Crypto card payments have grown sharply to more than $1.5 billion a month. This report asks whether that marks crypto cards as genuine financial infrastructure or a model that is still maturing.

-

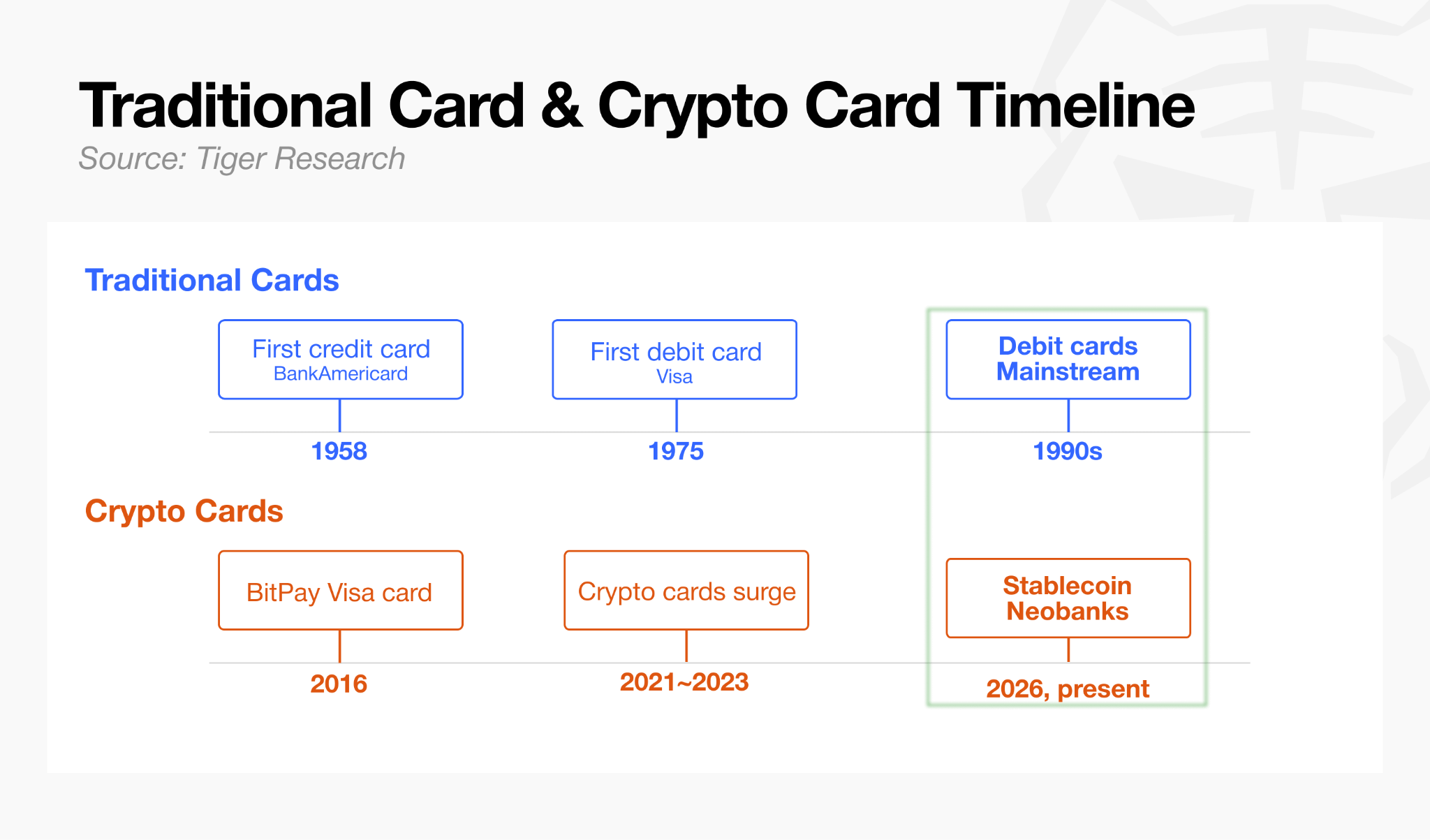

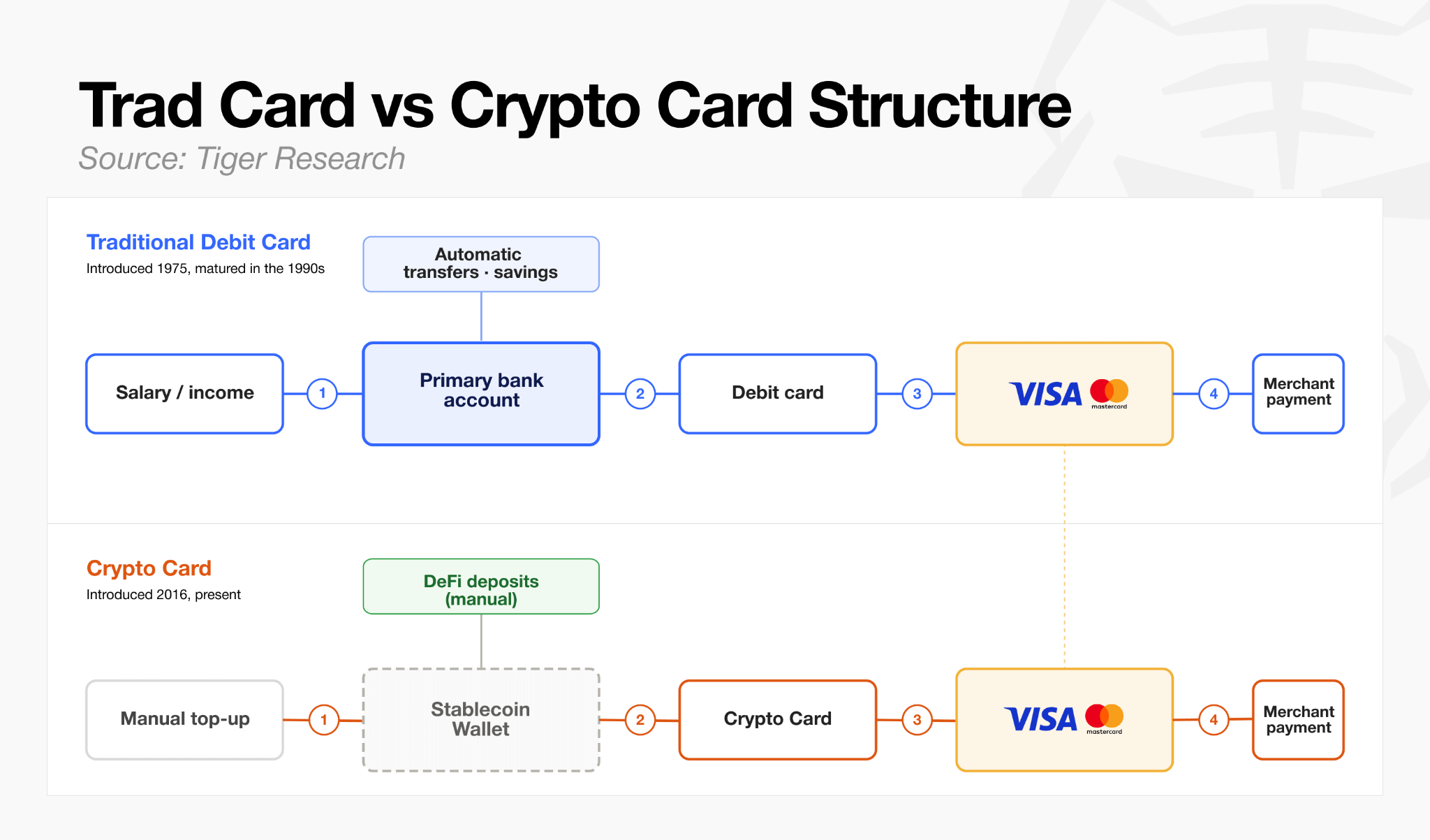

Crypto cards resemble debit cards just before their 1990 commercialization, since both use existing payment networks to skip the merchant acceptance bottleneck. The primary-account relationship, salary deposits and recurring expenses, remains unbuilt.

