Employee reviews can reveal hidden organizational strength LLMs can measure firm-specific intangible assets at scale CEO changes may weaken these assets before losses become visible

In 2022, organizational capital accounted for around 30 percent of firms’ total intangible investments, surpassing investments in research and development, software, brands or design. Still, with few exceptions, firms are unable to detect whether their intangible capital is increasing, decreasing, or eroding following a change in leadership; the standard deviation of the difference between the actual change in intangible capital and the expected change in intangible capital is equal to 0.27. This discrepancy matters because a large proportion of firm-specific intangible assets influence business value in currently relevant ways: trust and shared routines, internal knowledge, defined decision rights and co-location of information. They cannot be captured as capital in existing books of account. Many remain unrecorded in firms’ balance sheets and their loss might only become apparent when employees depart, forecasts deteriorate, projects are shelved, or consumers complain. There is now a way forward. Large language models can automatically analyze employee reviews at scale, transforming repeated cues of workplace dysfunction into a persistent metric. The question for policy is no longer whether firm-specific intangible assets exist. It is whether boards, investors and regulators will measure them before financial damage makes the answer self-evident.

Firm-Specific Intangible Assets Need a Better Measure

The argument for a new measure starts with a fundamental disconnect. Intangible investment was estimated to be $7.6 trillion in 2024 across the economies covered by the World Intellectual Property Organization. Between 2008 and 2024, it grew 3.7 times as quickly as tangible investment. Organizational capital alone accounted for 30 percent of total intangible investment in the most recent asset-level classification. Yet the national accounts exclude many such assets from their central asset category. And company accounts apply tightly defined recognition rules to internally generated intangibles. This is not an error in accounting. It highlights a core difficulty that internal know-how is very difficult to tease out, price and sell. However, the consequence is still serious. The rapidly expanding part of the economy is being measured with methods that were mainly designed for physical capital. Companies can account for expenditure on training, software, consultants and administration, but it is difficult for them to record whether such expenditure produced increased coordination, improved judgment and a more effective firm.

Traditional proxies do not answer that question. Selling, general and administrative may measure some effort to develop internal capabilities, but there is no reason to see expenditure as a success. Paying more just makes a firm harder to run. Staff surveys give more nuance yet are private, inconsistent and easily redesigned when the results are grim. Profit can be published years later. Earnings, productivity and value show the net result of strategy, the climate and prior decisions; they do not reveal how healthy individual, idiosyncratic intangible resources are. The best way is to understand that organizational strength is an accumulated stock that shows itself in mundane words; workers watch for clarity of decisions, teams transfer knowledge, managers meet promises and good ideas float upward. The indicators forecast a balance sheet penalty. They also change gradually, allowing deep operating capacity to be distinguished from a bad week or a hated policy. The question, therefore, should not be what a firm spends, but what its employees repeatedly see.

Employee Reviews Can Reveal Firm-Specific Intangible Assets

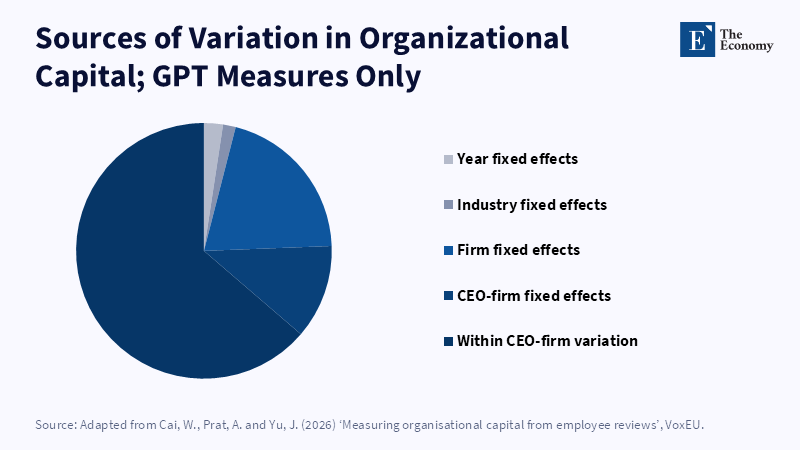

A new measure derived from over 1 million Glassdoor reviews provides evidence of how this can work. Its first stage employs word embeddings and synthetic reviews generated with ChatGPT to measure language associated with organizational capital. The second uses the embeddings and synthetic reviews as input to generate a firm-year score. The construct is not a happiness index. It is substantially more correlated with employees’ attitudes about culture and management than with pay or work-life balance. Firms with higher scores are also more profitable and valuable. Most importantly, the score acts like a persistent asset. It varies over time, but slowly, not like a news cycle. The slow variation dovetails with the notion that firm-specific intangible resources are cultivated through routines, trust, shared knowledge and incremental management decisions. The slow variation also provides boards with a key dimension: a sharp drop in mood might require an immediate local intervention, while a low but steady decline in organizational language might indicate system degradation.

