Kiah Treece is a licensed attorney and small business owner with experience in real estate and financing. Her focus is on demystifying debt to help individuals and business owners take control of their finances.

Kiah Treece is a licensed attorney and small business owner with experience in real estate and financing. Her focus is on demystifying debt to help individuals and business owners take control of their finances.

Jordan Tarver has spent several years writing and editing for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor’s degree in business finance and his personal experience to simplify complex financial topics. Jordan’s promise is actionable advice that’s easy to understand.

Jordan Tarver has spent several years writing and editing for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor’s degree in business finance and his personal experience to simplify complex financial topics. Jordan’s promise is actionable advice that’s easy to understand.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

Personal loan rates currently range from around 5% to 36%, depending on the lender, borrower creditworthiness and other factors. While interest rates are not the only costs associated with taking out a loan, it’s important to compare lenders to identify the best personal loan rates available.

Best Personal Loan Rates Of 2024

The above lists our best personal loan providers by highest to lowest annual percentage rate (APR) range. The below lists these providers in order from highest to lowest star rating. Our loan experts rate providers based on APR, as well as loan details, eligibility requirements, customer experience and more.

BEST OVERALL PERSONAL LOAN RATES

LightStream

APR range

7.49% to 25.49%

with autopay

7.49% to 25.49%

with autopay

Why We Picked It

With low minimum and maximum interest rates, LightStream personal loans stand out for having the best overall interest rates for a range of loan amount. Beyond that, LightStream charges no origination, late payment or prepayment fees. The lender also offers a 0.50% rate discount for borrowers who enroll in autopay, which is higher than most lenders with the same perk.

Pros & Cons

- No origination, prepayment or late fees

- Low, competitive rates

- Fast approval and funding

- No prequalification process

- No due date flexibility

- Limitations on use of loan proceeds

Details

Overview: LightStream is a consumer lending division of Truist—which formed following the merger of SunTrust Bank and BB&T. The platform offers unsecured personal loans from $5,000 to $100,000. Loan amounts vary based on the loan purpose. Although a number of lenders offer smaller loans than the LightStream minimum, few lenders offer a higher maximum loan. Repayment terms are available from two to seven years.

LightStream offers loans in all 50 states plus Washington, D.C., and applicants can contact the lender’s customer support team seven days a week; current borrowers have access to customer support from Monday through Saturday. While LightStream doesn’t offer a mobile app for loan management, customers can access their account through LightStream.com.

Eligibility:

- Applicants should have several years of credit history

- Minimum credit score: 660

- Can’t prequalify

Loan uses:

- Large expenses

- Finance land, timeshares and tiny homes

- Home project

BEST FOR LARGE LOAN AMOUNTS

SoFi®

APR range

8.99% to 29.49%

with autopay

8.99% to 29.49%

with autopay

Why We Picked It

SoFi personal loans range from $5,000 to $100,000, making the lender a great option for those with excellent credit who need to borrow a large amount of money. Loan amounts available may vary by the state you live in. Repayment terms range from two to seven years, making SoFi an incredibly flexible option for those with sufficient credit (minimum 650) and annual income (at least $45,000).

Pros & Cons

- Prequalification with soft credit check

- Funding in as little as one to two days

- High loan amounts and lengthy terms

- Does not offer direct payment to third-party creditors for debt consolidation

- Some applicants report difficult qualification standards

- Co-signers are not permitted

Details

Overview: Founded in 2011, SoFi is an online lending platform that offers unsecured fixed-rate personal loans in every state, extending over $50 billion in loans. SoFi offers comparatively low APRs and doesn’t charge origination fees, late fees or prepayment penalties—a stand-out feature because personal loan lenders often charge origination or late payment fees at a minimum.

However, if you’re considering a debt consolidating loan from SoFi, keep in mind that the lender does not offer direct payment to a borrower’s other creditors. This means the loan proceeds will be deposited to your bank account and you’ll have to pay off your other lenders individually.