-

RedotPay alone leads a market of roughly $18 billion in annualized volume, with users concentrated in emerging markets. This makes crypto cards a supplementary tool for underserved, dollar-scarce regions rather than universal financial infrastructure.

-

Payment volume growth alone does not secure crypto cards’ place as financial infrastructure. The market will likely be reshaped by who controls the flow of funds, claims regions large institutions haven’t reached, and owns the everyday financial relationship above the infrastructure layer.

In September 1958, Bank of America mailed cards to 65,000 residents of Fresno, California. Issued as the first payment card without any supporting infrastructure, it produced a dismal result within a year, a 22% delinquency rate and $20 million in losses. Building the electronic settlement system took 15 years, and the debit card took 17 years to arrive, while Visa’s path to becoming the global standard took 20 years in total.

The largest difference lies in whether an everyday financial relationship has taken hold.

The debit card, which first appeared in 1975, became a core instrument of the primary bank account only in the 1990s, once salary deposits spread in earnest. Today’s crypto card, by contrast, begins with a stablecoin deposit. Most crypto wallets still lack the everyday financial relationships of recurring salary deposits and fixed expenses, which places crypto cards somewhere around the stage the debit card occupied around 1990.

Whoever leads in crypto cards will be determined less by the number of cards issued than by who first builds the account that is used in daily life, or a growth trigger of that kind.

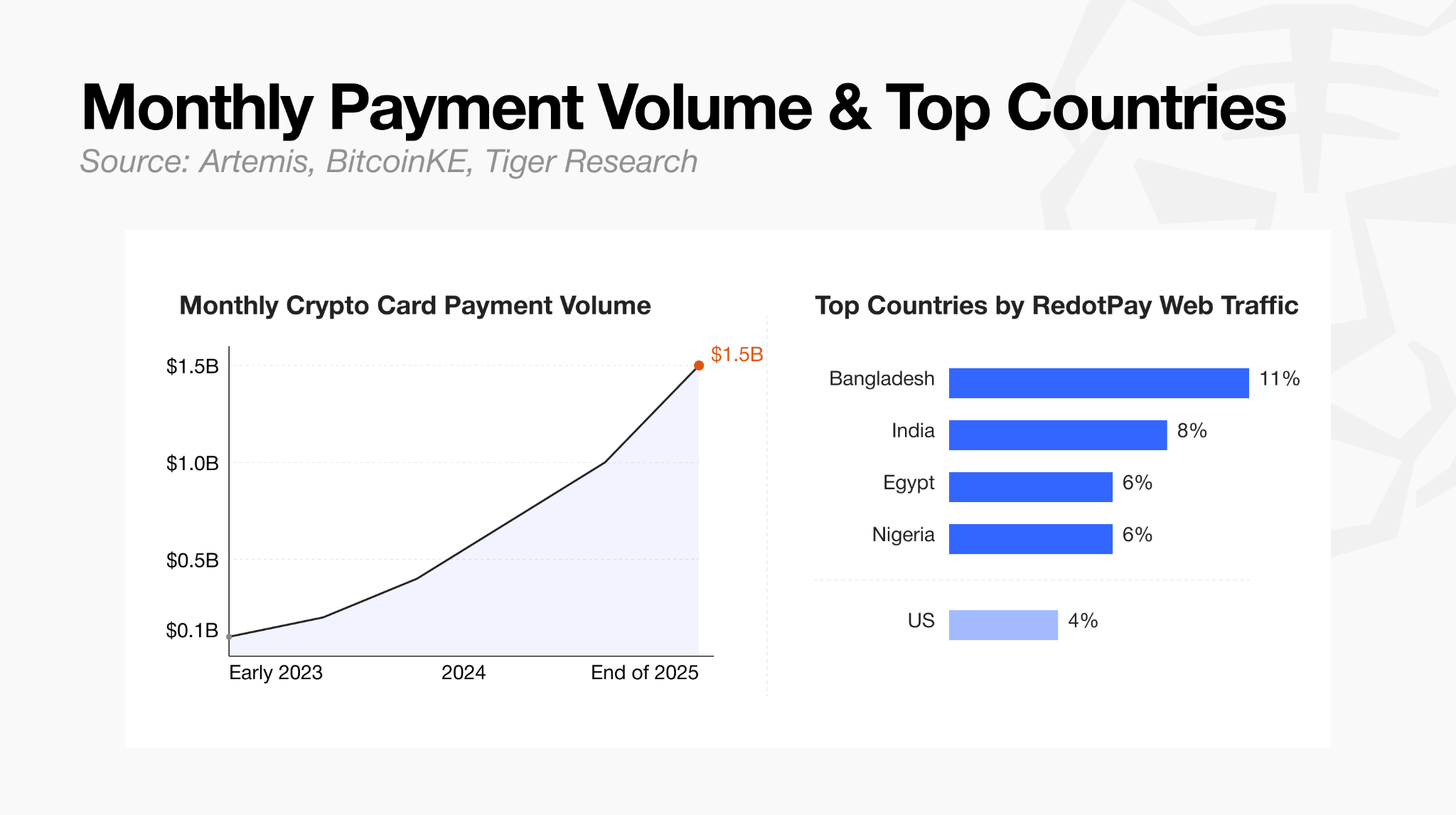

According to Artemis, crypto cards’ monthly payment volume grew from around $100 million in early 2023 to $1.5 billion at the end of 2025, which exceeds $18 billion on an annualized basis. The figure differs somewhat from a simple annualization depending on the scope of on-chain tracking, but the rapid increase in payment volume is clear.

A closer look at the indicators shows a pronounced concentration in particular services and regions. A single service, RedotPay, accounts for more than half of all transactions, and its top countries by web traffic are concentrated mainly in emerging markets, including Bangladesh at 11%, India at 8%, Egypt at 6%, and Nigeria at 6%. The US accounts for only 4%.

Real demand for crypto cards today therefore comes not from mainstream developed markets but from underserved regions with limited dollar access.

