As Australian traders anticipate a fresh start with the new financial year, geopolitical tensions in the Middle East continue to cast uncertainty over market stability, even as indices show signs of recovery. In such an environment, growth companies with high insider ownership can be particularly appealing, as they often indicate confidence from those who know the business best and may provide resilience against broader market volatility.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Torque Metals (ASX:TOR) | 21.2% | 94.2% |

| Starpharma Holdings (ASX:SPL) | 21.8% | 91.8% |

| SKS Technologies Group (ASX:SKS) | 28.2% | 39.5% |

| Santana Minerals (ASX:SMI) | 12.1% | 145.2% |

| Pinnacle Investment Management Group (ASX:PNI) | 25% | 21.1% |

| Forrestania Resources (ASX:FRS) | 39.6% | 113.3% |

| Clarity Pharmaceuticals (ASX:CU6) | 13% | 43.6% |

| Austral Resources Australia (ASX:AR1) | 20.3% | 38.7% |

| Adveritas (ASX:AV1) | 17.6% | 108.4% |

| Advanced Energy Minerals (ASX:AEM) | 35.1% | 48.5% |

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: HMC Capital Limited, along with its subsidiaries, owns and manages real estate-focused funds in Australia and has a market capitalization of A$1.24 billion.

Operations: The company’s revenue segments consist of A$48.90 million from Digital, A$83.30 million from Real Estate, and A$41.80 million from Private Credit, with a Segment Adjustment of A$28.40 million.

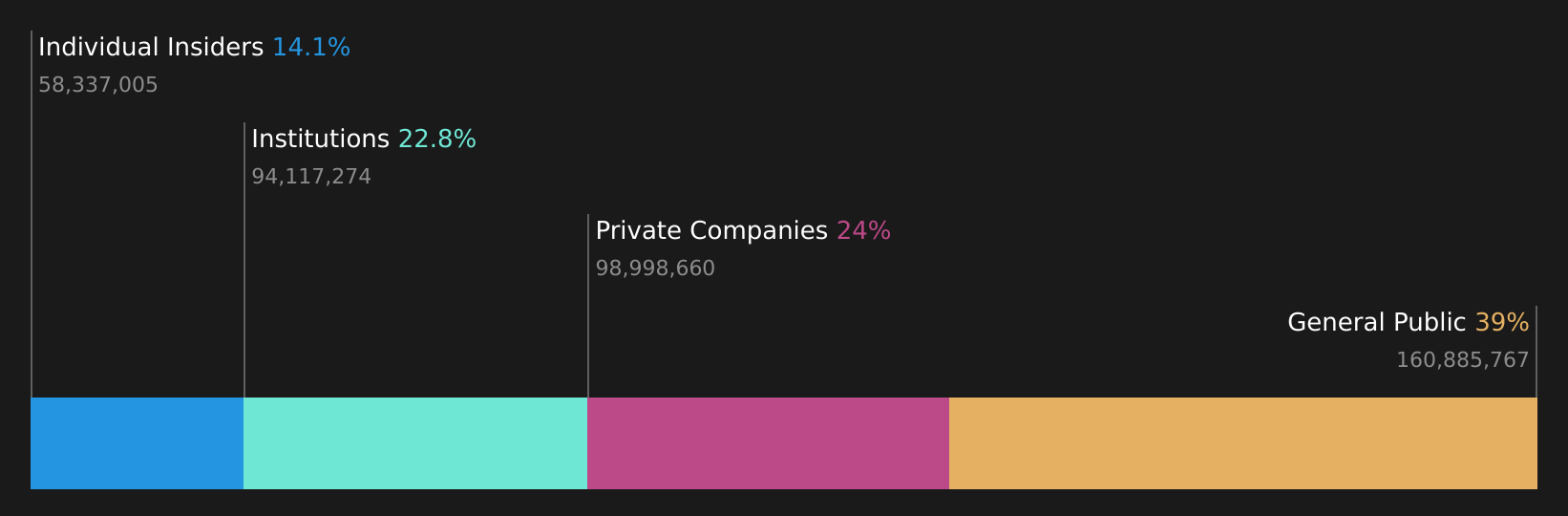

Insider Ownership: 14.1%

HMC Capital is forecast to achieve above-average market growth by becoming profitable in the next three years, with earnings expected to grow at 26.46% annually. Its revenue is projected to increase by 9.7% per year, outpacing the Australian market’s average growth rate of 6.1%. However, its Return on Equity is anticipated to be low at 5.8%, and its dividend yield of 3.99% lacks coverage from earnings or free cash flows.

Simply Wall St Growth Rating: ★★★★★☆

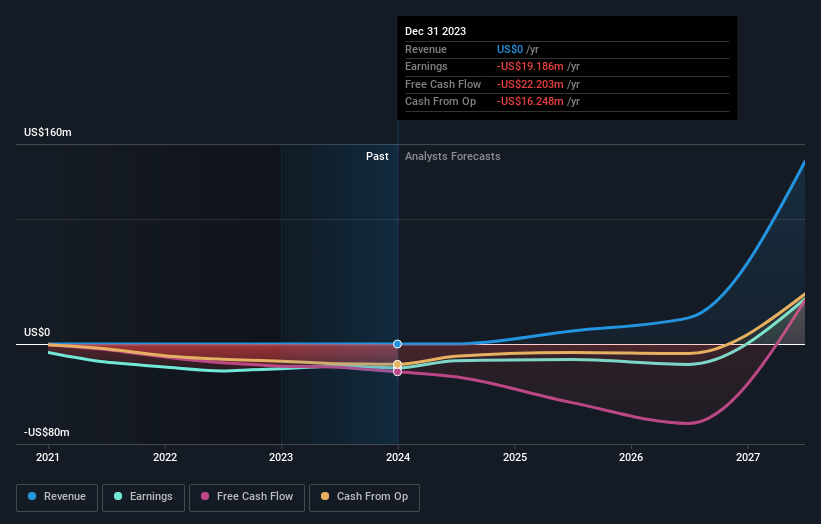

Overview: IperionX Limited focuses on developing mineral properties in the United States and has a market capitalization of A$1.31 billion.

