The trend is changing how lenders acquire customers, with banks now competing for a larger share of existing borrowers’ spending rather than relying primarily on new-to-credit consumers.

The shift is expected to continue as younger consumers adopt multiple credit products earlier in their financial journey. While credit cards remain an important lending and payment product, lenders will increasingly need to differentiate through customer engagement, rewards and cross-selling strategies.

According to TransUnion CIBIL’s report, credit cards accounted for 56% of consumption lending in 2016, but their share has declined to 38% in 2026. At the same time, borrowers are holding more diversified credit portfolios, with many consumers using multiple credit cards alongside personal loans, consumer durable loans and other borrowing products.

Jain attributed the shift to the growing availability of alternative lending products and digital payment options.

“The consumer has multiple choices… through consumer durable loans, personal loans or BNPL… and if a consumer is using credit cards as a payment tool, the consumer today has multiple choices, largely in the form of UPI.”

He noted that India’s payments infrastructure has also changed significantly, with around 600 million UPI acceptance points compared with only 11 million credit card POS terminals, making UPI more widely accessible.

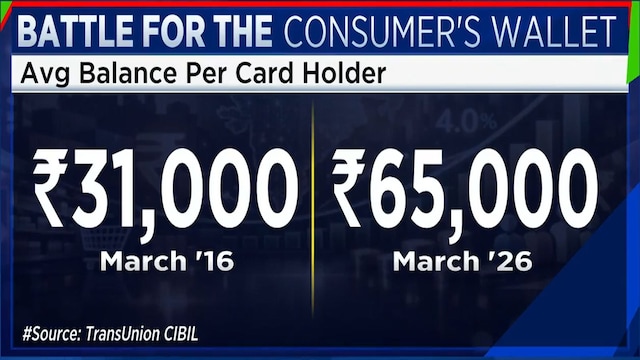

The report also shows that the number of credit card holders has remained largely unchanged at around 5.2 crore, suggesting that existing users are increasingly adding second and third cards instead of the market expanding through new users.

Jain said nearly 70% of new credit cards are now issued to customers who already hold at least one credit card.

Despite changing borrowing patterns, he said there are no signs of stress in the retail credit market.

“There is no stress right now… the credit card delinquency from last year has come down. It’s just 1.7%.”

He added that only about 25% of India’s credit-active population currently holds a credit card, leaving significant room for issuers to expand their customer base. Jain also said the opportunity is spread across both urban and semi-urban markets, giving both established and new lenders scope to grow.

As borrowers increasingly combine multiple lending products, the focus for banks is shifting from acquiring first-time borrowers to becoming the preferred financial partner throughout a customer’s credit journey.

For the full interview, watch the accompanying video

Catch all the latest updates from the stock market here