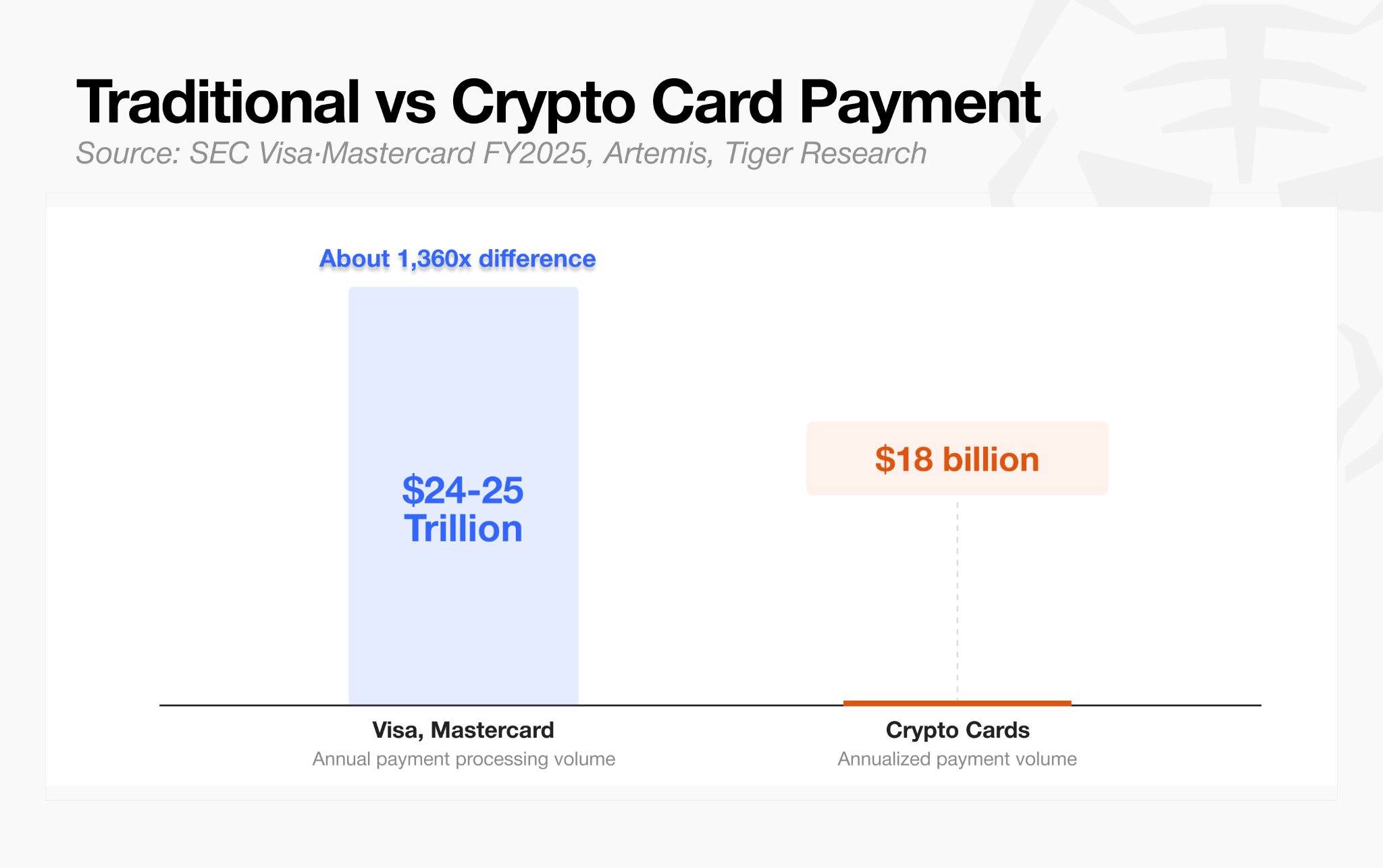

The scale gap with established financial networks remains wide. Visa and Mastercard process $24 to $25 trillion in annual payments, whereas crypto cards’ annualized payment volume stands at only about $18 billion. This makes the difference in weight class with the established market clear. .

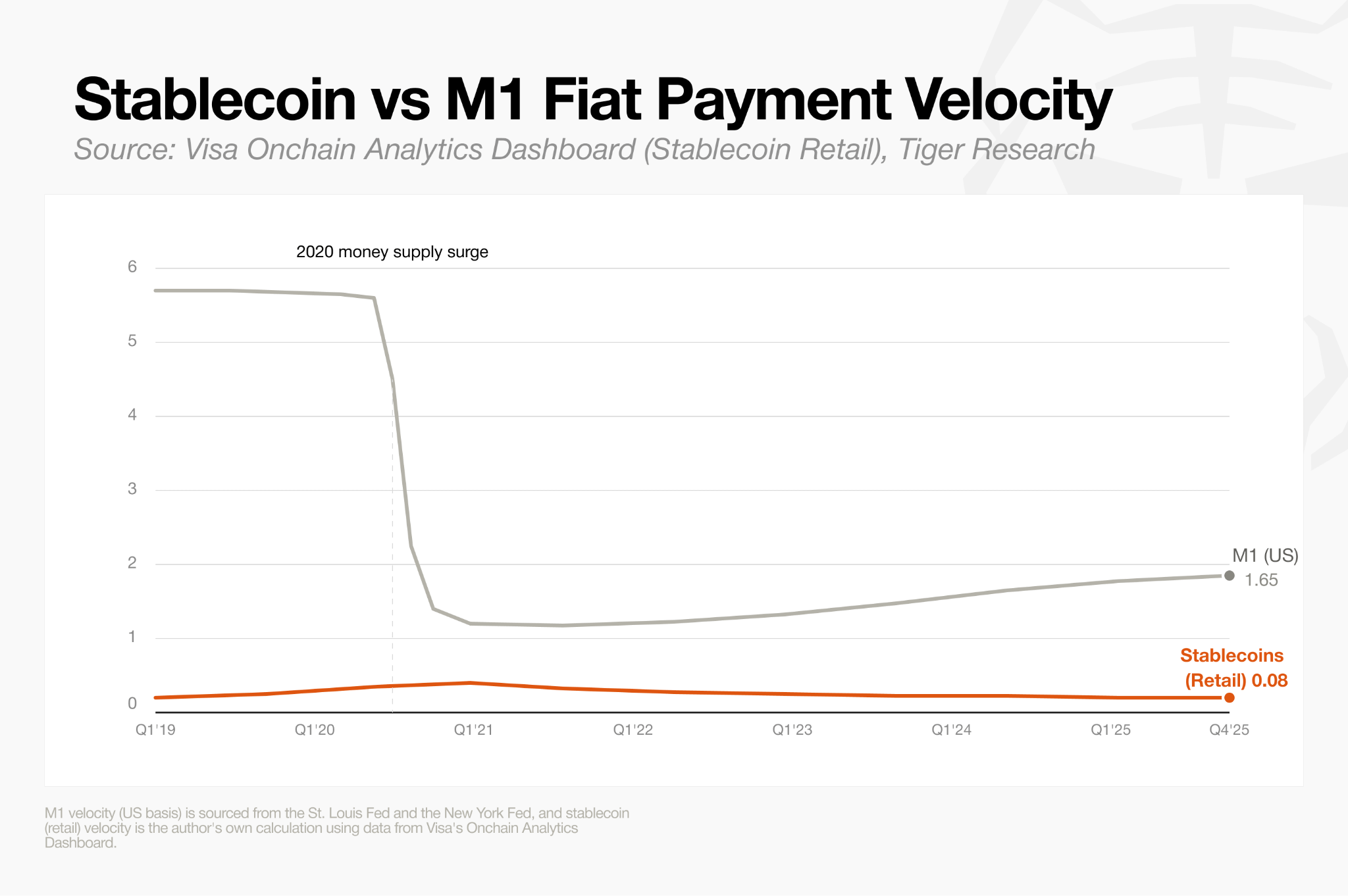

Indicators of use as an everyday payment instrument are also low. Velocity measures how many times, on average, a given asset is used for payments over a set period, and a higher figure means the asset is used more actively for spending than for holding.

Visa’s tracking of on-chain stablecoin transactions put retail velocity at 0.08, roughly one-twentieth of the 1.65 velocity of standard fiat money (M1). Users are therefore treating stablecoins less as something received like a salary, spent in daily life, and replenished, and more as a balance loaded once and drawn down only occasionally.

