As Asia’s markets navigate a landscape marked by technological shifts and economic challenges, investors are increasingly focusing on companies that demonstrate robust growth potential coupled with significant insider ownership. In this context, stocks with strong insider stakes can offer a unique perspective on confidence in the company’s future prospects, especially amidst the broader regional technology sell-off and evolving monetary policies.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Shanghai Biren Technology (SEHK:6082) | 11% | 118.1% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.3% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| Great Microwave Technology (SHSE:688270) | 21.1% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.2% | 38.2% |

| Fulin Precision (SZSE:300432) | 10.3% | 60.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.0% | 40.4% |

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Growth Rating: ★★★★★☆

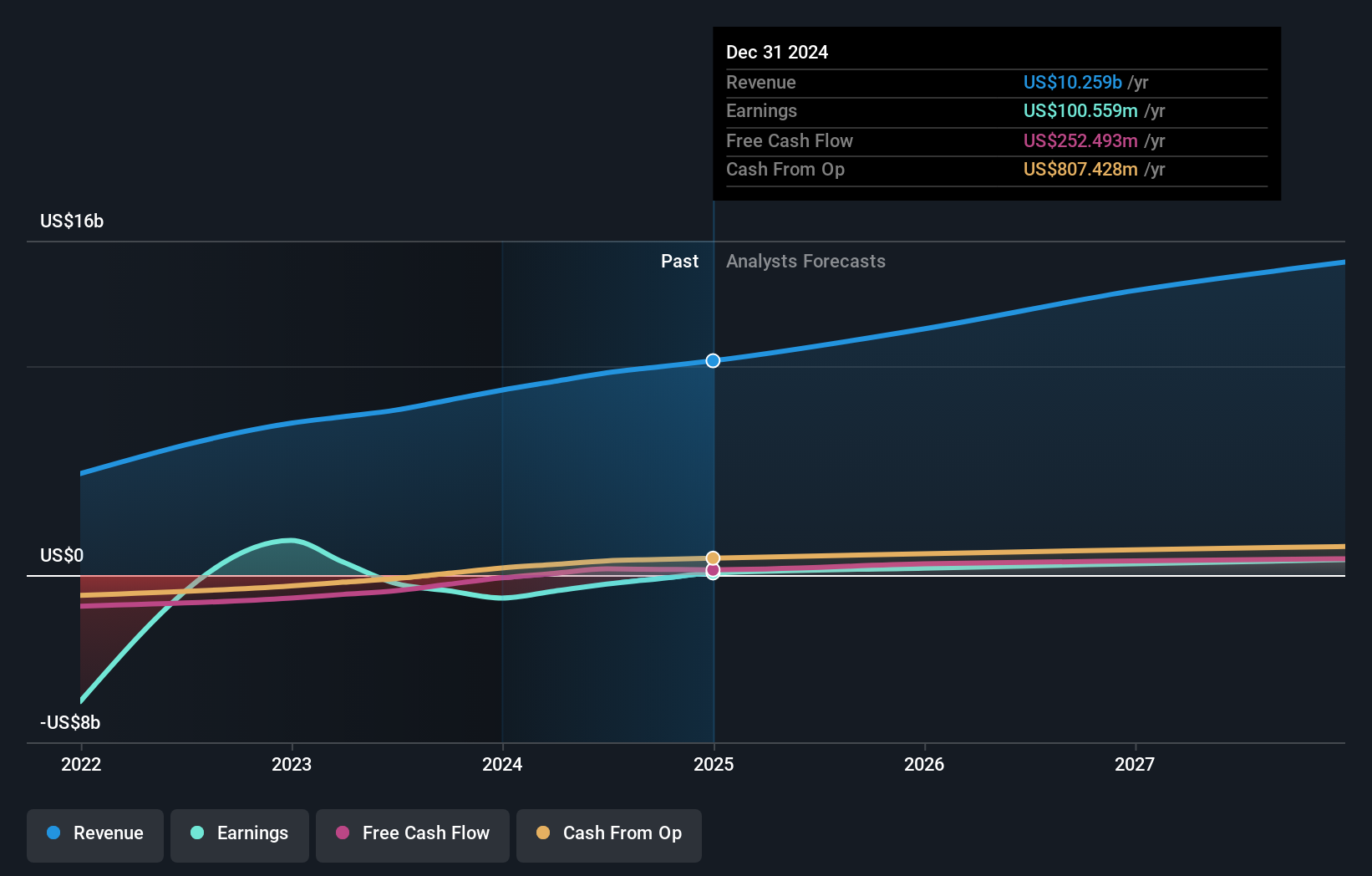

Overview: J&T Global Express Limited is an investment holding company providing integrated express delivery services across several countries including China, Indonesia, and Brazil, with a market cap of HK$80.89 billion.

Operations: The company’s revenue primarily comes from its transportation segment, specifically air freight, which generated $12.16 billion.

Insider Ownership: 17.5%

Earnings Growth Forecast: 34.1% p.a.

J&T Global Express is experiencing robust growth, with earnings expected to rise significantly by 34.11% annually over the next three years, outpacing the Hong Kong market. Its revenue growth forecast of 15.8% per year also surpasses market expectations. Despite trading at a substantial discount to its estimated fair value, J&T’s recent addition to the Hang Seng Index and strategic investor participation through private placements highlight strong insider confidence and operational momentum across global markets.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Horizon Robotics is an investment holding company that offers automotive solutions for passenger vehicles in China, with a market cap of HK$59.45 billion.