Eligibility:

- Minimum credit score required: 650

- Minimum annual income: $45,000

- Co-signers not permitted

Loan uses:

- Medical expenses

- Credit card consolidation

- Home projects

- Moving costs

BEST FOR CURRENT WELLS FARGO ACCOUNT HOLDERS

Wells Fargo

APR range

7.49% to 23.24%

with autopay discount

7.49% to 23.24%

with autopay discount

Why We Picked It

For customers with an established relationship with Wells Fargo, a Wells Fargo personal loan is a good option thanks to the 0.25% or 0.50% relationship discount. Wells Fargo offers fixed-rate personal loans with limits between $3,000 to $100,000 and repayment terms from 12 to 84 months. While longer term lengths, such as 84 months, will decrease your fixed monthly payment, you will pay more interest over the life of your loan compared to a loan with terms of, let’s say, 12 months.

Pros & Cons

- Receive funds the next business day, if approved

- 0.25% discount when you enroll in autopay

- No origination fees or prepayment penalty

- Must have a Wells Fargo checking account to receive 0.25% discount

- New Wells Fargo customers will need to visit a branch to apply

- No option to prequalify

Details

Overview: Wells Fargo offers fixed-rate personal loans with limits between $3,000 to $100,000 and repayment terms from 12 to 84 months. Although Wells Fargo is available to anyone in the United States, only current Wells Fargo customers will be able to apply online.

New customers will need to visit a branch location. Wells Fargo does not have branch locations in Indiana, Kentucky, Louisiana, Ohio, Oklahoma, Maine, Massachusetts, Michigan, Missouri, New Hampshire, Vermont or West Virginia.

Eligibility:

- Doesn’t disclose minimum credit requirement

- Doesn’t disclose minimum income requirement

- Doesn’t allow co-signers or co-borrowers

Loan uses:

- Debt consolidation

- Home improvement

- Medical bills

BEST FOR NO INTEREST IF REPAID WITHIN 30 DAYS

Discover

Why We Picked It

Discover personal loans offer borrowers the ability to repay their loans within 30 days interest-free. Along with that feature, Discover stands out because of its online application and mobile banking tools, well-reviewed customer support team and quick funding. In general, loans are available from $2,500 to $40,000 and may be issued for between three and seven years.

Pros & Cons

- Option to pay off creditors directly

- No origination fees or prepayment penalties

- Directly pays creditors

- Charges late fees

- Low maximum loan amount

Details

Overview: Discover is an online bank that also offers customers credit cards, retirement solutions and personal loans in all 50 states. Discover charges a late payment fee and does not offer an autopay discount; however, it does not charge any origination fees or prepayment penalties, making it competitive with other top personal loan providers.

Eligibility:

- Minimum credit score: 660

- Minimum household income: $25,000

- Doesn’t allow co-signers or co-borrowers

Loan uses:

- Medical bills

- Business expenses

- Home renovation

BEST FOR EXISTING U.S. BANK CUSTOMERS

U.S. Bank

APR range

8.24% to 24.99%

with autopay

Loan amounts

$1,000 to 50,000 to existing U.S. Bank customers (up to $25,000 for noncustomers)

Depends on the area you live in

8.24% to 24.99%

with autopay

$1,000 to 50,000 to existing U.S. Bank customers (up to $25,000 for noncustomers)

Depends on the area you live in

Why We Picked It

For their current customers, U.S. Bank personal loans are a great option since having a checking account here allows borrowers to access higher borrowing amounts and longer repayment terms. For customers, loan terms range from 12 to 84 months and loan amounts from $1,000 to $50,000.

Pros & Cons

- 0.50% autopay discount if payments are made from a U.S. Bank checking or savings account

- Funding in as little as one day after approval

- Competitive rates for borrowers with excellent credit

- Must refinance at least $5,000

- Charges early closure fee if you close your account within one year

- Refinance loans only available in 26 states

Details

Overview: U.S. Bank is one of the largest banks in the country. In addition to banking, wealth management and business services, it also offers several lending products, including auto refinancing.