Quantitative growth in payment volume does not by itself mean broad settlement in the market. A substantial share of current crypto card volume comes from users in emerging markets with limited access to dollar accounts. For these users, crypto cards do function as a meaningful instrument for everyday finance to some degree.

In developed markets, however, crypto cards have not yet secured clear product-market fit (PMF), nor have they formed the close account relationships that come from recurring salary deposits and automatic transfers.

Considering the inflow paths of funds and the nature of the spending, today’s crypto card is therefore closer to a supplementary tool that serves specific countries’ use cases than to universal financial infrastructure. Building on this growth, however, major players are emerging that are advancing each part of the model.

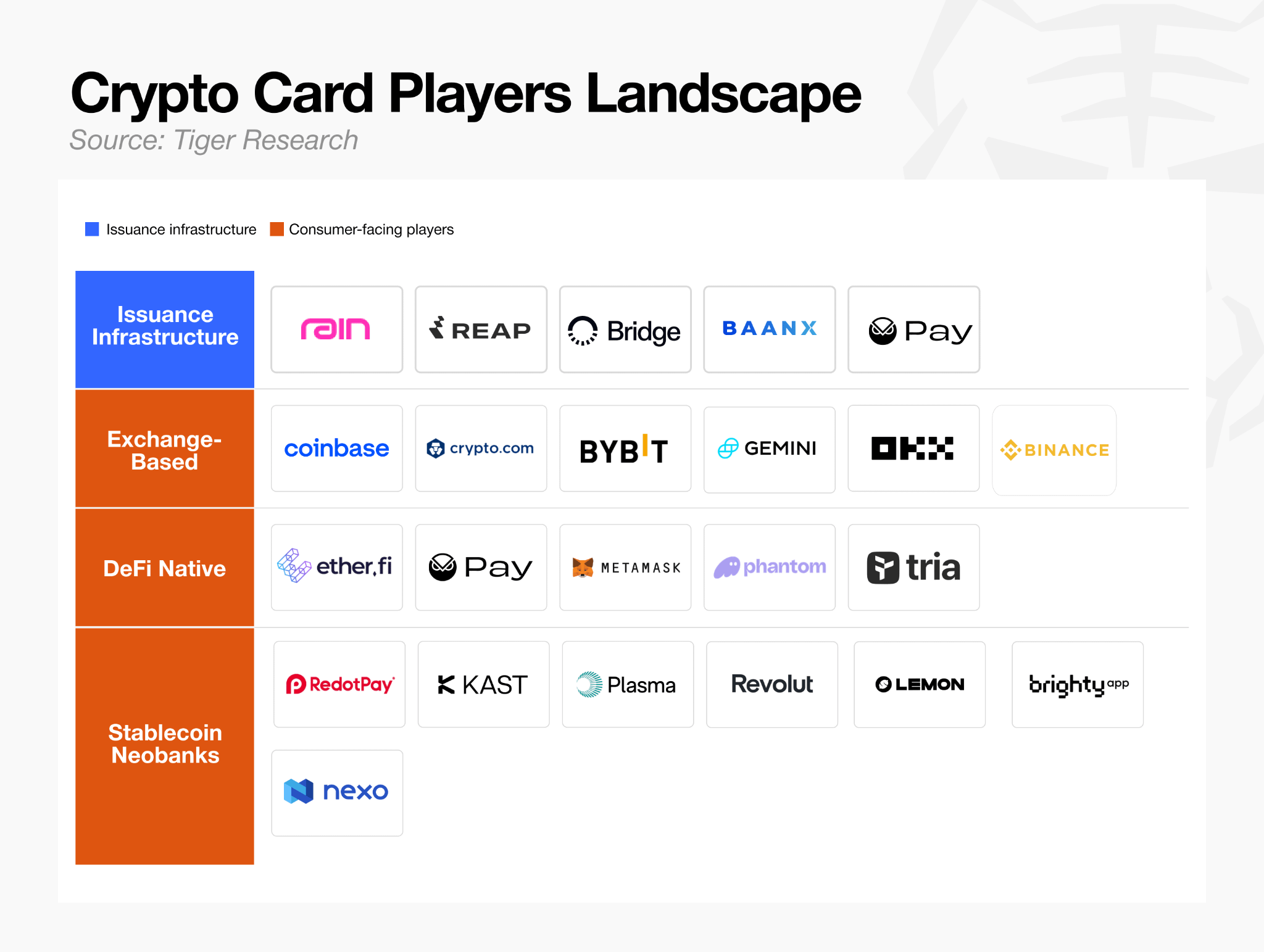

The crypto card sector divides broadly into four business models, and players compete to establish an early position in different layers. The forms vary widely, from firms that focus on providing back-end infrastructure to models that borrow only the card format while fully differentiating the underlying structure.

