Interest rate headlines are back in focus as the Federal Reserve signals a possible pause or slowdown in hikes, and that matters for rate sensitive areas like Real Estate and Utilities. With mixed economic data and a cautious central bank, some stocks in these sectors may see sentiment shift as investors rethink income, value, and balance sheet risk. This article looks at 3 stocks from a Rate Sensitive Sectors screener that appear positively exposed to the current Fed stance. It is intended to help you decide whether they might fit, or might not fit, into your watchlist as policy expectations evolve.

Balanced Commercial Property Trust (LSE:BCPT)

Overview: Balanced Commercial Property Trust is a UK listed real estate investment trust that owns a diversified portfolio of prime UK commercial properties, aiming to provide investors with regular income plus the potential for capital and income growth. It offers access to a broad mix of institutional quality assets without requiring investors to buy individual buildings directly.

Operations: The trust generates around £55.8 million in revenue from property investment in the United Kingdom.

Market Cap: £672.1 million

Balanced Commercial Property Trust sits at the crossroads of income investing and interest rate sensitivity, so a more patient Federal Reserve stance on rate hikes can matter for both its borrowing costs and how the market values its UK property portfolio. The stock is currently priced below one DCF based fair value estimate. Analysts have projected that earnings could improve and move into profitability over the coming years, although past returns on equity have been weak and losses have widened. Funding risk is a clear consideration, as the trust relies entirely on external borrowing. However, board independence is strong, and recent debt refinancings and occupancy trends indicate a disciplined approach that some investors may feel is not fully reflected in the current share price.

Balanced Commercial Property Trust looks like a classic mispriced income story, with market skepticism on funding risk potentially masking what a fresh 2 key rewards and 1 important warning sign could reveal about the real trade off in this situation.