In order to qualify as a U.S. Bank customer, you must have a U.S. Bank checking account. Non-U.S Bank customers must apply in person. U.S Bank has branches in 26 states: Arkansas, Arizona, California, Colorado, Iowa, Idaho, Illinois, Indiana, Kansas, Kentucky, Minnesota, Missouri, Montana, North Carolina, North Dakota, Nebraska, New Mexico, Nevada, Ohio, Oregon, South Dakota, Tennessee, Utah, Washington, Wisconsin and Wyoming.

Eligibility:

- Minimum credit score: 650

- Doesn’t disclose minimum income requirements

- Can apply with co-borrower

Loan uses:

- Medical bills

- Debt consolidation

- Home project

BEST FOR LOW RATES AT A CREDIT UNION

PenFed

Why We Picked It

PenFed is a national credit union with fixed-rate, low-interest loans that start at $600 to $50,000. PenFed personal loans carry rates from 8.49% to 17.99%, based on your application and credit information, and there’s no early payoff penalty and no origination or hidden fees.

Pros & Cons

- No origination or hidden fees

- Funds could be available the next day

- Few qualification requirements

- Branches only located on the East Coast

- Must open a PenFed savings account to become a member

Details

Overview: Although PenFed was originally created to serve U.S. military members and veterans, in addition to federal employees and retirees, it has expanded its membership to non-military members. PenFed has several federal partners, including the American Society of Military Comptrollers, Coast Guard Auxiliary Association, Navy League of the United States and United States Army Warrant Officers Association.

Although PenFed is located on the East Coast, borrowers will have around-the-clock access to their accounts through the PenFed mobile app. Anyone can apply for a loan through PenFed; however, if you’re approved and choose to move forward with your loan, you’ll need to become a member of the credit union. Becoming a member is easy, and it typically only takes a few minutes. While the membership is free, you’ll need to make a deposit of at least $5 into a new PenFed savings account.

Eligibility:

- Be a PenFed member

- Minimum credit score: 650

- Can apply with a co-borrower

Loan uses:

- Debt consolidation

- Home project

- Medical expenses

BEST FOR LOANS AS LOW AS $1,000

Upstart

Why We Picked It

With various loan options, including loan amounts ranging from $1,000 to $50,000, an Upstart personal loan is a good option for borrowers looking for small personal loans. Beyond that, the lender’s minimum 300 credit score makes it an accessible option to those with fair credit.

Pros & Cons

- Accessible to borrowers with fair credit

- Offers prequalification with a soft credit check

- Ability to choose a custom payment date

- Charges an origination fee up to 8% of the loan amount

- No secured or co-signer option

- Loans only available for three-, five-, seven-year terms

Details

Overview: Upstart has made a mark on the personal loan space because of its artificial intelligence- and machine learning-based approach to borrower qualification. In fact, Upstart estimates that it has been able to approve 27% more borrowers than possible under a traditional lending model.

Even though Upstart’s three-, five-, seven-year loan terms are more restrictive than other lenders, it’s likely to be an acceptable tradeoff for applicants who might not be approved in a more traditional lending environment. Plus, it’s available in every state except West Virginia and Iowa, so it’s as widely available as many other top lenders.

Eligibility:

- Minimum credit score: 300

- Minimum income requirement: $12,000

- Doesn’t allow co-signers or co-borrowers

Loan uses:

- Debt consolidation

- Medical expenses

- Educational expenses

Summary: Best Personal Loan Interest Rates Of February 2024

The above personal loan rates and details are accurate as of February 1, 2024. While we update this information regularly, the annual percentage rates (APRs) and loan details may have changed since the page was last updated. Keep in mind, some lenders make specific rates and terms available only for certain loan purposes. Be sure to confirm available APR ranges and loan details, based on your desired loan purpose, with your lender before applying.