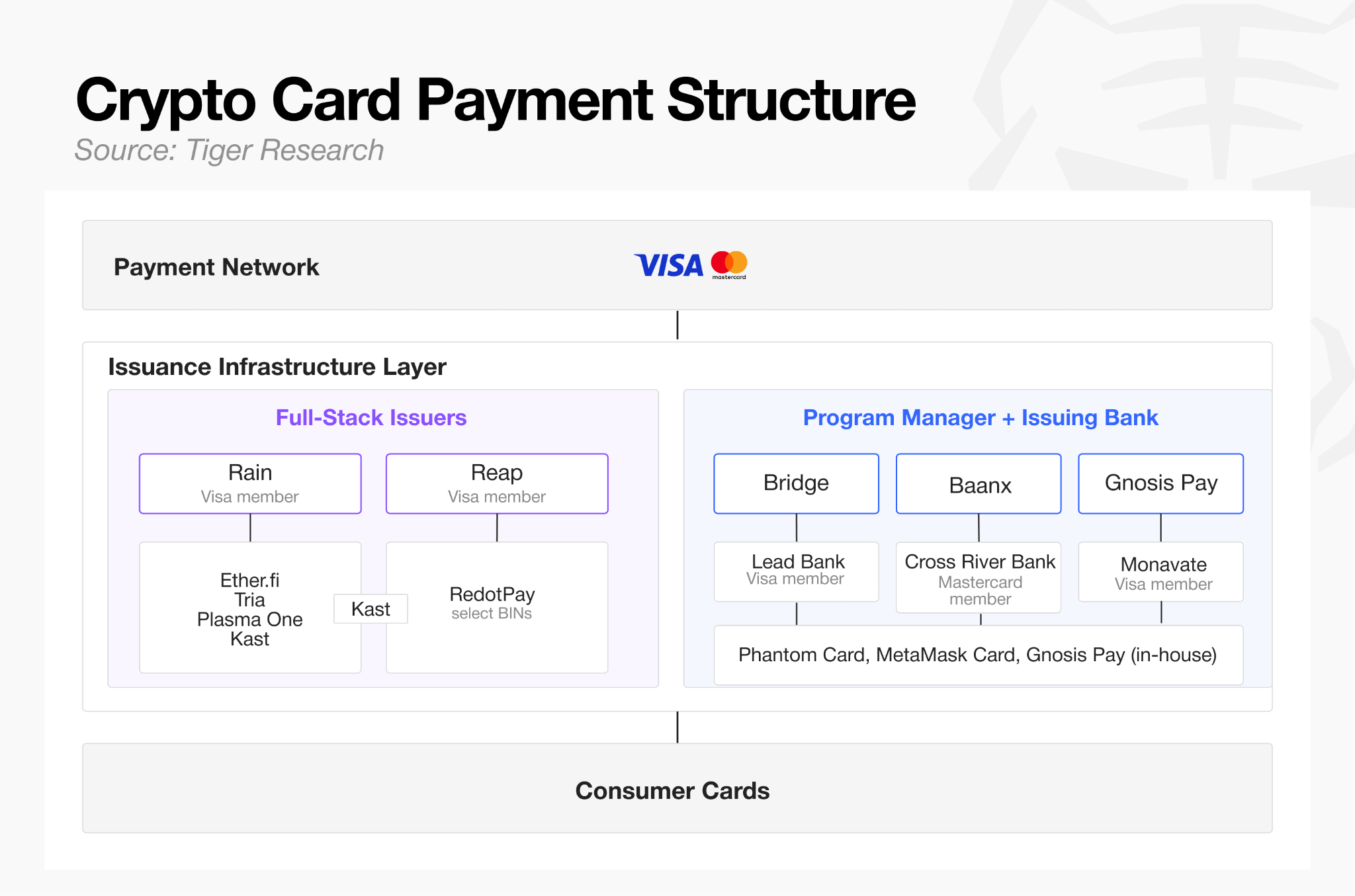

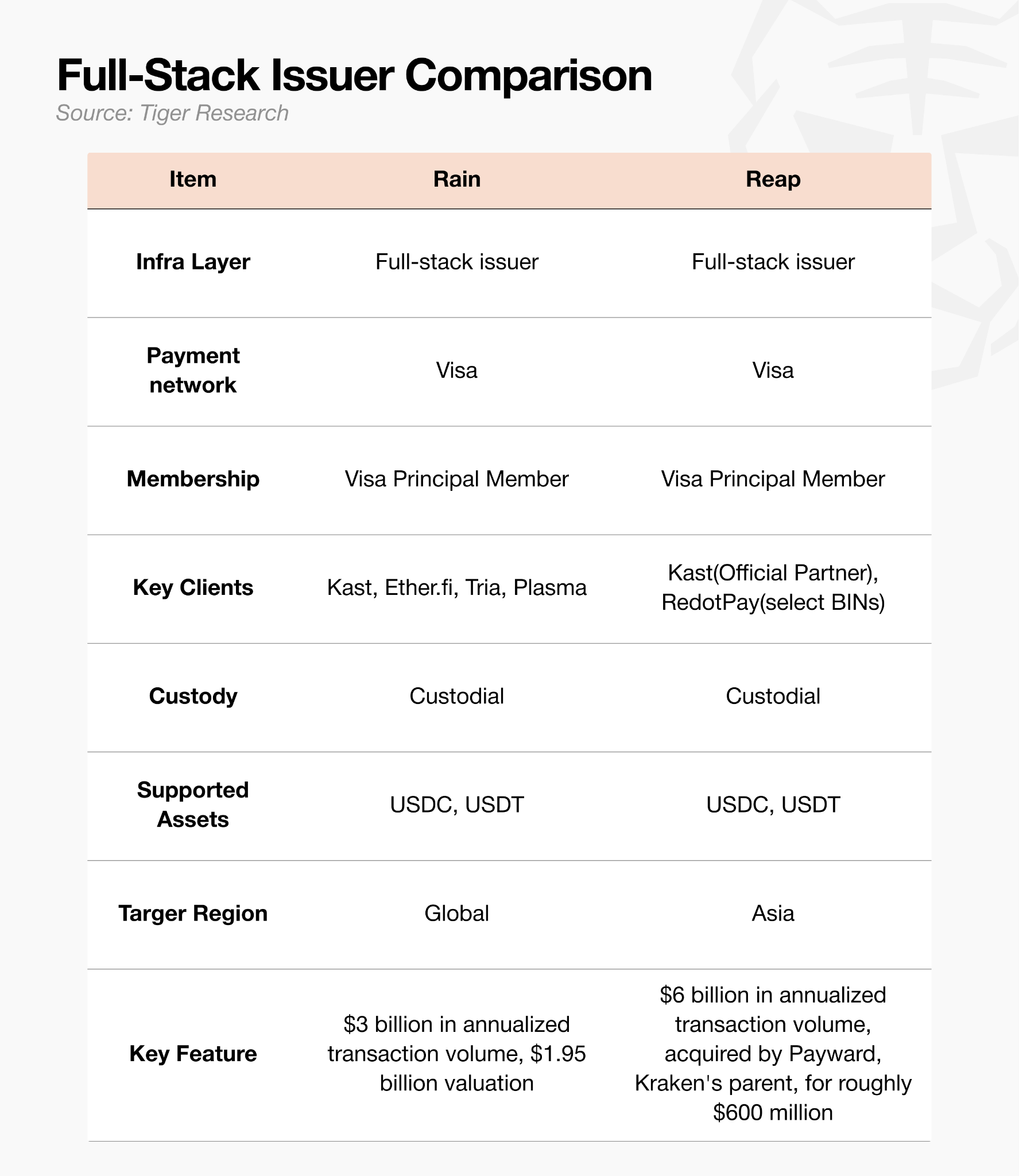

Visa and Mastercard, the familiar networks, also serve as the payment networks in the crypto card ecosystem. Below them sits the issuance infrastructure layer, which extends down to the consumer card. As shown in the figure above, two structures coexist within the issuance infrastructure layer. The first is the traditional two-tier structure, in which the program manager handling operations is separate from the issuing bank handling membership and settlement. The second is the full-stack issuer, such as Rain and Reap, which compresses the two into one.

