Why this matters: A decade of rising fixed rate mortgage (FRM) rates with no present sign of meaningful decline has reduced the amount of mortgage funding attainable by homebuyers. For tenants intent on homeownership, it became paramount to consider ARM funding to reach the ownership they expect.

As their sole gatekeepers, buyer brokers and their agents need a grasp on understanding ARMs to advise their buyers on the risky landscape of ARM financing. The advice is to caution buyers to instead obtain FRM mortgage funding and sidestep the foreclosure risks exclusive to ARMs.

The ill-informed popularity of adjustable-rate mortgages

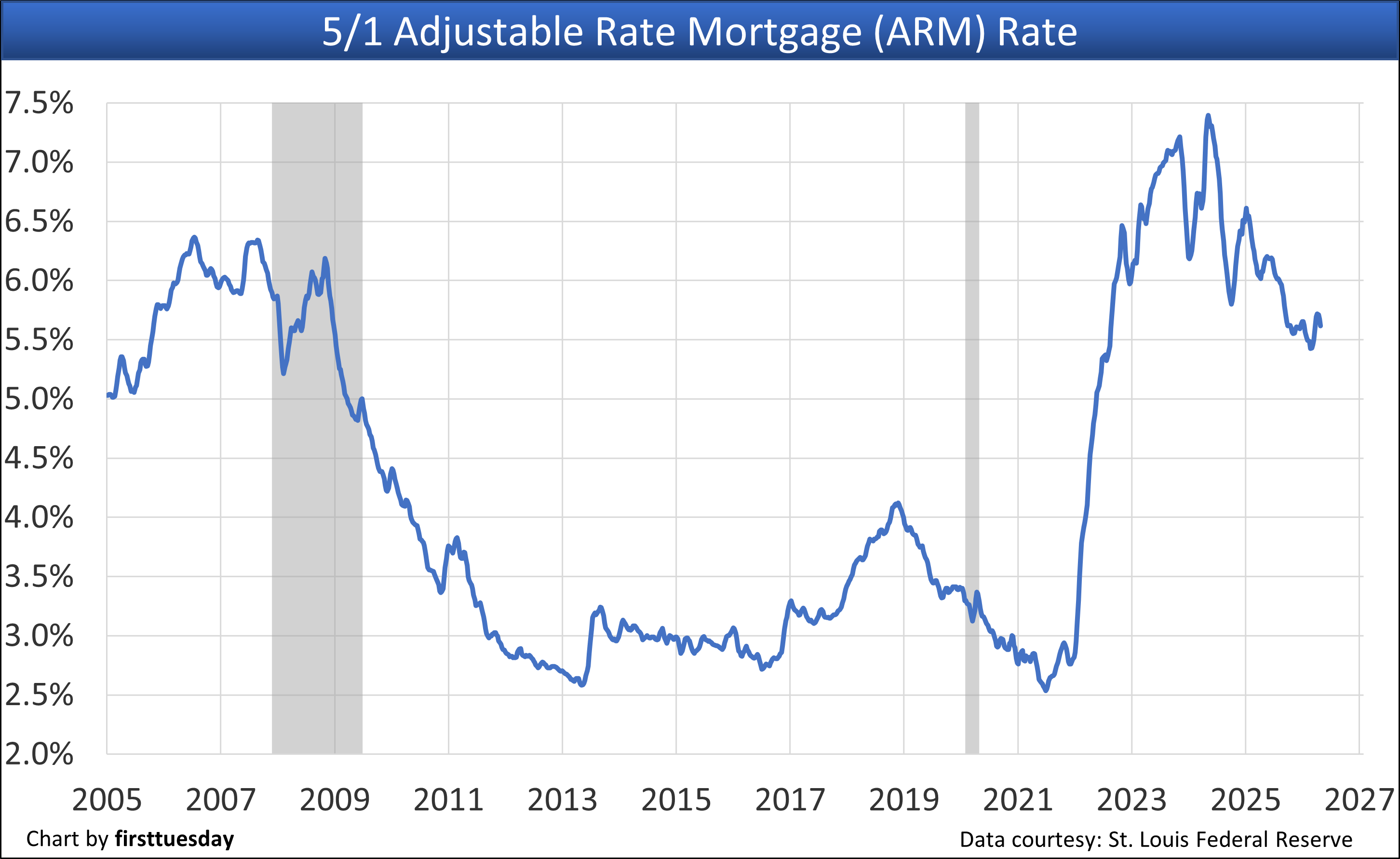

The average rate for an adjustable-rate mortgage (ARM) on a 5/1 ARM averaged 5.68% in April 2026. This is down from a year earlier when the ARM rate was 6.07%.

As of April 2026, the average 30-year amortized ARM rate is level with the average 15-year FRM rate, but much lower than the 30-year FRM rate by 66 percentage points, the rate spread between ARMs and FRMs.

This rate spread difference allows the buyer to borrow significantly more purchase-assist mortgage funds when taking out an ARM, rather than an FRM. Thus, the increase appeals to tenants borrowing using these riskier predatory mortgage products.

Long-term homebuyers prefer the security of an FRM rate. However, tenants as first-time homebuyers are confronted with MLOs and buyer agents who are incentivized by percentage-based fees to encourage ARM use. The property sold is priced too high for standard 30-year FRM financing, but it is reachable when the buyer takes out an ARM.

As always, remember that MLOs and buyer agents expecting to earn a fee for assisting a buyer are duty bound to act in the best interest of their buyer client, not their own self-interest.

Updated May 18, 2026.

Chart update 5/18/26

| Apr 2026 | Mar 2026 | Apr 2025 | |

| Average 5/1 ARM rate | 5.68% | 5.62% | 6.07% |

The chart above shows the average interest rate for the first five years after origination on a 5/1 ARM, the most popular type of ARM for homebuyers. After the initial five-year period, the ARM rate is adjusted annually based on an index figure.

ARM rates yesterday, today, tomorrow, after origination

