The United States market has experienced a robust performance, climbing 4.0% in the last week and 39% over the past year, with earnings forecasted to grow by 16% annually. In this thriving environment, growth companies with strong insider ownership can be particularly appealing as they often indicate confidence from those closest to the business, aligning well with current market optimism.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 35.7% | 74.1% |

| Upstart Holdings (UPST) | 13% | 53.6% |

| Precigen (PGEN) | 11.9% | 68.4% |

| Karman Holdings (KRMN) | 17% | 53.2% |

| Enovix (ENVX) | 11.3% | 41.1% |

| Clene (CLNN) | 12% | 62.2% |

| Caledonia Mining (CMCL) | 14.3% | 28.5% |

| Better Home & Finance Holding (BETR) | 19.3% | 99.2% |

| Astera Labs (ALAB) | 11% | 28.3% |

| AppLovin (APP) | 27.3% | 21.7% |

Let’s dive into some prime choices out of the screener.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Duos Technologies Group, Inc. designs, develops, deploys, and operates intelligent technology solutions in North America with a market cap of $253.76 million.

Operations: Revenue segments for Duos Technologies Group, Inc. are not specified in the provided text.

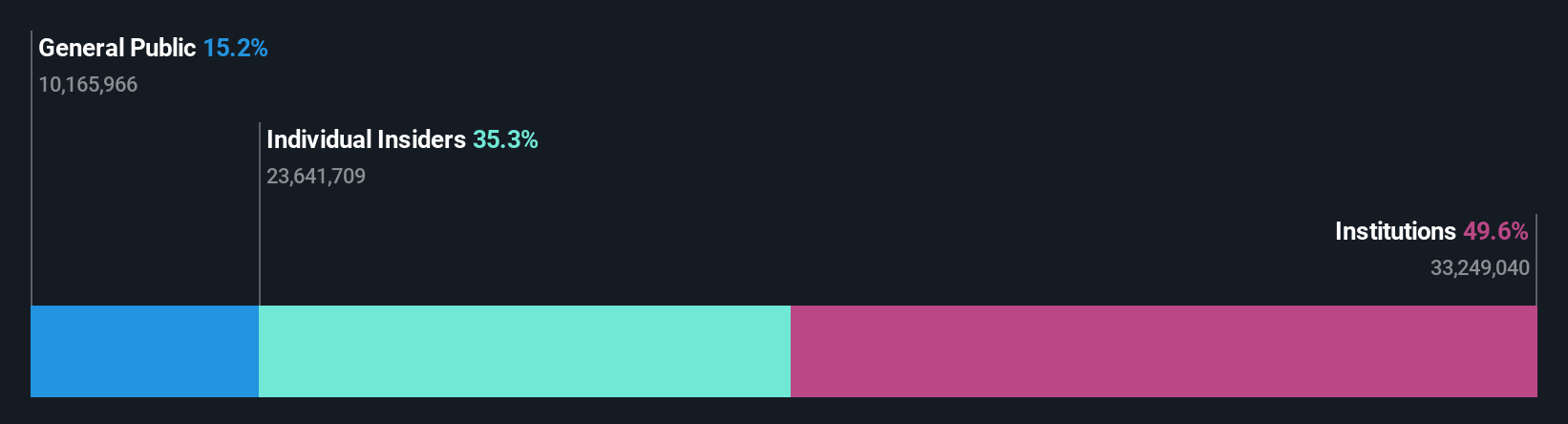

Insider Ownership: 12%

Earnings Growth Forecast: 141.2% p.a.

Duos Technologies Group, Inc. is experiencing significant growth, driven by its strategic partnership with Hydra Host to deploy high-density NVIDIA GPU clusters. This initiative is projected to generate approximately US$176 million in revenue over three years with gross margins exceeding 80%. Despite past shareholder dilution, Duos is forecasted for robust revenue growth of 36.6% annually and profitability within three years. Recent financial results show improved net loss figures alongside substantial insider ownership, indicating strong internal confidence in the company’s trajectory.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Daqo New Energy Corp., along with its subsidiaries, produces and sells polysilicon for photovoltaic product manufacturers in China, with a market cap of approximately $1.47 billion.