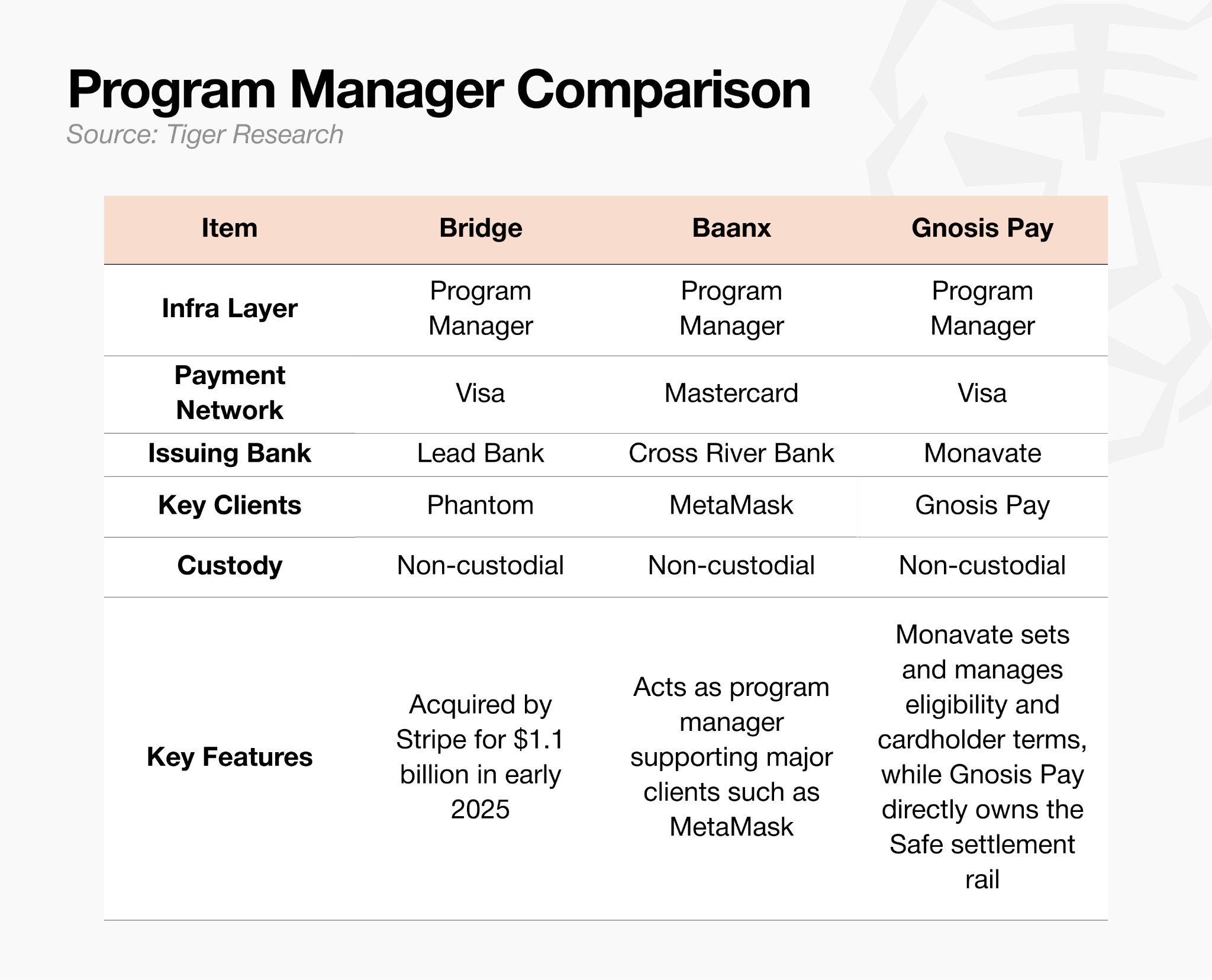

A comparison of three program managers that form a two-tier structure together with a bank follows.

Cards that appear to be separate brands on the surface converge on a small number of program managers once you look at the back end. Phantom Card, MetaMask Card, and Gnosis Pay are representative examples.

Card brands such as Kast, Ether.fi, Tria, and Plasma One also appear to be independent services, but in practice they run on a small number of infrastructure providers, as shown above. Rain in particular has most consumer cards connected to it.

Because the issuance infrastructure layer concentrates many brands in this way, traditional neobanks that already hold the relevant expertise are also entering the market.

Nium launched a stablecoin card issuance platform in March 2026 that can issue cards on both Visa and Mastercard. Other traditional fintech infrastructure players include Bridge, which Stripe acquired for $1.1 billion in early 2025, and BVNK, which Mastercard agreed to acquire for up to $1.8 billion in March 2026.

As a result, this layer has become one where full-stack issuers, existing program managers, and newly entering fintechs compete at the same time, and issuance alone is becoming harder to maintain as a barrier to entry.

Rain, for instance, differentiates itself with a daily settlement structure. Where established card companies settle over several days, Rain settles in stablecoins through Visa each day, which speeds up the cash turnover of issuers such as Ether.fi. It recently launched an Agent Control Layer that lets AI agents issue single-use virtual cards programmatically, extending its functions beyond basic card issuance infrastructure.

The issuance models that succeed will be those that go beyond providing payment infrastructure to secure and deliver differentiated functions that traditional infrastructure cannot provide quickly.

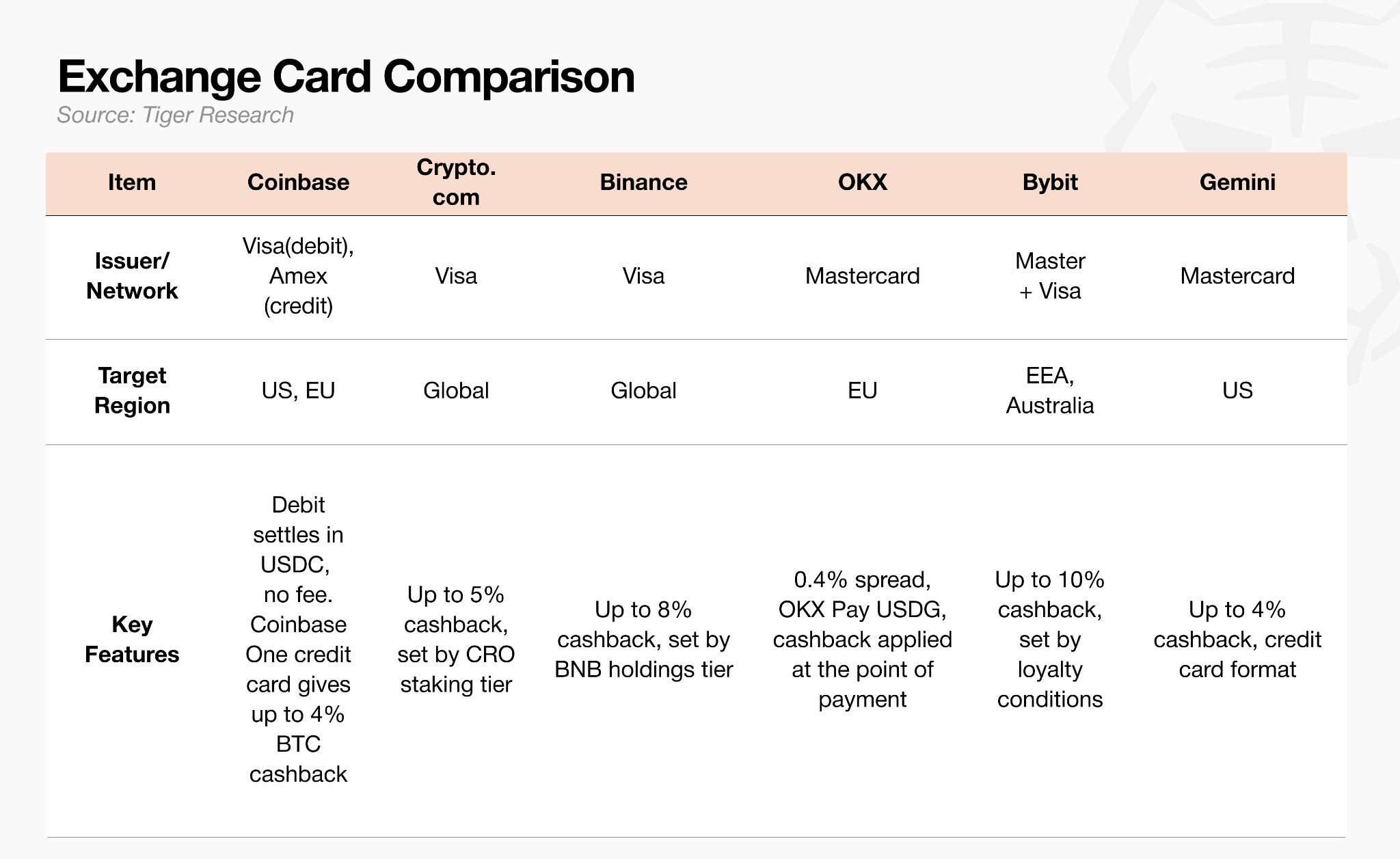

For exchanges, the card is less a direct revenue source than a tool for preventing user attrition. By connecting a card on top of an existing user base, balances, and transaction data, exchanges aim to keep users from leaving the platform. The actual revenue comes not from card payments themselves but from trading fees, lending, and the management of deposits.

Exchanges aim to use the card as an entry point into a financial super-app. Paying cashback in a proprietary token, however, carries the risk that the effective cashback rate becomes unstable as the token’s price fluctuates.