Operations: The company generates revenue primarily from its automotive solutions segment, which accounts for CN¥3.56 billion, and also earns CN¥201.08 million from non-automotive solutions.

Insider Ownership: 15.9%

Earnings Growth Forecast: 76.7% p.a.

Horizon Robotics is forecast to achieve profitability within three years, with earnings expected to grow 76.71% annually, significantly outpacing the Hong Kong market. Trading at 48.3% below its estimated fair value, it shows promising potential for investors. Recent share repurchases authorized by shareholders aim to enhance net asset value and earnings per share. Despite low insider buying in recent months, substantial insider ownership remains a key factor in its growth trajectory.

Simply Wall St Growth Rating: ★★★★★★

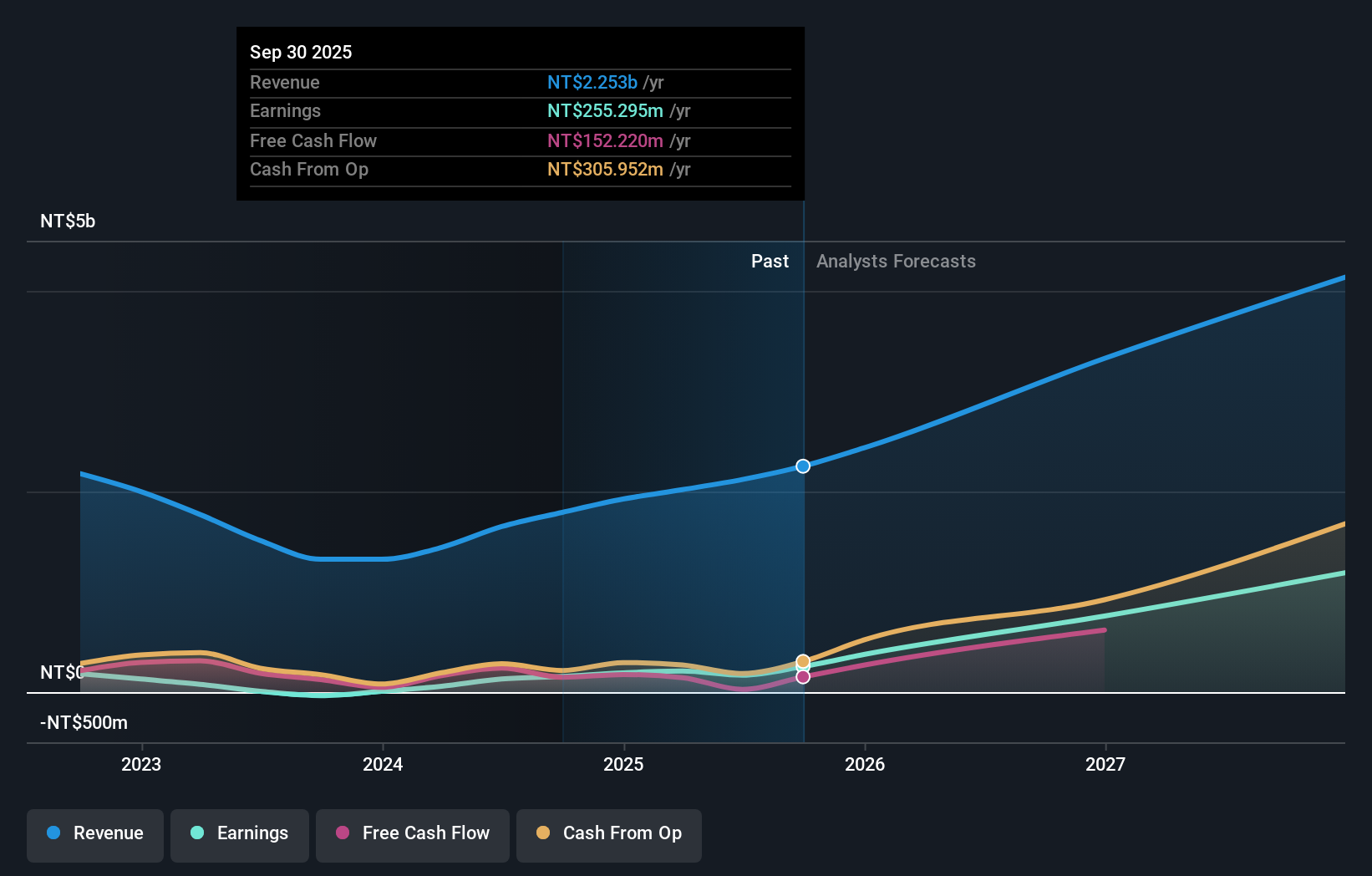

Overview: Nan Juen International Co., Ltd. operates in the research, development, manufacturing, and trading of steel ball guide rails across various global markets including the United States, Asia, Europe, and Africa with a market cap of NT$51.84 billion.

Operations: The company’s revenue primarily comes from the manufacture and sales of steel ball slide rails, totaling NT$2.80 billion.

Insider Ownership: 35.3%

Earnings Growth Forecast: 50.8% p.a.

Nan Juen International shows strong growth potential with its earnings forecast to increase 50.8% annually, outpacing the Taiwan market. Recent Q1 results reflect a significant rise in sales to TWD 866.89 million and net income of TWD 235.17 million, highlighting robust performance. The company’s revenue is expected to grow at 35.1% annually, well above market averages, while trading significantly below its estimated fair value further enhances its investment appeal despite recent share price volatility.

Next Steps

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we’re here to simplify it.

Discover if Horizon Robotics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com