As the Australian market anticipates GDP data with a cautious eye on potential economic slowdowns, investor attention remains focused on growth opportunities within the ASX. In this environment, companies with high insider ownership often signal strong confidence from those closest to the business, making them compelling options for investors seeking alignment of interests and potential resilience in uncertain times.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Torque Metals (ASX:TOR) | 18.6% | 94.2% |

| Starpharma Holdings (ASX:SPL) | 15.6% | 91.8% |

| SKS Technologies Group (ASX:SKS) | 28.2% | 39.5% |

| Pinnacle Investment Management Group (ASX:PNI) | 25.1% | 21.1% |

| Magnetic Resources (ASX:MAU) | 33.6% | 124.2% |

| Forrestania Resources (ASX:FRS) | 37.9% | 102.3% |

| Echo IQ (ASX:EIQ) | 19.7% | 108.8% |

| Austral Resources Australia (ASX:AR1) | 19.4% | 38.7% |

| Adveritas (ASX:AV1) | 17.9% | 108.4% |

| Advanced Energy Minerals (ASX:AEM) | 35.1% | 48.4% |

Let’s uncover some gems from our specialized screener.

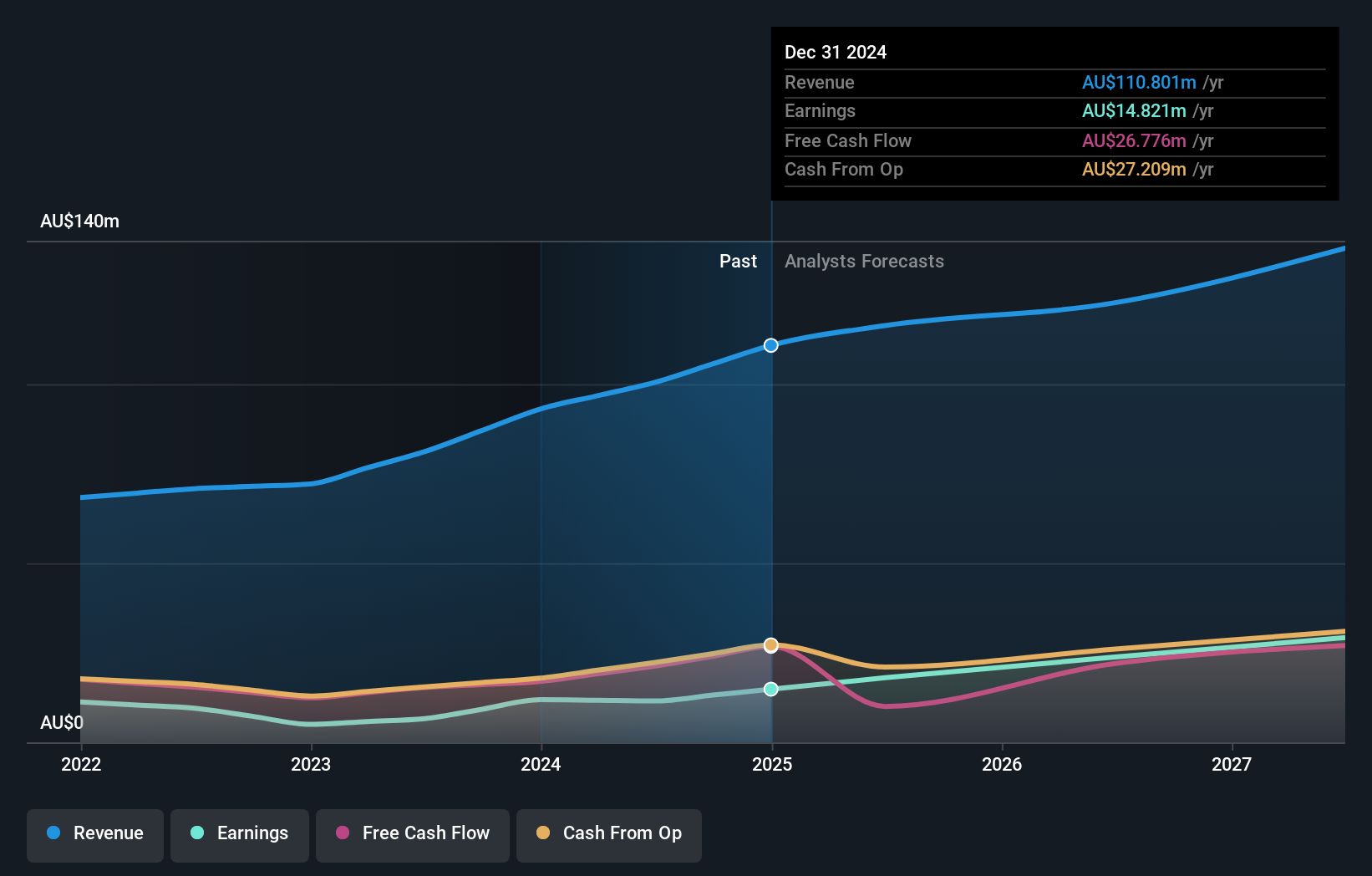

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Australian Ethical Investment Ltd is a publicly owned investment manager with a market capitalization of A$456.46 million.

Operations: The company’s revenue is primarily derived from its funds management segment, which generated A$126.41 million.

Insider Ownership: 19.5%

Earnings Growth Forecast: 14.4% p.a.

Australian Ethical Investment is experiencing moderate growth, with earnings projected to increase by 14.4% annually, outpacing the broader Australian market’s 12.1%. Revenue is expected to grow at 8.6% per year, surpassing the market average of 6.3%. The company’s Return on Equity is forecasted to be very high at 53% in three years. Recent board changes include Karen Orvad’s appointment as an independent Non-Executive Director, reflecting ongoing governance enhancements amidst a stable insider ownership structure.