Switching to stablecoin cashback or interest on balances is cited as an alternative, but in the US, the GENIUS Act’s prohibition on interest payments stands as an obstacle to market expansion.

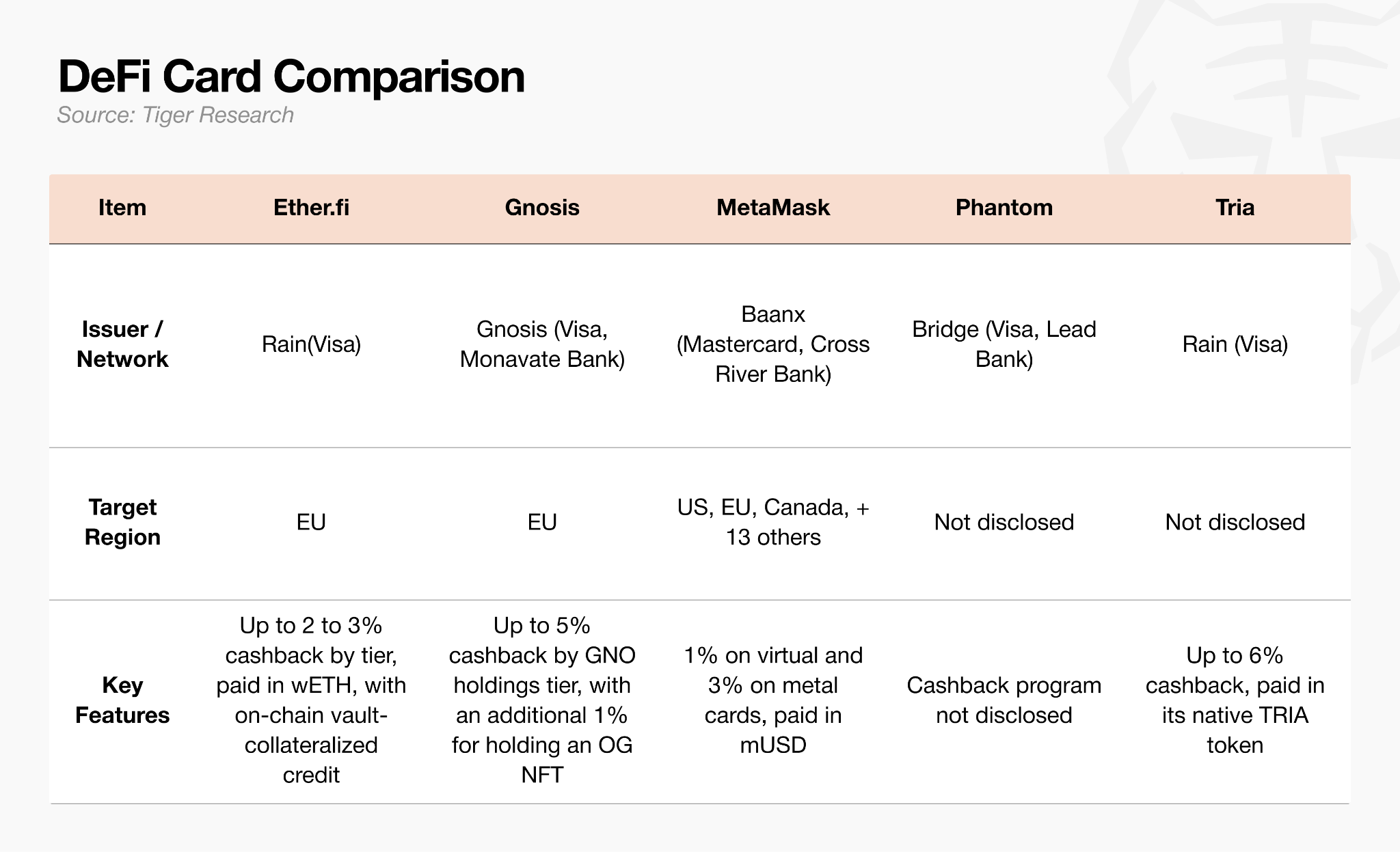

Built on the idea that the wallet itself is the account, this model holds assets directly on-chain rather than custodying them with a centralized exchange, and settles card payments from there. It provides a credit line while assets remain pledged as collateral.

The user, however, must manage a number of items directly, including setting up vaults, managing collateral, and tracking liquidation risk, which raises the cognitive cost involved. This is the main reason the DeFi-based model has formed a limited user base.

The DeFi-based model converts assets in the wallet into fiat in real time at the moment of payment and settles on that basis. Because this process runs on-chain, each transaction incurs gas fees (network fees), and on blockchains with low throughput or high congestion, fees can exceed the payment amount or approval can be delayed.

This is why MetaMask Card adopted Linea, its own layer 2 (L2) network. Cutting per-transaction gas fees to around $0.01 eased the fee burden and processing delays for small payments. Tria’s gasless top-up function takes a similar approach, with the platform covering the gas fee incurred at top-up, which removes the cognitive cost users would otherwise bear in choosing a network and calculating fees.

Until a user experience that satisfies both non-custodial asset holding and payment convenience is simplified to the level of a conventional debit card, however, the user base is likely to remain limited to users already familiar with crypto.

