- Indonesia’s May 20 regulation requires palm oil, coal, and certain mineral exports to pass through state-owned Danantara Sumberdaya Indonesia from June 1, with full implementation targeted by December 31, 2026, giving the state greater control over export pricing and margins.

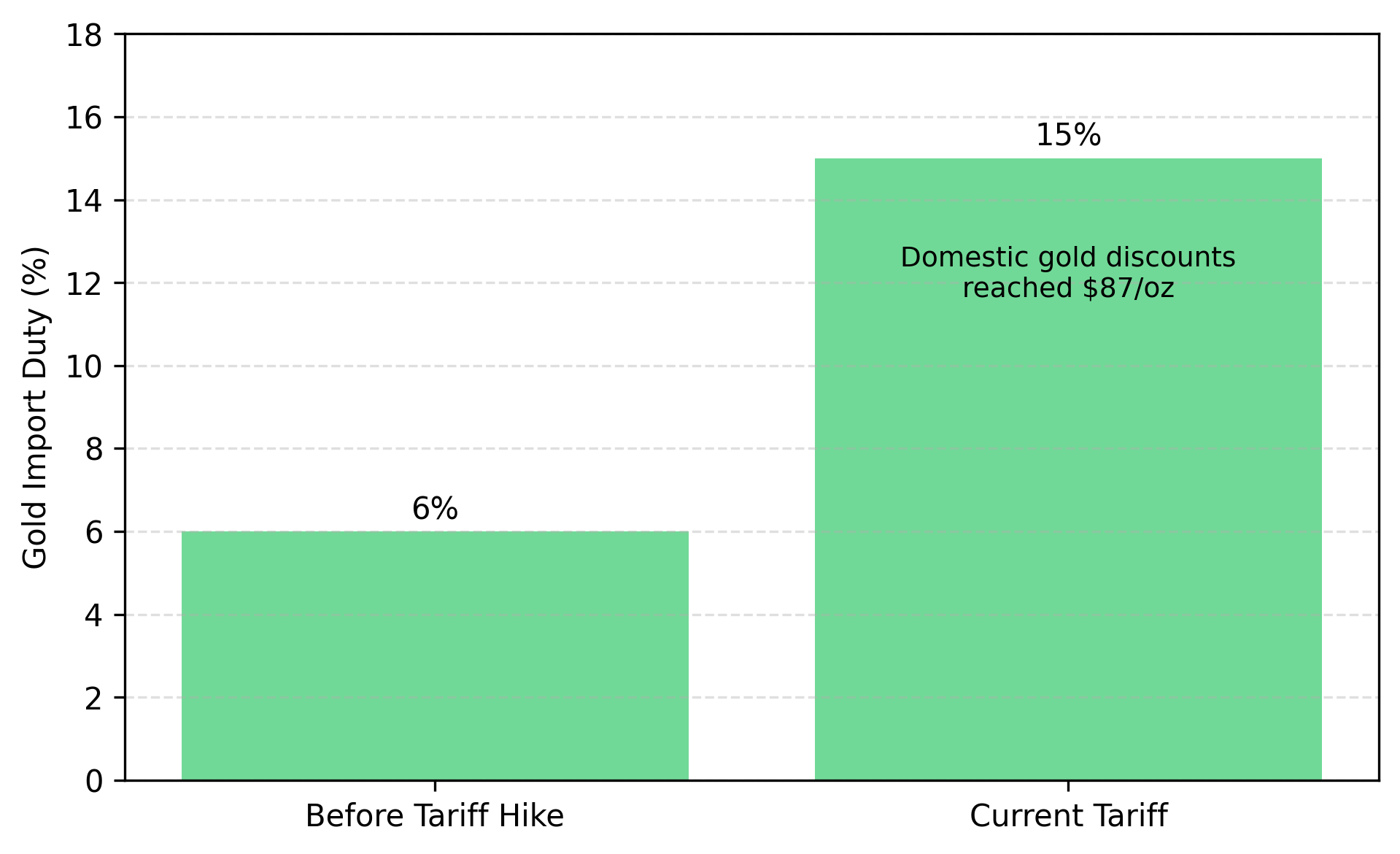

- India’s increase in gold and silver import duties from 6% to 15% widened domestic gold discounts to as much as $87 per ounce on June 5, 2026, reflecting weaker local demand.

- The Indonesian regulation allows the state export agency to determine selling prices and margins for covered commodities, reducing producers’ control over export revenue.

- Indian gold ETFs recorded their first monthly outflow in a year during May 2026 as higher import duties and elevated gold prices reduced investor demand.

- Indonesia granting broad export exemptions or India reducing its 15% gold import duty would weaken government intervention in commodity markets, improving earnings visibility for affected exporters and bullion dealers.

State Commodity Controls & Bullion Tariffs Hit Producer Margins

Indonesia imposed new export controls while India raised gold and silver import duties to 15%, increasing government influence over commodity markets. Indonesia’s May 20 regulation requires palm oil, coal, and certain mineral exports to pass through state-owned Danantara Sumberdaya Indonesia from June 1, with full implementation scheduled for December 31, 2026, giving the state authority over export pricing and margins.

In India, higher import duties pushed domestic gold discounts to as much as $87 per ounce on June 5 and contributed to the first monthly outflow from Indian gold ETFs in a year during May 2026.

Export Mandates & Import Duties Redirect Commodity Revenues

Indonesia’s regulation routes covered commodity exports through state-owned Danantara Sumberdaya Indonesia, with full state control scheduled from December 31, 2026. Producers can obtain exemptions only through existing agreements covering investment, divestment, or domestic processing, limiting eligibility for direct exports. In India, the increase in gold and silver import duties from 6% to 15% raised bullion import costs, prompting dealers to discount inventories as demand slowed and supporting government efforts to protect foreign exchange reserves, according to Reuters on June 5, 2026.

Implementation Delays & Exemptions Drive Producer Outcomes

Indonesia’s export overhaul will not be implemented immediately because exporters, buyers, and regulators must revise contracts, approvals, and shipment procedures before the December 31 deadline. Danantara Indonesia said on June 5 that producers could continue working with existing trading partners, reducing the risk of immediate supply-chain disruption, according to Reuters. Companies seeking exemptions still require regulatory approval, delaying visibility on which exporters can bypass state-controlled sales channels.

Export Margin Risk & Company-Level Resilience

Indonesian producers covered by the regulation face the greatest near-term risk to export margins. The decree allows the state export enterprise to determine selling prices and margins for covered commodities. If implemented as written, producers could retain a smaller share of export margins even if commodity prices remain unchanged.

Companies with domestic processing assets, qualifying government agreements, or diversified export channels are better positioned than producers that rely solely on direct commodity exports. For investors, the key variable is whether companies can preserve export margins under the new framework, not whether coal or palm oil prices rise.

Policy Triggers & Signals That Alter Earnings Risk

For Indonesian resource producers, earnings risk now depends more on implementation of export controls than on commodity price movements. Indonesian producers face margin pressure if the government proceeds with full implementation of export controls by December 31, 2026. Diversified global resource producers face less exposure to the regulation because earnings are not dependent on Indonesian export margins alone.

Margin pressure on Indonesian exporters would ease if Indonesia grants broad exemptions, while India’s bullion market would normalize if the government reduces its 15% gold and silver import duty. Either decision would give producers and distributors greater control over pricing, margins, and sales volumes.

Three specific signals to monitor: Indonesia’s detailed implementation regulations, announcements regarding exemption approvals, and any change to India’s 15% bullion import duty. These policy decisions provide clearer evidence of future earnings impacts than daily commodity-price volatility because they directly determine how profits are distributed across the supply chain.