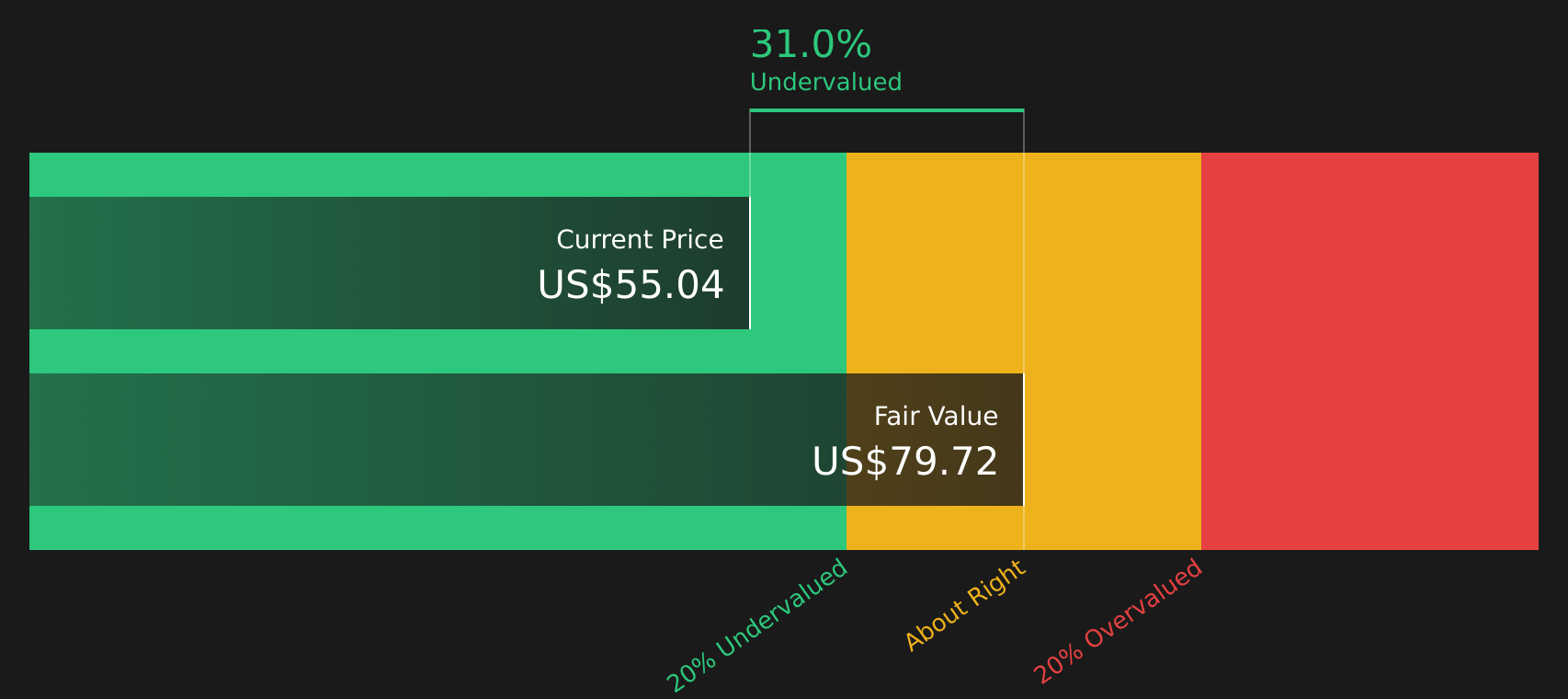

American Healthcare REIT (AHR)

Overview: American Healthcare REIT is a self managed real estate investment trust that owns and operates a large portfolio of senior housing, skilled nursing facilities, outpatient medical buildings, and other healthcare properties across the U.S. and selected international markets, aiming to generate income from rent and healthcare real estate operations. It combines property ownership with on the ground operating capabilities under structures such as RIDEA.

Operations: American Healthcare REIT generates most of its roughly US$2.37b in revenue from Integrated Senior Health Campuses (about US$1.84b), with additional contributions from SHOP (US$369.1m), Outpatient Medical (US$123.7m), Triple net leased properties (US$39.5m), and a small segment adjustment.

Market Cap: US$10.12b

American Healthcare REIT sits in the middle of the Fed’s softer tone on rates, as interest costs, debt structure and property values all react quickly for a pure play U.S. healthcare REIT. The company is already profitable, with what analysts describe as strong earnings growth expectations and revenue of roughly US$2.37b. Even after a recent equity raise that diluted shareholders but strengthened the balance sheet and helped fund an acquisition pipeline, it is trading below at least one estimate of its future cash flow value. At the same time, a very high P/E, weak interest coverage and reliance on external borrowing keep funding risk firmly on the table, which is the trade off rate sensitive investors may want to weigh more closely here.

American Healthcare REIT’s combination of profitability, a recent equity raise and rate sensitivity makes the valuation debate hard to ignore. Reviewing the full 3 key rewards and 2 important warning signs (1 is major!) could surface one crucial twist investors are missing.

FirstService (TSX:FSV)

Overview: FirstService is a North American property services group that manages residential communities and provides essential services like restoration, roofing, painting, inspection and custom storage for residential and commercial clients across the United States and Canada.

Operations: FirstService generates about US$3.3b from FirstService Brands and US$2.3b from FirstService Residential, with roughly US$5.0b of revenue coming from the United States and US$584.3m from Canada.

Market Cap: CA$9.27b

FirstService operates in rate sensitive sectors, but its business is tied to everyday property upkeep rather than speculative development. As a result, demand for repairs, restoration and community management can remain connected to ongoing maintenance needs even as financing conditions shift and the Federal Reserve indicates a slower pace of hikes. Reported earnings grew 24% in the past year with margins slightly higher, and management is still adding contracts, acquisitions and leaders across key regions, from Florida luxury communities to expansion in Colorado and the Midwest. At the same time, a high P/E multiple, meaningful debt and reliance on acquisitions mean investors are paying a premium for execution. The key consideration is whether that premium is still justified as conditions ease.

FirstService’s rising earnings and premium P/E suggest investors may be missing a key angle on its growth run. Review the analyst forecasts for FirstService to see how that premium could tie into one overlooked risk.

The three stocks covered here are just a starting point. The full Rate-Sensitive Sectors (Real Estate and Utilities) screener highlights 19 more companies with equally compelling rate sensitive stories that could shift how you think about Real Estate and Utilities. Use Simply Wall St to identify, analyze and filter for the specific catalysts, balance sheet traits and dividend narratives that matter most to you, so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If American Healthcare REIT or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives With Real Curiosity?

Fresh stock ideas do not stay under the radar for long, and momentum often shifts before the crowd catches it. Use these curated lists now to explore opportunities early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com