Tips for Comparing Personal Loan Rates

In general, annual percentage rates (APRs) vary by lender and depend on several factors, including the applicant’s creditworthiness. However, there are several things you can do to access the lowest rate possible when applying for a personal loan. Consider these factors when comparing personal loan rates:

Credit score and eligibility requirements.

Average borrower rates.

Loan amounts and repayment terms.

Additional costs.

Pro Tip

In addition to interest rates, be aware of any origination fees, processing fees, prepayment penalties and other charges associated with the loan. Consider these costs while evaluating the overall affordability of the loan.

Complete Guide To Personal Loan Rates

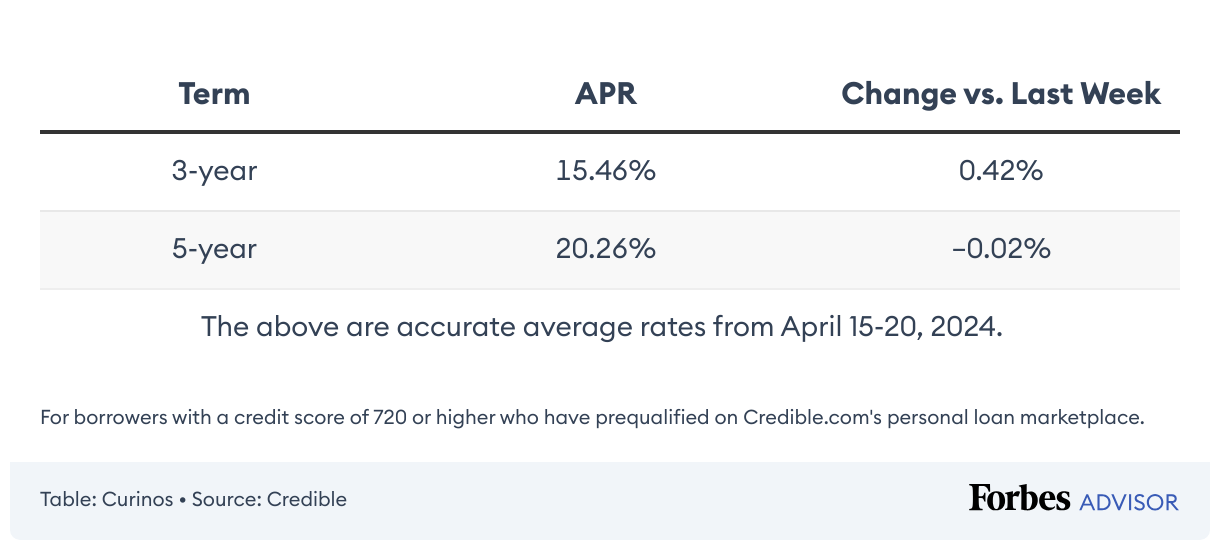

Current Personal Loan Rates

What Is a Good Interest Rate on a Personal Loan?

Personal loan rates range from around 5% to 36%, with the average hovering around 12-15% for a 3-year loan. A good interest rate on a personal loan is one that is lower than the national average. However, borrowers with excellent credit scores may qualify for even lower rates.

Average Personal Loan Interest Rates By Credit Score

Interest rates vary by lender, borrower qualifications and loan characteristics. However, interest rates are best predicted by a borrower’s credit score. According to Experian, the average interest rates for Vantage Score ranges are as follows:

Personal Loan Rates for Excellent Credit

Personal Loan Rates for Good Credit

Personal Loan Rates for Fair Credit

Personal Loan Rates for Bad Credit

How Lenders Determine Personal Loan Rates

Lenders determine personal loan rates based on several factors, but the applicant’s credit score and overall credit profile are the most important. Many traditional and online lenders also look at the prospective borrower’s income and current outstanding debts to determine their debt-to-income ratio (DTI).