Operations: The company generates revenue primarily from the sale of polysilicon, amounting to $665.42 million.

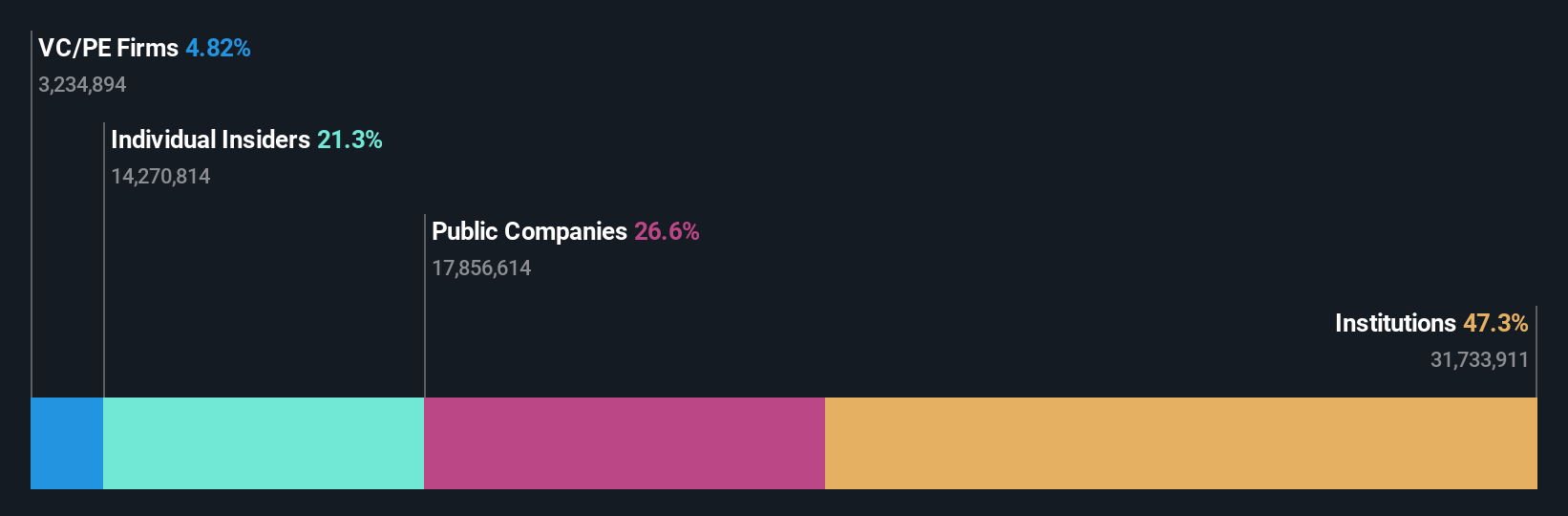

Insider Ownership: 33.8%

Earnings Growth Forecast: 103% p.a.

Daqo New Energy demonstrates potential for growth with a forecasted annual revenue increase of 26.9%, outpacing the US market average. Despite a net loss of US$170.51 million in 2025, the company is expected to achieve profitability within three years, reflecting above-average market growth. Recent production figures show an increase in polysilicon output, and insider ownership remains significant without substantial recent trading activity, suggesting confidence in Daqo’s strategic direction amidst its current undervaluation at 55.8% below fair value estimates.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: MediaAlpha, Inc. operates an insurance customer acquisition platform in the United States and has a market cap of approximately $638.39 million.

Operations: The company’s revenue is primarily generated from its Internet Information Providers segment, amounting to $1.11 billion.

Insider Ownership: 11.1%

Earnings Growth Forecast: 20.3% p.a.

MediaAlpha’s growth potential is underscored by expected annual earnings growth of 20.3%, surpassing the US market average. Recent launches, like their AI app for auto insurance, enhance their programmatic marketplace offerings. Despite a revenue forecast below market average, insider ownership remains significant with minimal recent trading activity. The company trades at 79.3% below estimated fair value and has increased its buyback plan to US$100 million, indicating strategic confidence amidst high debt levels and strong earnings performance last year.

Next Steps

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com