Other evidence emphasizes the importance of the employee voice. An early 2025 study combined 1.5 million Glassdoor ratings and found that stronger employee perceptions of culture were associated with more accurate management forecasts. A ChatGPT-based proxy for the internal information environment accounted for roughly 47 percent of that association. This is a core finding. Forecast accuracy hinges on the unobserved fact that must reach the chief executives without delay or distortions. To the degree that weak reporting, fear, or poor coordination is described by the members of staff, it may not stay with the human resources professionals. It can migrate into the knowledge of the top managers and then to their communications with the investors. A separate 2025 investigation documented that optimistic employee forecasts predicted annualized abnormal stock returns of 8-11 percent. Those projections do not establish that the reviews should be the benchmark of market worth; they confirm only that the large numbers of human resources staff, after all, can harbor information that conventional reports have yet to know. Firm-specific intangible assets, therefore, are not nice-to-haves. They shape the information flows on which concrete decisions rely.

This allows research to scale up good evidence. Human rating analysts can read hundreds of reviews, but large companies produce hundreds of thousands across countries, roles and years. Manually coding becomes slow and not always reliable. In controlled text-annotation experiments, ChatGPT outperformed crowd-worker accuracy by 25 percentage points, roughly averaged across four datasets. That does not indicate an LLM is ready to be used without verification. The implication is that the cost barrier to structured review analysis has dropped. Product teams already employ similar models to sort app store reviews, identify common complaints and cluster themes. The same approach could be applied here with modest adjustments for the interests at stake for workers, managers and investors. A reasonable system would use explicit definitions, repeated inputs, held-back human labels and regular validation. It would also provide confidence intervals instead of a single, rather polished score. The aim is not to let ChatGPT judge companies. The aim is to employ language models as rigorous scanners of the abundant information firms already produce.

CEO Change Is an Intangible Asset Event

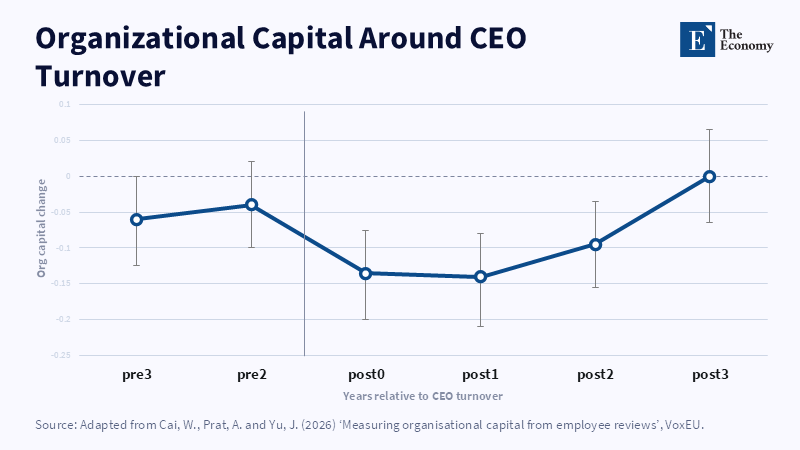

There is a compelling reason to try to value firm-specific intangible assets: leaders influence them. Research by Glassdoor suggests that CEO-related variation is responsible for about one-third of organizational capital. The figure drops immediately after CEO turnover, sustaining at a lower level for two years before climbing again. This evidence necessitates a new way of evaluating a leader. A CEO’s influence is not constrained to product launches, divestitures, reorganizations and financial reengineering. The leader also has implications for how people formulate goals, divide risk, resolve differences and determine what can be said. While such effects may be difficult to interpret, they are not intangible. They influence how quickly actions are directed and how effectively information is processed. A modern CEO can redesign a strategy without maintaining the processes essential for its implementation; the corresponding losses may be attributable to the former’s direction, not the latter’s ineptitude. Performance measures, including a rising number of missed common objectives, failing estimates and uninvited retrenchments, may turn boards’ affection for change into a fondness for impotence.

Nor does this support any simple rule of thumb limiting CEO change. Turnover may be required when circumstances are worsening. A new chief executive, or even a new manager, might have to eliminate destructive routines or replace a closed mindset. In short, there is a different point at issue here. Transition has a hard-to-measure cost that will have to be managed with care and it has a significant one. Studies based on staff records of over 200,000 white-collar workers, 30,000 managers and 100 countries illustrate the point. Better managers make each worker-job pairing better and when their impact endures well beyond their departure, manager quality will be inherently present in many detailed decisions of allocation, not just-or even-macro strategy. The CEO affects the framework in which those managers operate. Restructuring may disrupt productive relationships between roles and personnel and the knowledge they hold. Any serious succession planning should identify those relationships before the new chief assumes power. It should go on to monitor review themes, internal transfers, lost opportunities, errors in output prediction and hurdles to decision-making. An assessment of the CEO’s performance should focus on whether existing firm-specific intangible assets were saved, reconstructed, or needlessly destroyed.

