Software Sell-Off Was Overdone. Here Are the Best Growth Stocks to Buy Now.")

Artificial intelligence (AI) seemed a boon to tech stocks until investor sentiment shifted in 2026. AI was suddenly seen as a disruptor to many businesses, particularly those operating in the software-as-a-service (SaaS) sector. This led to the “Saaspocalypse,” where SaaS stocks experienced a widespread sell-off.

According to Goldman Sachs, the reaction went overboard. CEO David Solomon described the sell-off as “too broad,” and believes AI won’t create the sweeping destruction dreaded by Wall Street, stating, “There’ll be winners and losers, and, you know, plenty of companies will pivot and do just fine.”

The situation has created an opportunity to pick up shares in great businesses at a discount. Two software stocks well-positioned to rebound from this year’s sell-off are Figma (FIG +5.73%) and Atlassian (TEAM +29.10%).

Image source: Getty Images.

Why Figma stock is a buy

Generative AI’s ability to produce images and videos from simple text prompts fueled investor fears that Figma’s design software business was in trouble. The Saaspocalypse added fuel to the fire as the company’s share price plunged over 50% in 2026 through April 30. However, Figma’s success says otherwise about the AI threat.

In 2025, sales soared an astounding 41% year over year to $1.1 billion, driven by new customers. This is an encouraging sign, indicating Figma’s products are proving popular.

Today’s Change

(5.73%) $1.01

Current Price

$18.71

Key Data Points

Market Cap

$9.8B

Day’s Range

$18.26 – $19.27

52wk Range

$16.60 – $142.92

Volume

913K

Avg Vol

17M

Gross Margin

82.43%

Moreover, the company is increasingly integrating AI capabilities into its design tools. It acquired Weavy last year, which specializes in bringing multiple AI models together, allowing designers to easily employ the AI product best suited to a task. Figma’s AI tools are so powerful, my 10-year-old son used them to create a video game in a day.

The design giant expects sales to continue expanding in 2026, forecasting $1.4 billion for this year. While that sum represents excellent double-digit revenue growth over 2025’s $1.1 billion, it’s based on a per-user fee structure that doesn’t factor in AI income.

Figma added charges based on the consumption of AI credits. Customers must buy and expend credits to use AI. In Q1 of last year, no customers were consuming AI credits. Now, the company is experiencing a ramp up in AI usage, which should add to sales growth.

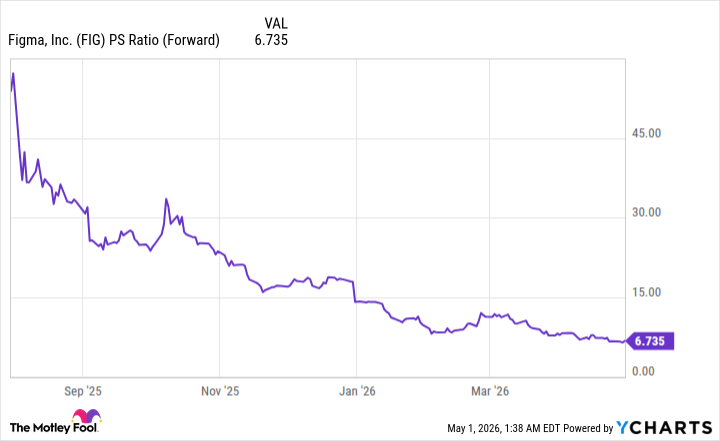

With its drop in share price this year, the company’s stock valuation looks attractive, as demonstrated by the change in its forward price-to-sales ratio.

Data by YCharts.

The chart shows Figma’s forward sales multiple experienced a substantial drop since its IPO last July. Now, shares are at a much better valuation. This, combined with the company’s strong sales growth and AI adoption, makes now a good time to buy Figma stock.

Reasons to invest in Atlassian

Atlassian provides software to help teams collaborate, plan, and manage work. Its stock tumbled nearly 60% this year through the end of April, as it was swept up in the Saaspocalypse. Since the company charges based on the number of app users, concerns cropped up that artificial intelligence would replace users, resulting in a fall in revenue.

This logic isn’t panning out, as Atlassian’s results for its fiscal third quarter 2026 (ended March 31) revealed. Customers weren’t cutting usage. Instead, they expanded the number of users accessing the company’s apps in Q3, proving the seat-based pricing model continues to deliver revenue growth.

Today’s Change

(29.10%) $19.96

Current Price

$88.55

Key Data Points

Market Cap

$24B

Day’s Range

$82.05 – $90.20

52wk Range

$56.01 – $232.36

Volume

1.3M

Avg Vol

7.7M

Gross Margin

84.50%

In addition, Atlassian’s AI solution, Rovo, is experiencing strong adoption. Customers can delegate routine tasks to Rovo, enabling greater productivity and efficiency. Like Figma, Rovo is priced based on AI credit consumption, producing a new revenue stream. In Q3, Atlassian reported AI credit usage was growing 20% month over month.

This success resulted in outstanding fiscal Q3 results. Revenue reached $1.8 billion, representing a strong 32% year-over-year increase. The company isn’t profitable, incurring a Q3 net loss of $98.4 million compared to the prior year’s loss of $70.8 million due to restructuring charges, but its balance sheet is strong.

Atlassian exited fiscal Q3 with total assets of $5.7 billion, including cash and equivalents of $1.1 billion. Total liabilities were $4.8 billion, but over $2 billion of that comprised deferred revenue of up-front customer payments that will be recognized as sales once services are delivered.

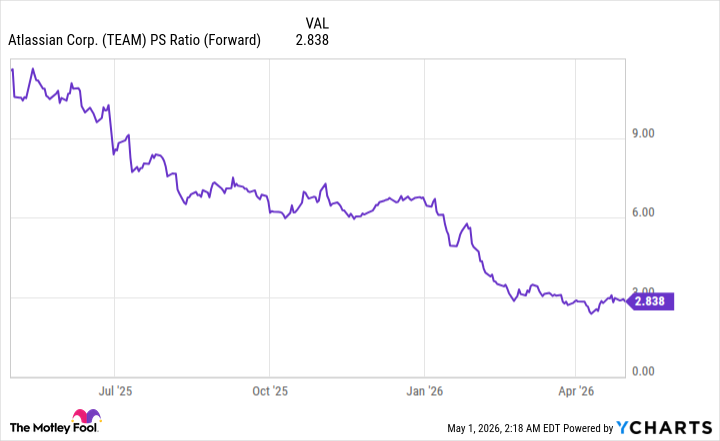

This year’s stock sell-off offers an opportunity to scoop up Atlassian shares at a substantial discount. Its forward price-to-sales ratio has plummeted over the past year.

Data by YCharts.

Atlassian’s enormous drop in its forward sales multiple suggests its stock is cheap. In fact, after releasing its fiscal Q3 results, Atlassian shares soared 20%, indicating investors are realizing the stock appears undervalued.

Even so, it’s still not too late to grab shares. After all, Atlassian achieved a 52-week high of $232.36 in 2025, so there remains the potential for considerable upside.