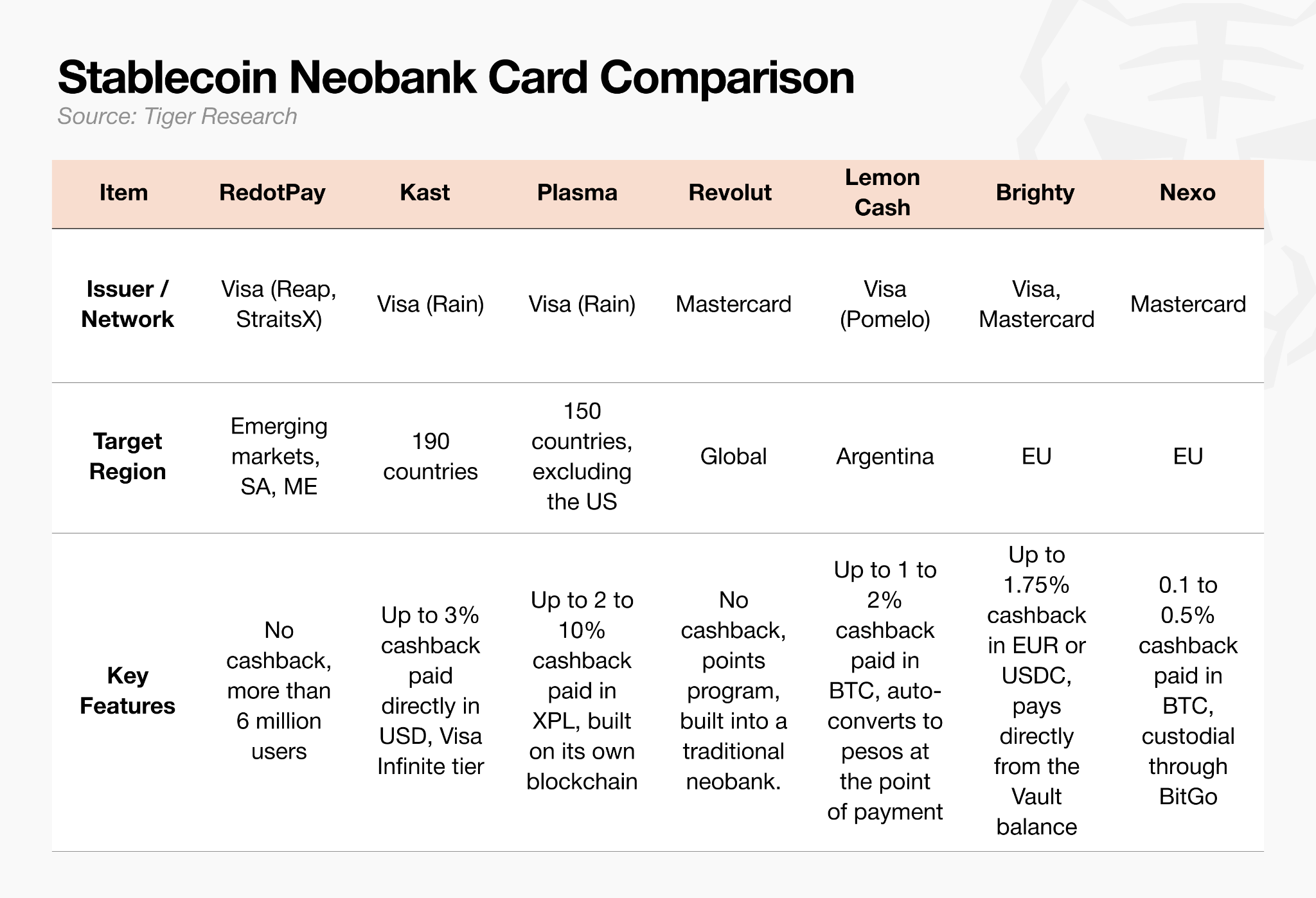

This model currently accounts for the majority of crypto card market volume and focuses on the function of the account rather than the card itself. It links foreign exchange, remittance, and savings functions to a stablecoin balance, with the card layered on top as a spending instrument. It holds a strong competitive position in emerging markets where local currency value is unstable, remittance costs are high, and dollar access is limited.

For this model to keep growing, it needs to move beyond an experience equivalent to a prepaid card, in which users buy stablecoins themselves and load the balance.

As the table shows, cashback strategy diverges by market position. RedotPay, with its dominant share, and Revolut, which carries a strong traditional fintech identity, do not run cashback programs at all, while later entrants such as Kast and Plasma One actively push USD or proprietary token cashback to attract users.

Benefits alone, however, cannot sustain crypto cards’ integration into everyday use.

As the precedents of traditional cards and neobanks show, a plain payment service has a clear ceiling on the value and profitability it can generate. These businesses turned profitable only after incorporating structures such as the primary-account concept and the deposit-lending margin into their business models. The crypto card sector now faces the same threshold, but global regulation, including the GENIUS Act in the US and MiCA in Europe, restricts the paths to paying interest and managing assets through stablecoins, which makes finding a breakthrough difficult.

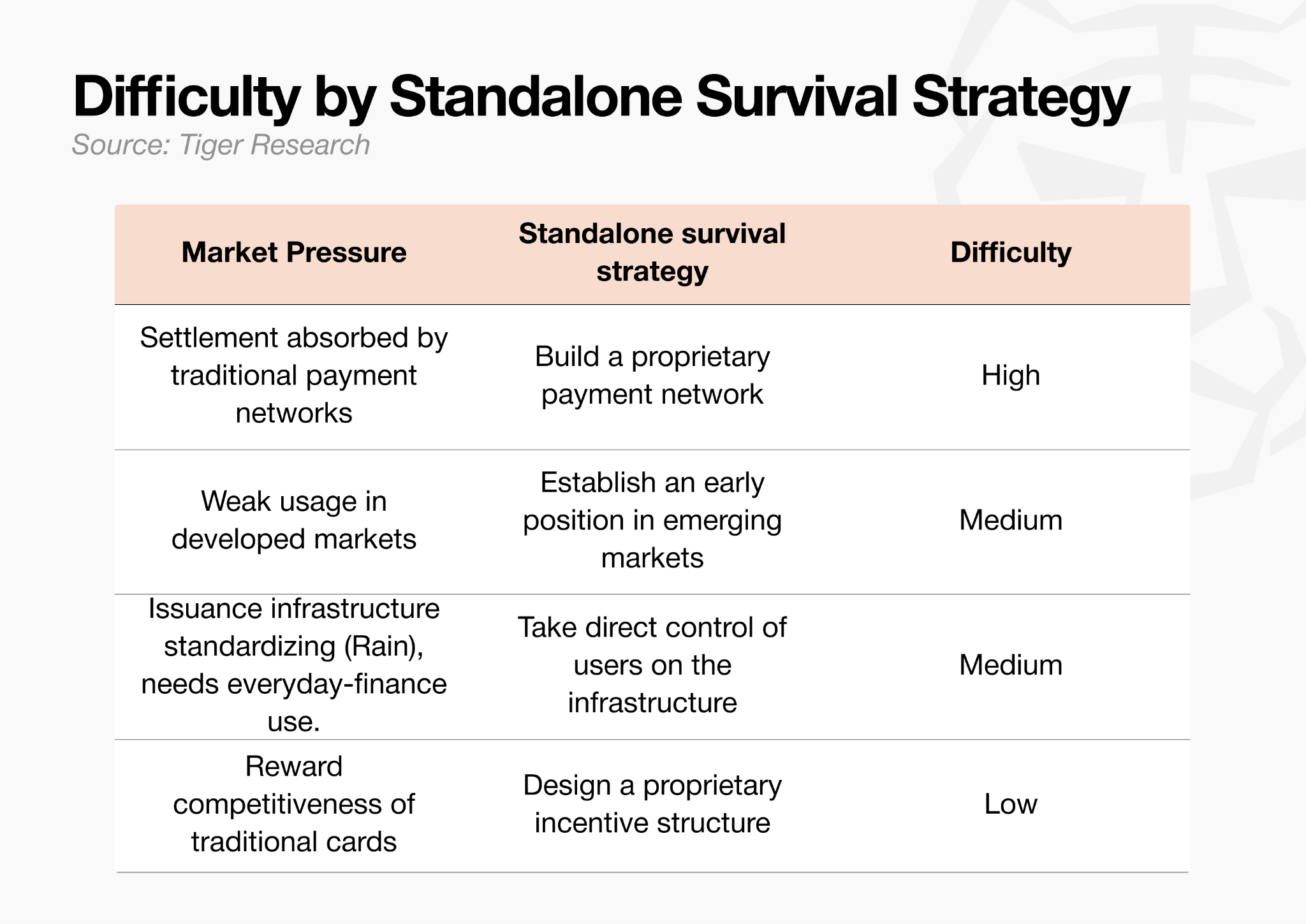

Reading this macro-level pressure in reverse yields three core strategic requirements that crypto card players will need to secure in order to survive going forward.

Players that fail to take direct control of the flow of funds, defend their use case in emerging markets, or build a proprietary account relationship that infrastructure providers cannot replace are likely to fall behind as market standards take shape.

After the introduction of the debit card, the players that ultimately came to lead the market were not those that issued the most cards but those that established an early position in the actual bank account. The crypto card sector today faces the same underlying question.

Crypto card players need to take direct control of the flow of funds upstream of the Visa payment step, secure an early position in niche markets, and capture consumer infrastructure in the way the primary bank account emerged in traditional finance. Doing so means establishing a global standard without an existing precedent to follow.

Crypto cards that fail to do so will remain not an essential element woven into daily life, but simply a prepaid card used by a limited group of people because the rewards happen to be somewhat better.

Read more reports related to this research.This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.