The adjustable rate mortgage (ARM) rate was legalized in 1980 through passage of the Depository Institutions Deregulation and Monetary Control Act of 1980. It overrode California’s decade old variable interest rate (VIR) mortgages which prohibited damaging rate and payment adjustments.

The Act’s title includes the word “deregulation” as a clue of the pending damage to the borrowing consumer. Further deregulation came each decade until this was brought to an end by highly detailed re-regulation in 2010. Consumers received protection with the nation’s first consumer protection laws, ever, brought on by the Great Recession of 2008.

Unlike a fixed rate mortgage (FRM), which guarantees a set rate and a constant monthly payment amount over the life of the mortgage, ARMs shift economic analysis and risk of loss from the mortgage lender to the borrower. This risk shifting allows mortgage rates to “float” based on future money market conditions. Any increase in future money costs trigger an increase in the rate charged on a previously funded ARM.

The cost of lending money based on the Fed rate at a 10-year or 30-year fixed bond market rate, a huge risk for lenders, is with an ARM that is no longer theirs to consider. However, the home-buying public has no general understanding of secondary financing arrangements, much less multi-faceted adjustable-rate arithmetic.

Worse, the median age in the California population is about 40 years. Thus, the typical first-time homebuyer has had little to no opportunity or education to learn about ARMs. Without practical experience or wisdom on real estate financing they cannot appreciate the risks in an ARM even when they know ARMs exist.

For example, the ARM rate charged and amortized payments are tied to one of several specified indexes that varies based on market factors, none of which consumers are taught to understand.

For starters, the initial interest rate before adjustments is called the teaser rate. It has no relationship to current mortgage rates, other than it is lower. On adjustments in coming years, the update of the ARM note rate equals the change in figures of the index specified in the ARM note, plus a fixed profit margin for the lender. What possibly could go wrong?