DTI is the ratio of a borrower’s monthly income to their monthly debt service and is used to evaluate an applicant’s ability to make on-time payments. The higher the DTI, the riskier the borrower—and the higher the interest rate they’ll likely receive.

When determining personal loan rates, some online and alternative lenders also look at a prospective borrower’s occupation and education to evaluate earning potential. Likewise, lenders may evaluate the risk posed by a borrower based on where they live.

How to Get the Best Personal Loan Rates In 2024

The most competitive personal loan rates are typically reserved for the most creditworthy borrowers. However, there are other factors that can impact rates, and it is possible to get a lower rate without a stellar credit profile. Follow these tips to get the best personal loan rates:

- Understand your credit report. Before prequalifying or applying for a personal loan, request a copy of your credit report from one of the three main credit bureaus—Equifax, Experian and TransUnion. A credit report includes valuable insight into how your credit scores are calculated and how much risk you pose to lenders. Likewise, check your credit score and use it to prequalify for an APR before submitting to a hard credit inquiry.

- Calculate the best loan amount and term. Personal loan APRs are generally higher for larger loans and more extended repayment terms. That said, shorter repayment terms mean larger monthly payments. Use a personal loan calculator to determine how much monthly payment you can afford, and then opt for the shortest possible loan term.

- Apply with a co-signer or co-borrower. If you won’t qualify for a competitive APR based on your personal credit, consider applying with a co-borrower or co-signer who has a higher credit score. This approach can lead to higher approval odds and lower personal loan rates.

- Choose a secured loan. A secured personal loan is one that is collateralized by a valuable asset, such as real estate. If a borrower defaults on a secured loan, the lender can seize the collateral in order to recoup the outstanding loan balance. Because secured loans are less risky to lenders, they may be a better fit for borrowers who can’t qualify for a personal loan or a competitive APR.

- Take advantage of rate discounts. Many lenders offer rate discounts to borrowers who sign up for automatic payments during the loan application process. When comparing lenders, choose an option that offers autopay discounts or other savings opportunities.

- Opt for a fee-free lender. To remain competitive, some lenders moved to a fee-free structure that does not charge origination fees, late payment fees, prepayment penalties or other additional costs. Choosing a fee-free lender can reduce the overall cost of a loan, thereby reducing the APR.

Pros and Cons of Personal Loans

Before taking out a personal loan to consolidate debt or finance your next purchase, it’s a good idea to run through the pros and cons. Below are the advantages and disadvantages of personal loans you should be aware of.

Pros of Personal Loans

- Flexible loan amounts

- Unsecured loans typically require no collateral or down payment

- Fixed installment payments

- Can qualify for low interest rates

- Loan funding may happen in a week or less

- Funds can be used to pay for almost any type of legal personal expense

Cons of Personal Loans

- Loans may have origination fees

- Collateral may be required if you don’t have good credit

- Borrowers with less-than-perfect credit may qualify for higher interest rates

- Loans can damage your credit history if you don’t make on-time payments

- Late payment fees or prepayment penalties may increase the cost of the loan

Where To Get a Personal Loan

Various lenders offer personal loans and some may be better suited for you and your financial needs. Before accepting a loan, consider

How To Get a Personal Loan

Although the process can vary by lender, you’ll generally take these steps in order to get a personal loan:

- Check your credit. Before starting your search for lenders, check your credit score for free through your credit card issuer or another service. This will help you narrow down which lenders will be willing to work with you.

- Improve your credit. If your credit score is lower than 610, take steps to improve your credit score such as lowering your credit usage or paying off debts. This can help you qualify for a loan and, in some cases, a lower interest rate.

- Shop around for lenders. Determine how much money you need to borrow and which lenders whose qualification requirements you meet. Many lenders will let you pre-qualify before submitting a formal application, which allows you to see the rates you could qualify for without impacting your credit score.

