Northisle Copper and Gold Inc is advancing one of Canada’s largest undeveloped copper-gold projects, with significant molybdenum and rhenium by-products, as demand for critical minerals shifts investor attention back to tier-one mining jurisdictions. Its flagship, the 100%-owned North Island project, is a district-scale copper-gold porphyry system near Port Hardy on northern Vancouver Island, British Columbia.

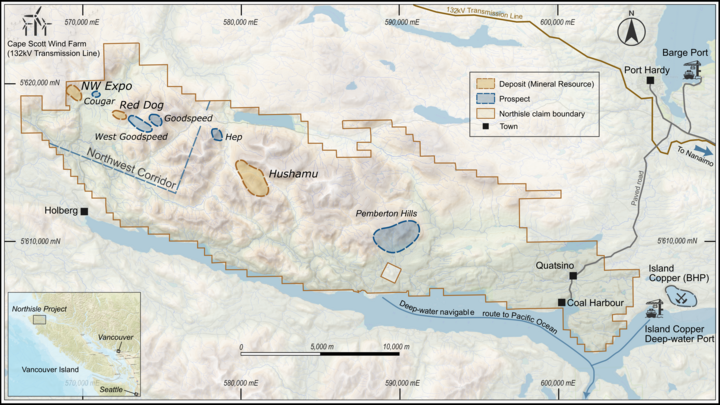

Originally transferred to Northisle in 2011 through a spin-out from Western Copper Corp, the project spans more than 34,000ha across 218 mineral claims and hosts the Hushamu, Northwest Expo and Red Dog deposits, together with six additional targets offering exploration upside.

The latest resource estimate increased global indicated resources by 60% to 906Mt, containing 3.1Blb of copper, 6.9Moz of gold, 149Mlb of molybdenum and 847,000lb of rhenium in indicated resources.

“British Columbia is the only place in Canada where these large porphyry copper systems occur,” Sam Lee, president and chief executive at Northisle Copper and Gold, told Mining IQ, underscoring the province’s strategic importance for future critical minerals supply.

A top priority project in BC

Northisle’s positioning as a critical minerals project was further reinforced in February 2026, when it was selected for British Columbia (BC)’s Critical Minerals Office. The designation supports early coordination with government agencies, First Nations and local communities, helping to streamline environmental assessment and permitting.

The initiative is expected to improve regulatory certainty by identifying key requirements and timelines earlier in the project development cycle.

“Being selected for the BC Critical Minerals Office sent a strong signal to the market that this is the top-priority project in British Columbia,” said Lee. “The selection helped underpin the company’s subsequent C$115 million financing.”

According to Lee, the project’s commodity mix sets it apart from many large copper development projects. Based on the 2025 preliminary economic assessment (PEA), revenues are expected to be approximately 45% copper, 45% gold and 10% molybdenum and rhenium. This means that more than half of North Island’s value is derived from commodities classified as critical minerals in Canada, the US and other jurisdictions.

At the same time, the substantial gold endowment strengthens the project’s economics by helping fund development of the more capital-intensive copper operation.

“Our tagline is realising copper value through gold,” Lee said, adding that the gold component could also lower the project’s cost of capital by attracting streaming and royalty financing from companies such as Wheaton Precious Metals – one of the world’s largest precious metals streaming companies and a significant shareholder of Northisle.

Northisle’s largest-ever drilling programme

On June 10, Northisle reported drilling results from the Red Dog deposit that confirmed the continuity of known mineralisation while identifying a new high-grade zone beyond the eastern limit of the PEA pit shell, highlighting further resource growth potential.

The results came from an 8,112m, 31-hole programme completed between 2025 and early 2026, primarily aimed at upgrading resources for the ongoing pre-feasibility study (PFS), with a standout intercept of 216m grading 0.67% Cu Eq., including 64.1m at 1.10% Cu Eq.

The campaign formed part of Northisle’s largest-ever drilling programme, totalling more than 20,000m across 58 holes, with a further 14,500m of drilling underway in 2026.

Beyond Red Dog, the company completed an updated PEA, raised C$154.5 million through two financings, advanced environmental permitting, expanded its technical team and continued regional exploration. As a result, Northisle extended mineralisation at Northwest Expo, confirmed a 1.2km mineralised trend at West Goodspeed and identified new copper-gold mineralisation at Cougar.

Northisle expects to deliver an integrated resource update and initial metallurgical results during 2026, ahead of completing the North Island project PFS in late 2026 or early 2027. First production is possible at the beginning of the next decade, with the PEA outlining average annual production of approximately 75Mlb of copper and 137,000oz of gold, for 157Mlb of copper equivalent production over a 29-year mine life.

First Nations partnerships

As the North Island project advances, Northisle continues to prioritise engagement with indigenous rightsholders and local communities. The company has formal agreements with all three First Nations whose traditional territories overlap the project, providing a framework for consultation, collaboration and exploration activities.

According to Lee, the success and timing of project development ultimately depend on the support of First Nations partners. “The timeline is almost entirely based on alignment with your First Nations partners,” he said, adding that community trust cannot be rushed.

“If the will isn’t there, you can’t change it overnight. It takes generations, and that’s not something you can force. Our role is to build relationships, not push against that, and help create enduring value across the North Island.”

Back to tier-one jurisdictions

According to Lee, mining investment has come full circle. After leading the industry in the 1950s-‘70s, Canada lost ground in the 1980s and 1990s as capital shifted to Latin America and Africa, attracted by faster permitting. But since around 2010, growing community opposition and political instability have eroded the appeal of many emerging mining jurisdictions, prompting investors and major miners to return to tier-one countries such as Canada, the US and Australia, where stronger a rule of law and social licence provide greater long-term certainty.

“The challenge today isn’t finding mines: they’re everywhere. The challenge is earning the social licence that allows communities to support development. Canada spent decades building that framework and is now 20-30 years ahead of many tier-two jurisdictions. While the permitting system is far from perfect, we’re seeing growing political will at both the federal and provincial levels to restore Canada’s position as a resource superpower, much like the nation-building era of the 1960s and 1970s,” explained Lee.

“That’s why I believe tier-one jurisdictions such as Canada, the US and Australia are once again the most attractive places for long-term mining investment.”