Your three-digit credit score is one factor that lenders, such as banks or other financial service providers, consider when deciding whether to approve you for loans, lines of credit or credit cards — and what interest rate you’ll pay.

In Canada, Equifax is one of two credit reporting agencies, or bureaus, that collect information about your credit use and generate credit scores for both lenders and the public.

What is an Equifax credit score?

Your Equifax credit score is a three-digit number from 300 to 900 that lenders and other creditors use to evaluate your credit risk.

Equifax is a credit bureau — a private company that collects and shares information about your financial behavior in Canada. Equifax Canada was founded in 1989, although its U.S-based parent firm has been around since the late 1800s, making it the oldest of the major credit bureaus.

Using data from lenders and financial institutions, Equifax generates a credit report that outlines your borrowing and payment history.

Equifax uses this information to calculate your three-digit credit score, using scoring models provided by the Fair Isaac Corporation (FICO) combined with its own proprietary algorithms.

Your credit score is a window into your credit activity and history at a particular point in time — but can also fluctuate depending on your recent actions, for example, if you’ve closed a credit card, missed a bill payment or applied for a loan.

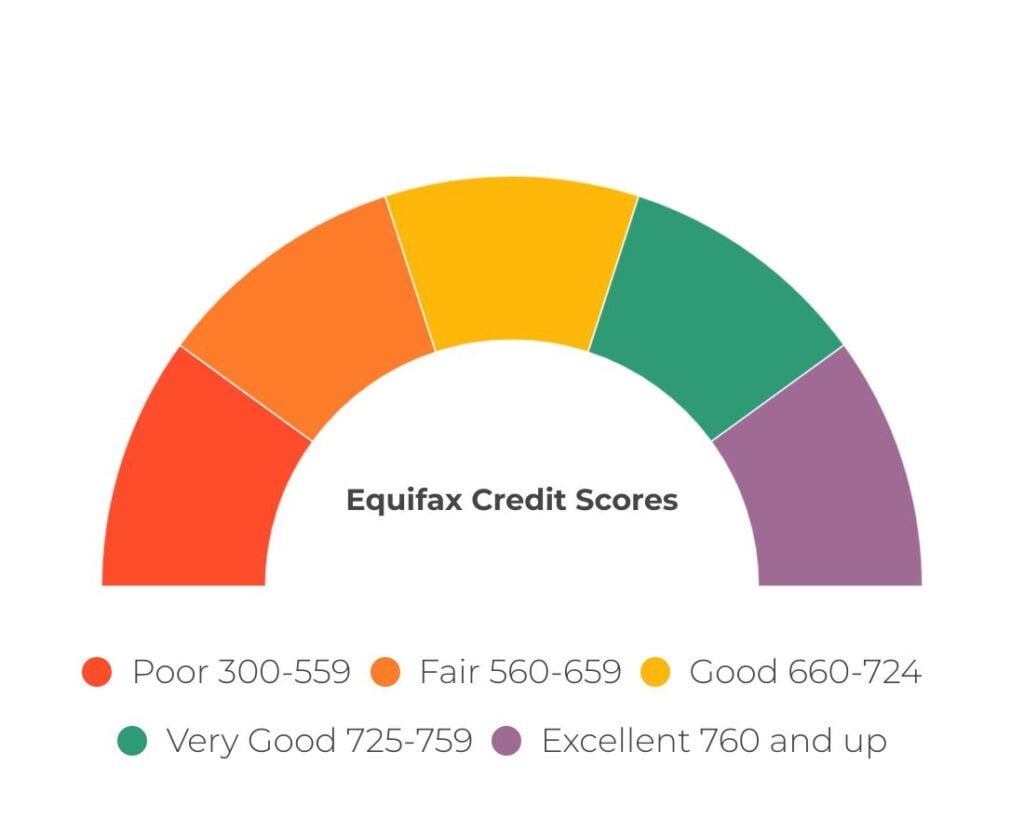

Equifax credit score ranges

What Equifax credit score ratings mean

Poor: You likely have a number of credit “delinquencies” or you may not have had the chance to build up your credit history. As a high-risk borrower, you will face challenges accessing unsecured credit or qualifying for favourable interest rate terms.

Fair: You may be re-establishing or building your credit but are still considered higher-risk and may still have some difficulty accessing lower interest rates or unsecured credit cards.

Good: You are likely in control of your debt picture and will likely be able to qualify for loans from a variety of lenders at competitive rates.

Very Good: You are considered a low-risk borrower and will likely qualify for most financial products with favourable rates.

Excellent: You have demonstrated responsible credit behaviour and will likely be considered the lowest-risk borrower by lenders and qualify for a wide range of loans and credit cards with the most favourable interest rates on the market.

How to Get Your Equifax Score in Canada

There are several ways to access your Equifax credit score in Canada. Canadians can check their Equifax credit report and credit score for free, by registering with MyEquifax, with information updated monthly. You can also request a free copy of your credit report by phone, by mail or in person. Equifax also offers daily access to credit scores and other features via a subscription, at a cost of $24.95 per month, after a 30-day free trial.

Through fintech companies like Borrowell and Mogo, you can access your Equifax credit score by creating a free account, although these third-party providers will also provide recommendations for optional financial products to purchase.

Some Canadian banks also allow their customers to check their Equifax credit score for free via their online banking or through the Interac verification service app.

Credit scores from other providers

Equifax is not the only credit bureau in Canada — your credit score may vary from one credit bureau to another, as a result of varied scoring models, lenders reporting different data to one credit bureau or another or a delay in data being reported.

You may also see credit scores in Canada from:

TransUnion: Similar to Equifax, TransUnion is a Canadian credit bureau that uses data from lenders to generate credit reports and scores, as well as sharing general insights on credit industry trends.

Fair Issac Corporation: FICO isn’t a credit bureau, but an independent data analytics company that leverages data from Equifax and TransUnion to produce its own three-digit credit score (called a FICO score). FICO is widely recognized and used in the U.S., and many Canadian lenders also use this metric.

How to improve your Equifax score

Getting a better credit score is possible — here are a few healthy financial habits that can help you get there:

Keep an eye on your credit utilization ratio: Credit scores are impacted by your credit utilization ratio — the amount of credit you’re using, compared to your credit limit. For example, if your credit card limit is $5,000 and your credit card balance is $2,500, you have a credit utilization ratio of 50%. As a rule of thumb, keeping your credit utilization ratio at 30% or under can help improve your credit score.

Pay attention to bill repayment: Payment history is one of the biggest factors impacting your credit score — keeping on top of your monthly bills and all debt payments on time is essential to improving your Equifax score.

Build your credit history: As much as 15% of your Equifax credit score is based on history — having a record of consistent borrowing and repayment activity on your report shows lenders how you’re able to handle credit over time. Keeping a no-fee credit card active and using it sparingly, rather than cancelling the card, can work to build credit history — and improve your Equifax score.

Keep new applications in check: Each time you apply for a new credit card, line of credit, personal loan or mortgage, the lender will carry out a “hard inquiry” on your credit profile. Each credit inquiry can lower your score by a few points and can stay on your Equifax report for three years (in some cases, multiple inquiries carried out over a short time period in order to compare loans — such as mortgage rates, for example — may not count as separate inquiries.) Consider the impact that credit inquiries may have on your Equifax credit score before deciding whether you need to apply for new loans or credit cards.