Global markets are wrestling with mixed inflation signals, shifting rate expectations and uneven growth across regions, which makes clear earnings visibility and balance sheet strength especially important. That is where the Healthy high growth potential screener can help. It focuses on companies that analysts expect to grow earnings firmly over the next 3 years and that also sit in an acceptable financial position. This article highlights three stocks from that screener, giving you a focused shortlist to research further if you are looking for growth opportunities that are backed by analyst forecasts and supported by financial discipline.

Sylvania Platinum (AIM:SLP)

Overview: Sylvania Platinum is a producer of platinum group metals such as platinum, palladium and rhodium, as well as chrome, primarily by processing mine tailings in South Africa and exploring near surface deposits. Its operations include multiple chrome tailings retreatment plants and exploration projects including Everest North, Volspruit, Aurora and Hacra, with corporate headquarters in Hamilton, Bermuda.

Operations: Sylvania Platinum generates essentially all of its revenue, about US$155.5m, from the Sylvania Dump Operations tailings retreatment business, with a small segment adjustment of roughly US$1.0m.

Market Cap: £233.0m

Sylvania Platinum may appeal to investors who want exposure to platinum group metals through a business focused on processing waste material rather than building deep new mines. This approach can help keep capital needs in check. Analysts have highlighted the company’s cash generative profile and some see scope for the stock price to close a wide gap to their view of fair value. However, factors such as the funding structure, mixed longer term earnings history and governance questions mean the setup involves risks. Understanding the balance between the company’s potential and these risks is important for investors considering this stock.

Sylvania Platinum’s cash generative profile and tailings focus hint at a story that many investors may be underestimating, especially if the funding structure and governance questions are masking the bigger picture in the 5 key rewards and 1 important warning sign

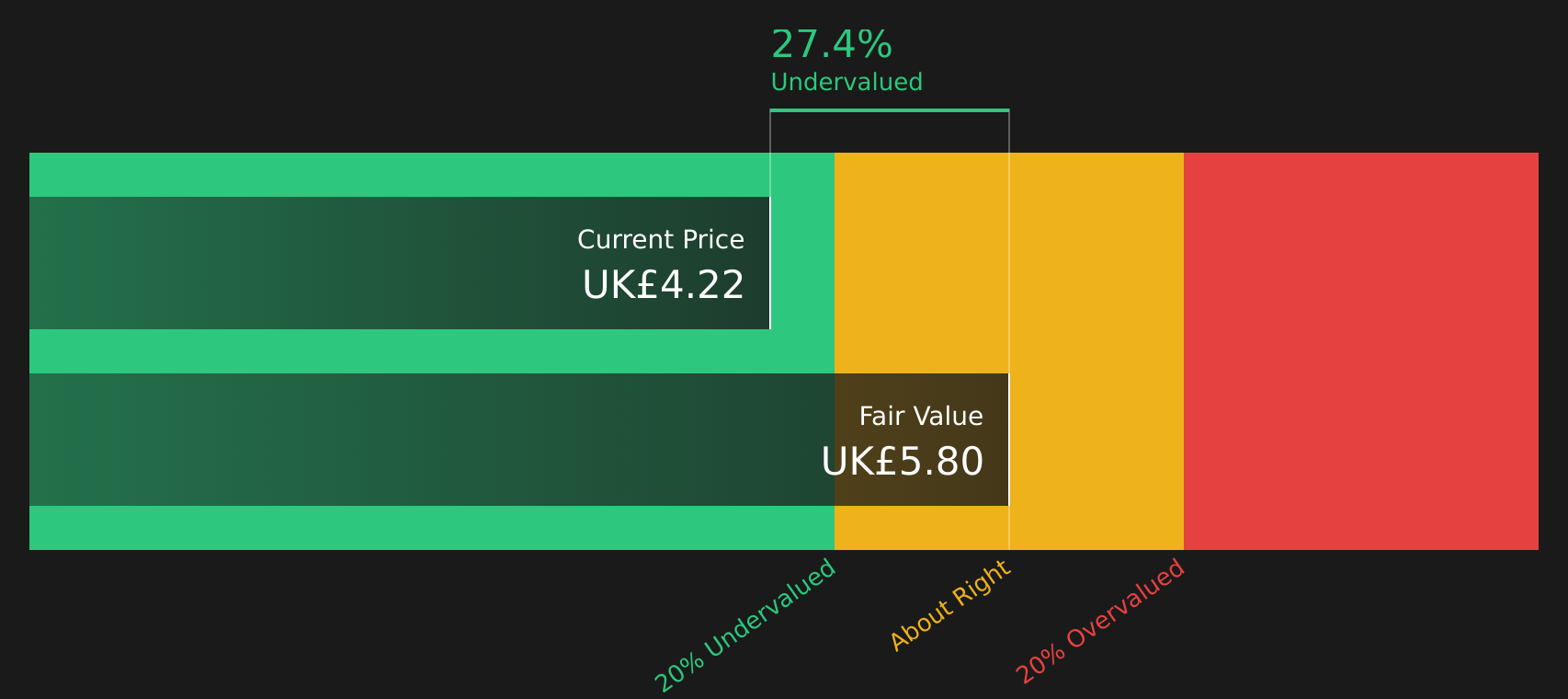

Metals Exploration (AIM:MTL)

Overview: Metals Exploration is a London based miner that focuses on finding, developing and operating gold and other precious and base metal projects, with its core asset being the 100% owned Runruno gold project located north of Manila in the Philippines, alongside additional exploration ground in the Philippines and Nicaragua.

Operations: Metals Exploration currently generates all of its approximately US$208.4m in revenue from gold and other precious metal production in the Philippines.

Market Cap: £393.4m

Metals Exploration may appeal to investors who want direct gold exposure backed by an operating mine, revenue of about US$208.4m and net income of US$28.9m, while also gaining potential upside from projects such as the Batong Buhay copper gold venture and concessions in Nicaragua. Analyst expectations for earnings and revenue growth are being compared with a share price that some estimates suggest is below fair value. This combination can be attractive if those expectations are achieved. At the same time, the company relies fully on external borrowing, has relatively low current ROE and limited board independence, so funding risk and governance are key issues that may warrant closer inspection.

Metals Exploration’s revenue, operating mine and extra growth options indicate that the full story is not yet reflected in the share price, particularly if funding and governance are better understood in the analysis report for Metals Exploration

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that focuses on infrastructure, renewable energy and private equity, giving investors access to real assets and sustainable investment opportunities across the UK, Europe and Australia through listed funds and private vehicles.

Operations: Foresight Group Holdings generates most of its revenue from Real Assets at about £105.7m, alongside £47.4m from Private Equity and £9.2m from Foresight Capital Management.

Market Cap: £473.5m

Foresight Group Holdings may appeal to investors who want exposure to renewable energy and infrastructure themes within an asset management model that earns largely recurring fees. Its current return on equity (ROE) of 44.3% points to an efficient underlying business. At the same time, expansion into Europe and Australia, heavier regulation around ESG products and reliance on external borrowing introduce meaningful risks if fund flows slow or compliance costs rise. Recent share buybacks and a 60% dividend payout policy indicate a clear focus on shareholder returns.

Foresight Group Holdings is earning high ROE and buying back shares, but the real story sits in how its fee engine compares with regulatory and funding pressures in the analysis report for Foresight Group Holdings

The three highlighted stocks are just a starting point, with the full Healthy high growth potential filter surfacing 36 more companies with similarly compelling setups and stories in the Healthy high growth potential screener. Identify and analyze the specific catalysts, growth drivers and financial narratives that matter most to you inside Simply Wall St so you can focus on the highest conviction opportunities.

Take Control of Your Investment Journey

If Foresight Group Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Today?

Some of the most interesting stocks often move from quiet accumulation to full breakout before most investors notice. Scan fresh ideas while they are still under the radar for now and consider them while they remain less widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com