A Governance Standard for Firm-Specific Intangible Assets

The crux of the main objection is that online employee reviews are biased. That is correct. Reviewers are self-selected. Most reviews present extreme experiences, while those feeling moderately satisfied or dissatisfied are less likely to post. Companies may incentivize positive reviews, or former employees might post in order to get back at the company. Interface decisions influence content as well. Nevertheless, bias alone doesn’t render the data worthless. Bias compels careful design and reporting of practices. A study of over 116,000 reviews on Glassdoor showed that the platform’s give-to-get policy cut one-star reviews by 3.6 percentage points and five-star reviews by 2.1 points. It also resulted in more moderate feedback. Academic evidence suggests that public reviews can alter company behavior. Following a new review on Glassdoor, companies enriched employee and diversity practices, with larger effects for companies receiving a negative review. Therefore, the review data exhibit both noise and real influence. A credible index should weigh current and past employees separately, have a minimum number of reviews, identify upward trends and analyze differences across job functions, locations and sites.

The second objection is that a score might be gamed or abused. And this problem is worse still when an LLM provides a neat number for a flow that’s inherently messy. Was an investor’s shareholder vote a resignation? Did a board misdeed or a minor fall? Did an analyst put a match to the books? Did a marketer try to get employees to praise their products? But these are not reasons to drop measurement. There are reasons for a governance standard. And the new score should be a monitored metric rather than a recognized asset or stand-alone valuation function. Its sources should be stable or continuously recalibrated in a transparent manner, so that training data and classification categories are visible and to the extent that various tests against staff satisfaction surveys, turnover, internal transfers, accident reporting, forecasting mistakes and business performance can be measured. Each individual review should have passed through blind blocks of suppressible subgroups to avoid exploitation by the person being rated. Independent reviewers should screen for language, gender, regional address and functional bias. A firm-specific subset of intangibles only becomes a valuable indicator when those making use of it understand how it was created and how accurate and stable the estimate is and where its limits are.

Practical policy step: a voluntary reporting scheme before any formal accounting rule. Large listed firms could publish a brief organizational-capital statement with three parts: what direction of change, what main drivers and what controls for testing the measure. As a minimal presentation, it must not reveal raw reviews and it must not artificially pound out a precise monetary figure. For example, it should say if communication, trust, collaboration and internal learning have gained or lost and if the result conforms with other evidence. Boards each quarter should receive a more comprehensive private dashboard. Investors should get a relatively stable public series each year. Regulator and standard setter could then compare methods. This proposes a rise in minimum standards. It cuts through to compare criteria. It builds on the limits of IAS 38, which factors internally generated ‘goodwill’ and many other presumed assets away because they are too difficult to recognize and measure. It also addresses a lack of clear information. More than 60 percent of intangible investment remains unmeasured in implied standards. But better disclosure can begin long before the time of perfect valuation.

Organizational capital is already the largest component of intangible investment and yet many firms run it with an inadequate summary. That no longer makes sense. Employee surveys may be flawed, machine learning models may be flawed, but together they can help show sharp shifts in intangible capital that traditional reporting misses. The aim is not to find out the perfect measure of good working conditions, but to identify when trust, knowledge and collaboration are going up and down. Attentive boards should treat a CEO change as an intangible capital event. Investors should demand evidence of internal operational strength. Regulators should enable common standards around privacy and validation tests. Company-specific intangible assets spell the difference between planned strategies and realized ones. An online measurement will not always make things certain, but it will increasingly help ensure that the best part of the firm appears in time to avoid turning into a line item.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Brown, A.B., Wang, V.X. and Zhou, A. (2025) ‘Employee perceptions of corporate culture and management forecast accuracy: Evidence from Glassdoor and ChatGPT’, Accounting Horizons, advance online publication.

Cai, W., Prat, A. and Yu, J. (2026a) ‘Measuring organizational capital’, Journal of Accounting Research, forthcoming.

Cai, W., Prat, A. and Yu, J. (2026b) ‘Measuring organisational capital from employee reviews’, VoxEU, 26 June.

Chamberlain, A. (2017) ‘Give to get: A mechanism to reduce bias in online reviews’, Glassdoor Economic Research, 11 October.

Gilardi, F., Alizadeh, M. and Kubli, M. (2023) ‘ChatGPT outperforms crowd-workers for text-annotation tasks’, Proceedings of the National Academy of Sciences, 120(30), e2305016120.

Grewal, A.K., Wunsch-Vincent, S., Jona-Lasinio, C., Bontadini, F., Corrado, C., Haskel, J., Iommi, M., Jaccoud, F., Poquiz, J.L. and Serberis, P. (2025) World Intangible Investment Highlights 2025. Geneva and Rome: World Intellectual Property Organization and Luiss Business School.

International Accounting Standards Board (n.d.) IAS 38: Intangible Assets. London: IFRS Foundation.

Minni, V. (2026) ‘Making the invisible hand visible: Managers and the allocation of workers to jobs’, The Quarterly Journal of Economics, advance article, qjag017.

Viswanathan, S. (2023) ‘How I used ChatGPT to perform user review analysis from appstore!’, Bootcamp, 21 May.