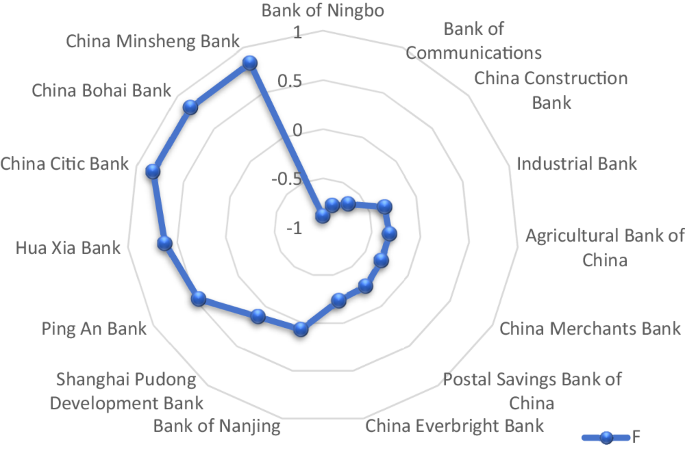

Factor analysis

Factor analysis was first developed by Charles Spearman, a British psychologist, who put forward in 1904 that the basic idea of factor analysis is to group the original variables. These variables must be grouped according to the correlation size so that the correlation between variables in the same group is higher, while the correlation between variables in different groups is lower. Each group of variables represents a basic structure, and an unobservable comprehensive variable called a common factor. For a specific problem studied, the original variable can be divided into two parts; a few unmeasurable linear functions or common factors, and special factors unrelated to public factors (Qin and Lin, 2021; Kim et al., 2020a, 2020b).

Suppose there are n samples, each sample observes p indicators, and there is a strong correlation between the p indicators. To facilitate research, the sample observation data is standardized, the standardized variable Xi (i = 1, 2, …, p) is used as the evaluation index, and Fj (j = 1, 2, …, m) is used as the common factor. εk (k = 1, 2, …, p) represents a special factor, and the specific model of the factor analysis is as follows:

$$\left\{\begin{array}{c}{X}_{1}={a}_{11}{F}_{1}+{a}_{12}{F}_{2}+\ldots +{a}_{1m}{F}_{m}+{\varepsilon }_{1}\\ {X}_{2}={a}_{21}{F}_{1}+{a}_{22}{F}_{2}+\ldots +{a}_{2m}{F}_{m}+{\varepsilon }_{2}\\ \ldots \ldots \\ {X}_{p}={a}_{p1}{F}_{1}+{a}_{p2}{F}_{2}+\ldots +{a}_{{pm}}{F}_{m}+{\varepsilon }_{p}\end{array}\right.$$

(1)

Where the common factor Fj (j = 1, 2, …, m) is mutually independent and unmeasurable. It is a factor that appears in the expression of the original variable. The special factors and the common factors are also independent of each other. aij is the factor loading. The greater its absolute value, the greater the degree of dependence between Xi and Fj.

Fragility indicators of the banking system

The key to accurately and comprehensively evaluating the fragility of the banking system lies in selecting evaluation indicators. A study by Gobert et al. (2002) on the issue of financial fragility looked at the indicator of the liquidity ratio of the banking system. In addition, they also argued that liquidity constraint was an important factor that triggered the crisis of financial institutions and led to financial fragility. Karadima and Louri (2020) pointed out that a high non-performing loan rate has aggravated the fragility of banks and has a strong negative impact on economic development. The capital adequacy ratio has become an important indicator of banks’ risk management and avoidance capabilities. Many countries are facing the threat of financial fragility to varying degrees while opening their financial markets. Therefore, from the perspective of safe operation, whether capital is sufficient has become a core issue of increasing concern to the banking industry. As Asteriou and Spanos (2018) mentioned, higher capital adequacy performance maintains the stability of the financial system. While banks are improving security and liquidity, profitability cannot be ignored. It can be represented by an indicator of return on average total assets. Therefore, this article adopts the average return on total assets, capital adequacy ratio, liquidity ratio, and non-performing loan ratio to measure the fragility of the banking system.

Fragility indicators of the financial system

Discussions on the fragility of the financial system have always received great attention from the theoretical community. Subdividing the financial system and monitoring financial risks from different subsystems is the core issue. Aikman et al. (2017) examine financial fragility from the stock, real estate, and bond market subsystems and highlight that there are many different views on the selection of specific evaluation indicators. Hamdaoui and Maktouf (2020) refer to the research of other scholars and use indicators such as international capital flow, inflation, real exchange rate, the ratio of money supply M2, and supervisory diffusion to measure financial fragility. Kaminsky (2006) mainly selected the main indicators, such as the proportion of fiscal deficit to GDP, the actual excess of M1, the proportion of M2 and foreign exchange reserves, and the ratio of foreign debt to imports. Additionally, Kaminsky subdivided the two subsystems of the stock market and bank credit among the model, making the model more comprehensive. According to the theory of the above scholars, combined with the characteristics of China’s financial system, this paper focuses on establishing the fragility evaluation model of the financial system from four subsystems: economic environment, financial market early warning, financial monitoring, and financial export-oriented. Among them, determining the boundary of some evaluation indexes and the weight setting of subsystems refers to the common international standards and foreign experts (Graciela L Kaminsky, 2006). Other indicators are based on historical data to get the average value and then determine the index range according to the degree of deviation from the average value. Table 1 provides specific information.