Simply Wall St Growth Rating: ★★★★☆☆

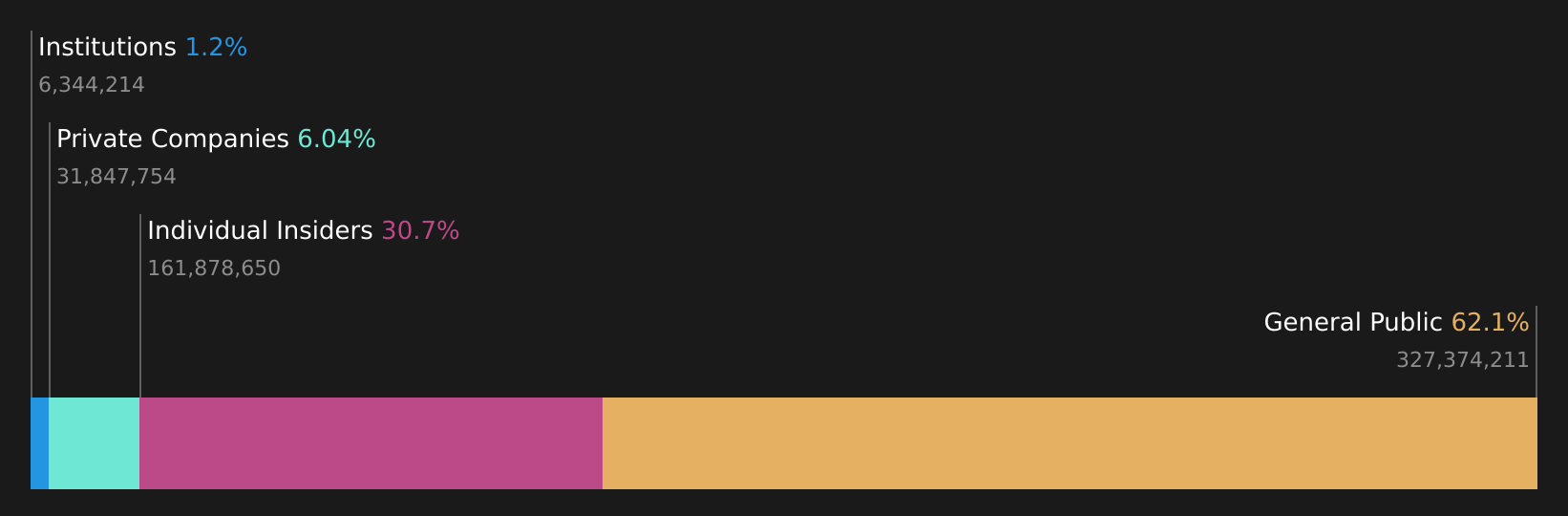

Overview: MA Financial Group Limited, along with its subsidiaries, offers a range of financial services in Australia and has a market capitalization of approximately A$1.09 billion.

Operations: MA Financial Group Limited generates revenue through its Asset Management segment (A$217.55 million), Lending & Technology (A$96.79 million), and Corporate Advisory and Equities (CA&E) services (A$68.70 million).

Insider Ownership: 36.3%

Earnings Growth Forecast: 27.4% p.a.

MA Financial Group faces a mixed outlook with earnings expected to grow significantly at 27.41% annually, outpacing the Australian market’s 12.1%. However, revenue is forecast to decline by 27.3% per year over the next three years, and profit margins have decreased from last year’s 3.8% to 0.7%. Insider activity shows more shares bought than sold in recent months, indicating confidence despite financial challenges and a dividend that is not well covered by earnings.

Simply Wall St Growth Rating: ★★★★☆☆

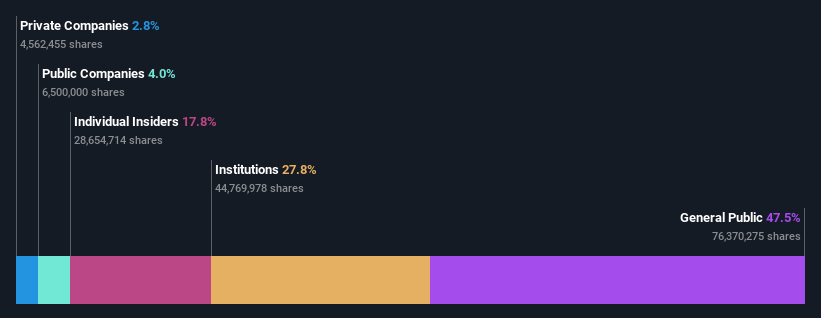

Overview: Vysarn Limited offers water services across sectors such as resources, urban development, government and utilities in Australia, with a market cap of A$522.17 million.

Operations: Vysarn Limited generates revenue through its Advisory segment with A$30.46 million and Industrial segment with A$72.44 million, serving sectors like resources, urban development, government, and utilities in Australia.

Insider Ownership: 30.7%

Earnings Growth Forecast: 21.3% p.a.

Vysarn exhibits strong growth potential with earnings expected to rise significantly at 21.3% annually, surpassing the Australian market’s average of 12.1%. Although revenue growth is forecasted at a slower rate of 15.4%, it still exceeds the broader market’s 6.3%. Despite no recent insider trading activity, substantial insider ownership suggests confidence in its trajectory. However, a forecasted Return on Equity of 13.8% in three years indicates room for improvement in profitability metrics.

Next Steps

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders.

It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities.

All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com