Common indices used to periodically adjust the ARM rate include the:

However, the interest rate not listed above with the primary influence over movement in the listed indexes used to adjust ARM rates is the Federal Funds rate. Thus, it is the setting of the Fed rate that, well, sets the change in the ARM rate, a daily occurrence. The Fed rate is the target short-term borrowing rate the Federal Reserve (the Fed) sets for banks for purposes fully unrelated to mortgage lending or real estate operations.

The Fed rate is not a rate directly related to setting long-term treasury note and bond rates or FRM interest rates. However, the Fed rate hugely affects the indexes making further adjustments to ARMs taken out by homebuyers. Not what prudent ownership of real estate is about.

ARM use: a danger for the housing market

The previous peak in average ARM rates during 2006 put ARM rates at just over 6%. At that time, three out of every four mortgages originated in California were ARMs, a harbinger ignored until 2010’s re-regulation of ARMs. This proved disastrous for all owners of homes in California. The forced sales, achieved one way or another on 1.1 million homes in California for inability to pay, drove home pricing down nearly 50% from 2007’s peak over the following five-year period.

ARMs are far riskier mortgage products than FRMs. ARMs, unlike FRMs, basically function as a short-term loan with a rollover feature when not prepaid during the initial period of the teaser rate. Here too, buyers are coached by both MLOs and buyer agents — again, it is about fees for otherwise unnecessary services for a homeowner — to figure out refinancing to avoid any adjustment in payments.

When ARM rates do reset, the higher payment often results in a foreseeable but unbudgeted payment shock, catching many homeowners without the ability to pay.

To refinance into an FRM before ARM payments reset requires the economy to cooperate by having proper conditions for refinancing. However, economy cycles do not function based on homeowner plans. As always in a business cycle, employment rates drop as jobholders are released when another job is not available in the location of the home.

This jobs market condition, always volatile, makes mortgage payments impossible for unemployed homeowners during a recession. This situation was the primary cause for the depth of the 2008-2011 foreclosure crisis as prices were forced downward thus eliminating the equity of small down payments quickly.

The epic catastrophe of the Great Recession due to ARM originations enlightened homebuyers to steer clear of the mortgage ARM products in the years following the recession. Stricter underwriting standards introduced in 2010 required MLOs processing homebuyer mortgage applications to qualify the homebuyer’s capacity to pay based on payment resetting at the maximum index ceilings rather than the teaser rate.

This ability to pay for an MLO to qualify a buyer helped keep ARM use in check. Still, ARM use inched up when the ARM rate was at its bottom in 2013. By 2014, roughly one out of every six mortgage originations was an ARM, according to Freddie Mac. Historically, this ratio is considered about average for a healthy mortgage market.

Today, ARM use continues its unhealthy rise. New data from Cotality shows ARMs make up almost 21% of mortgages nationally. In California, it’s worse: ARM share jumped up to more than 31% of mortgages in 2025. As this trend providing greater reach to homebuyers intensifies, we now wait for the coming recession. The rising higher use of ARMs bodes poorly for a low foreclosure rate to take place when we enter the next recession — an inevitability.

The future of the ARM

What will the ARM chart above look like in the coming months and years?

Homebuyers were granted some new protections after the fallout of ARM overuse in 2008. To decrease the damage brought on by ARMs, some lender provisions deemed predatory with a reputation for unacceptable consumer risk were barred in 2010 federal legislation.

However, it is the convenience of a lower interest rate provided by an ARM when the Fed Rate is lower than the 30-year FRM rate that grabs people hook, line and sinker. The greater borrowing capacity provided by an ARM when the Fed Rate is too low sways those buyers in pricy real estate markets with low ARM rates to take that bait. An irony is they achieve ownership over the significantly lower monthly cost of renting the same or similar property.

That said, the rise in ARMs will remain as long as FRM rates remain significantly higher, a Fed monetary decision going forward. Today, with economic and military wars, it appears FRM rates will remain high and will naturally move higher in the longer term. It is the consumer inflation rapidly building up that (when properly managed) will cause ARM rates to increase and reduce the use of ARMs.

Related article: