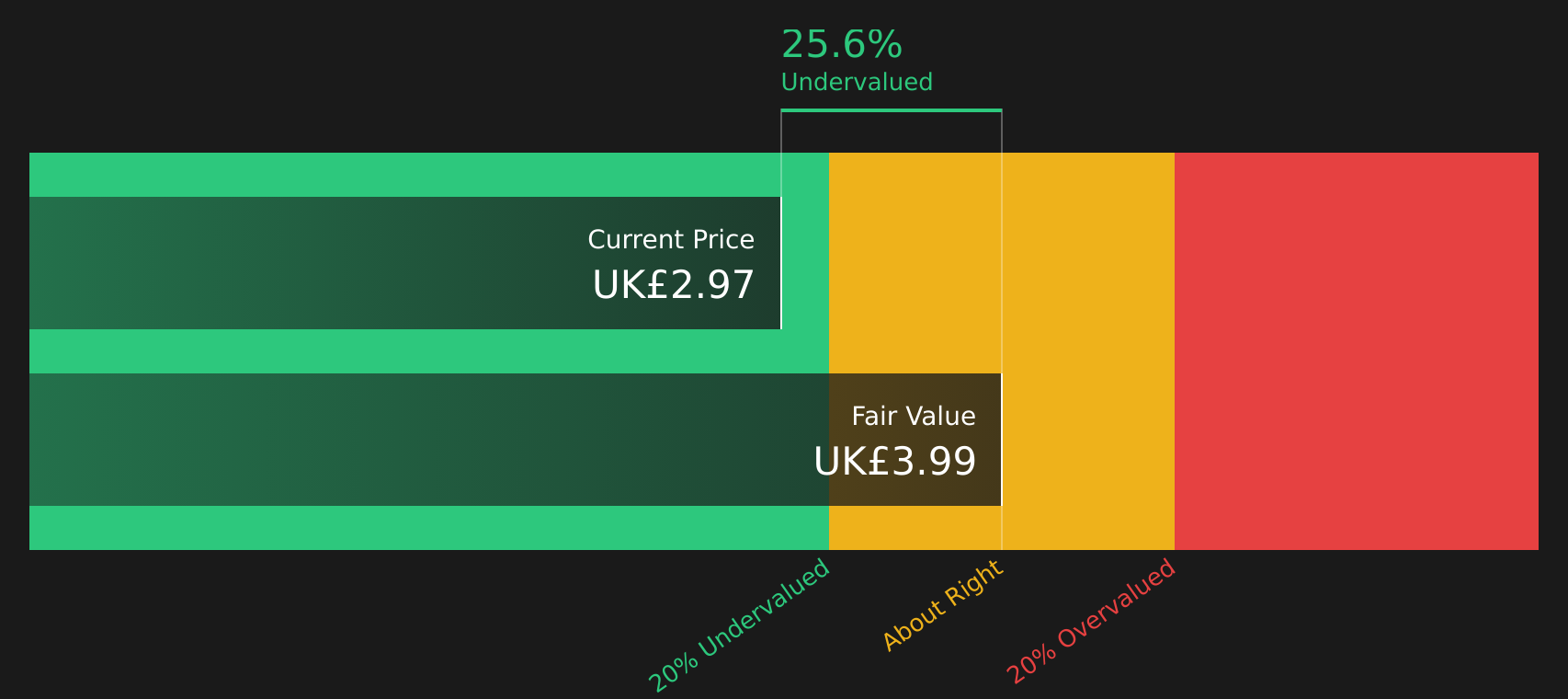

Griffin Mining may attract investor attention because it combines a single high quality producing asset with recent financial momentum and long term visibility on ore from Zone II, where mining is permitted under the current licence through 2054. Revenue and earnings have grown, with net income at US$22.06 million and margins at 16%, while the stock is indicated as trading below the Simply Wall St DCF estimate of fair value. Set against this, investors need to weigh a P/E of 31.9x, concentrated exposure to one mine in China and a board that currently has limited independence. These factors make further due diligence important.

Griffin Mining’s single mine story, current earnings and DCF discount suggest that the market may not be pricing the full picture yet. The DCF valuation analysis for Griffin Mining could help clarify what might be driving that gap.

Oxford Instruments (LSE:OXIG)

Overview: Oxford Instruments develops and sells high end scientific equipment such as microscopes, nano measurement tools and quantum technology systems that help researchers and companies analyse materials, semiconductors and advanced devices in detail.

Operations: Oxford Instruments generates most of its revenue from the Imaging & Analysis segment at £314.7 million, with the Advanced Technologies segment contributing £108.5 million.

Market Cap: £1.59b

Oxford Instruments sits at the crossroads of advanced manufacturing, semiconductors and quantum technologies. Recent earnings have grown faster than both the UK market and the wider electronics sector. The relatively high P/E and a share price that is already close to analyst targets mean that future returns are likely to depend on whether margin expansion, order book strength and collaborations such as the Covalent partnership continue to support earnings. Currency swings, higher taxes and a mixed long term profit trend also play a role, so this is a stock where the quality of execution really matters for investors focusing on lower risk leaders.

Oxford Instruments’ earnings are accelerating faster than many investors may realise, yet the current valuation and tax headwinds raise harder questions about what happens next. The analysis report for Oxford Instruments could reveal the one assumption that might change how you see this stock.

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, private equity and venture capital funds, with a focus on renewable energy projects, social and digital infrastructure, and providing equity and credit to smaller companies across the UK, Europe and Australia.

Operations: Foresight Group Holdings generates most of its revenue from Real Assets at £114.8 million, with Private Equity contributing £50.1 million, and a large majority of income sourced from the United Kingdom alongside smaller contributions from Australia and several European markets.

Market Cap: £506.4 million

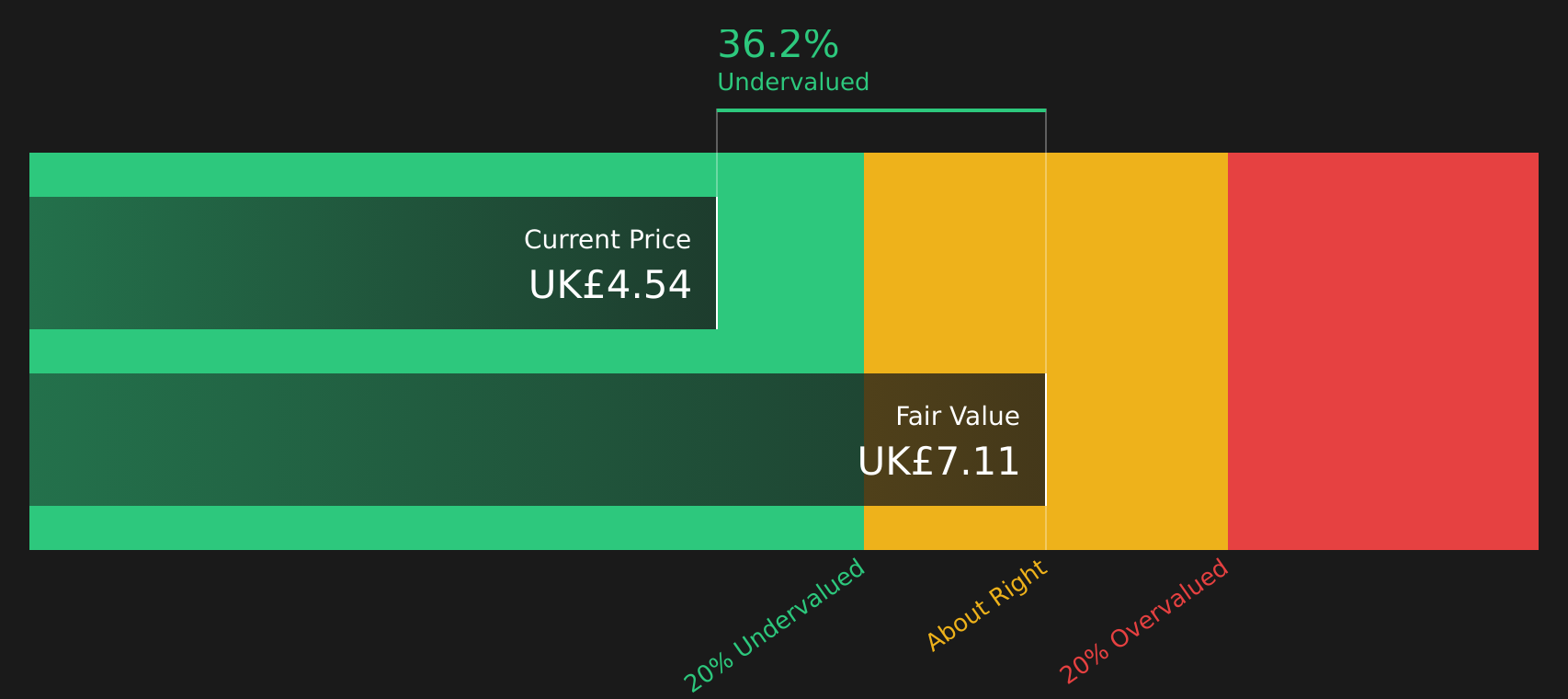

Foresight Group Holdings is highlighted in the Low Risk Leaders context because it combines high profitability with exposure to long term themes like energy transition and infrastructure, while still trading below estimates of its future cash flow value and analyst price targets. Earnings have grown faster than the wider Capital Markets industry and margins are reported at 27.7%, supported by strong forecast growth and a 47.8% ROE. The P/E remains below both sector and peer averages. At the same time, investors need to factor in funding risk from reliance on external borrowing, sensitivity to UK and European regulation, and the lumpier nature of performance fees, which means the quality of execution and capital allocation will be crucial.

Foresight Group’s high profitability, strong ROE and exposure to energy transition themes suggest that the story is still developing. The analyst forecasts for Foresight Group Holdings sets out one forward-looking detail that could change how you frame the risks.

The three stocks in this article are just a starting point, and the full Low-Risk Leaders screener uncovered 4 more companies with equally compelling low risk stories that you have not seen yet. Use Simply Wall St to identify and analyze the specific catalysts, balance sheet strength and risk factors that matter most to you so you can focus on the highest conviction opportunities in this group.

Take Control of Your Investment Journey

If Griffin Mining or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Today?

Fresh stock ideas do not stay under the radar for long. Before momentum takes off and ideal entry ranges are gone, scan these focused shortlists and consider your options.

- Target dependable income streams by reviewing a curated set of high-yield opportunities in the 3 dividend fortresses before yields compress and prices start flying.

- Spot emerging trends early by checking the curated 52 AI infrastructure stocks powering data centers and AI capacity while these enablers are still under the radar for now.

- Review potential commodity opportunities by scanning a hand picked 33 elite gold producer stocks as market interest evolves.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com