- Submit an application. Once you find the lender that works best for you, submit an application. Depending on the lender, this can take hours or days.

Calculate Personal Loan Payments

A personal loan calculator can help you estimate the payments on a personal loan and how much interest will cost you. Before accepting a loan, estimate your payments to be sure they’ll fit into your budget.

Recap: Best Personal Loan Interest Rates of 2024

- LightStream: Best for borrowers who can qualify for low interest rates and want a lender with no origination, late payment or prepayment fees

- SoFi: Best for borrowers who are looking to borrow a large personal loan

- Wells Fargo: Best for borrowers who have an existing relationship with the lender

- Discover: Best for borrowers who can repay their loan within 30 days

- U.S. Bank: Best for borrowers who are U.S. Bank customers and can take advantage of the customer discounts

- PenFed: Best for borrowers looking to get low interest rates at a credit union

- Upstart: Best for borrowers who are looking to borrow a small amount

Methodology

We reviewed 29 popular lenders based on 16 data points in the categories of loan details, loan costs, eligibility and accessibility, customer experience and the application process. We chose the best lenders based on the weighting assigned to each category:

- Loan cost. 35%

- Loan details. 20%

- Eligibility and accessibility. 20%

- Customer experience. 15%

- Application process. 10%

Within each major category, we also considered several characteristics, including available loan amounts, repayment terms, APR ranges and applicable fees. We also looked at minimum credit score requirements, whether each lender accepts co-signers or joint applications and the geographic availability of the lender. Finally, we evaluated each provider’s customer support tools, borrower perks and features that simplify the borrowing process—like prequalification options and mobile apps.

Where appropriate, we awarded partial points depending on how well a lender met each criterion.

To learn more about how Forbes Advisor rates lenders, and our editorial process, check out our Loans Rating & Review Methodology.

Frequently Asked Questions (FAQs)

A personal loan is a type of financing that lets borrowers access cash for a wide range of personal uses, including home improvements, auto repairs and unanticipated expenses. Loan amounts and repayment terms vary by lender, but the best personal loans typically range from $1,000 to $100,000 with some starting as low as $250. In general, loan repayment terms extend from one to seven years.

What’s the difference between APR and interest rate?

The main difference between APR versus interest rate is that the interest rate is the actual cost to borrow money. In contrast, a loan’s annual percentage rate includes the interest rate plus additional costs like finance charges as the annual cost over the life of the loan.

Can I negotiate personal loan rates with lenders?

In some cases, you may be able to negotiate with lenders to get a lower interest rate on your personal loan. Call and ask the lender if you can lower your interest rate, and if that doesn’t work, refinancing your loan may be the best option for securing a lower interest rate.

Can I get a personal loan with bad credit?

It is possible to get a personal loan with bad credit, but it is generally more difficult to qualify—especially for competitive rates. Less creditworthy applicants also face lower borrowing limits and higher interest rates than more qualified applicants. However, some lenders specialize in personal loans for borrowers with bad credit, instead basing lending decisions on alternative credit data.

How much will a personal loan cost?

The cost of a personal loan depends on the lender, type of loan and the borrower’s creditworthiness. Interest typically accrues on personal loans at a rate from 4% to 36%, with the lowest rates accessible to high-credit borrowers. In addition to interest, some lenders also charge origination fees between 1% and 8% of the total loan amount. Borrowers also may be subject to late payments fees and/or prepayment penalties, which can increase the total cost of the personal loan.

How much can you borrow with a personal loan?

How large of a personal loan you can borrow depends on what the lender offers and your own creditworthiness. It’s possible to find lenders offering a wide range of loan amounts from a few hundred dollars up to $100,000.

When you apply with a lender, they’ll consider several different factors to figure out how much to approve you for. This could include your credit score, monthly income, other debt obligations and overall credit history.

Next Up In Personal Loans

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.