Operations: Revenue information for IperionX Limited is not available in the provided text.

Insider Ownership: 17.4%

IperionX is poised for substantial growth, with revenue forecasted to grow significantly faster than the Australian market. Despite being currently unprofitable, it is expected to achieve profitability within three years, outpacing average market profit growth. Insider confidence is evident as more shares have been bought than sold recently. The acquisition of Covia Solutions’ assets enhances IperionX’s strategic position in the U.S., potentially reducing development complexity and strengthening its critical minerals supply chain capabilities.

Simply Wall St Growth Rating: ★★★★★★

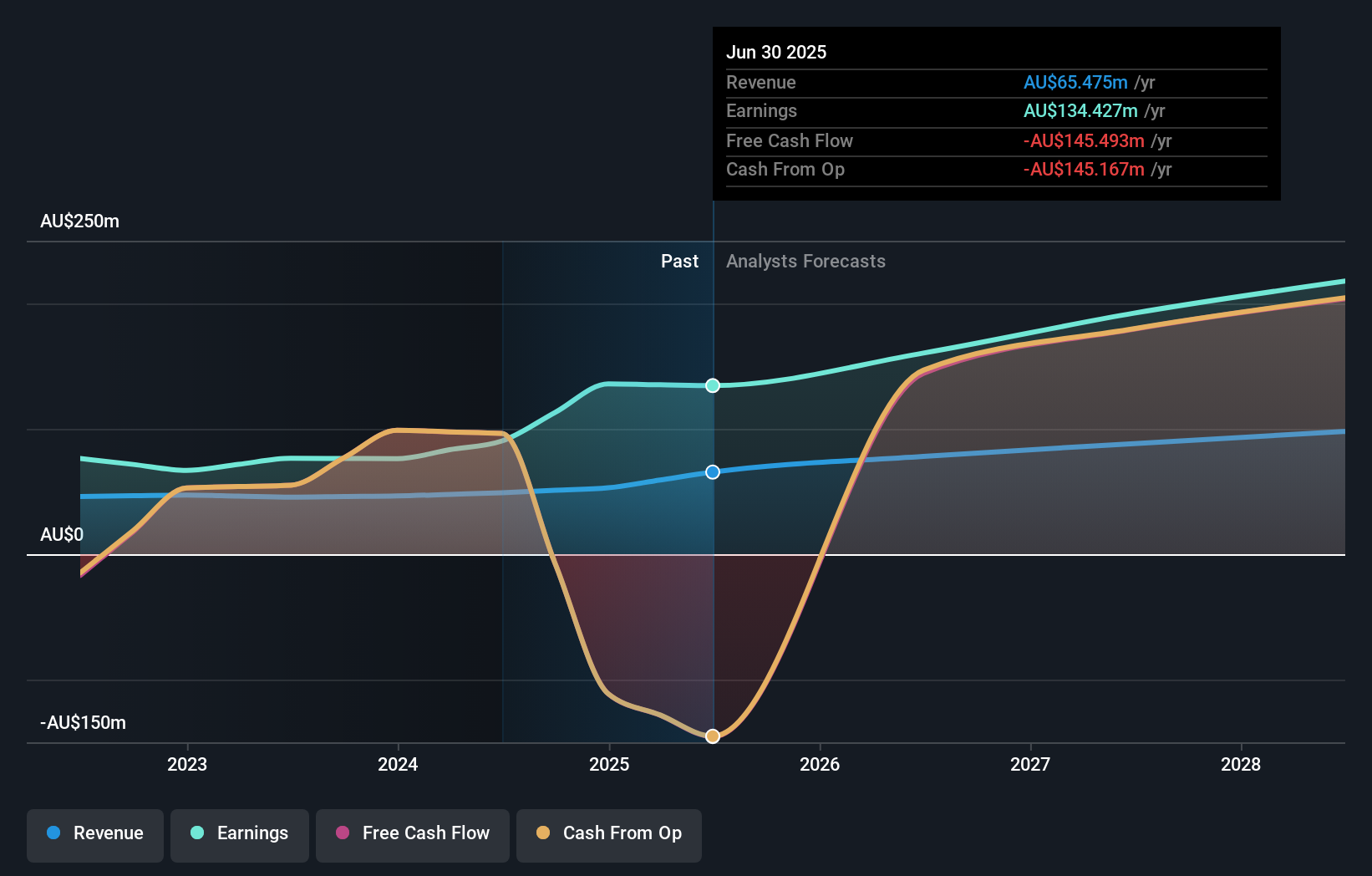

Overview: Pinnacle Investment Management Group Limited is an Australian investment management company with a market cap of A$4.04 billion.

Operations: The company’s revenue primarily comes from its Funds Management Operations, generating A$83.90 million.

Insider Ownership: 25%

Pinnacle Investment Management Group is positioned for strong growth, with revenue expected to increase at 30.4% annually, outpacing the Australian market. Insider activity shows more buying than selling recently, indicating confidence despite modest volumes. However, its profit margins have declined compared to last year. While trading below estimated fair value by 15.4%, the dividend yield of 3.26% isn’t well covered by earnings or cash flows, warranting caution for income-focused investors.

Turning Ideas Into Actions

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we’re here to simplify it.

Discover if HMC Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com