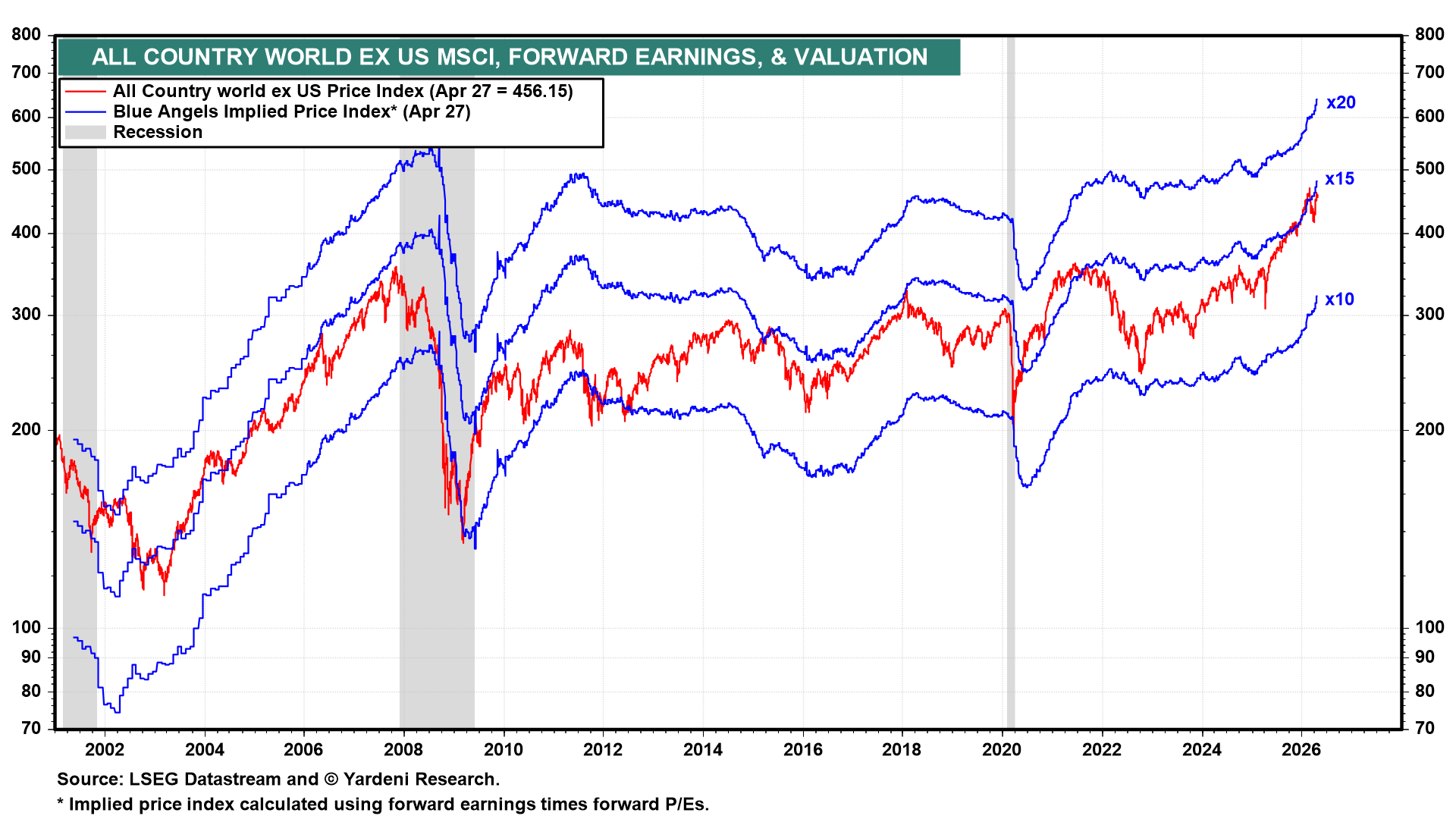

Stock markets around the world sold off sharply after the US and Israel attacked Iran on February 28. Despite the blockade of the Strait of Hormuz since the war began, global stock prices have rebounded since the end of March. That is surprising, given that many countries’ economies are vulnerable to stagflation and even recessions if oil prices remain elevated and oil shortages occur. Even more surprising is that industry analysts have raised their forward earnings expectations to record highs for the All Country World (ACW) ex-US MSCI in recent weeks, and at a faster pace (chart). They are either all delusional or correctly betting on the resilience of the global economy. That resilience might be partially attributable to technological innovations that are boosting profit margins worldwide.

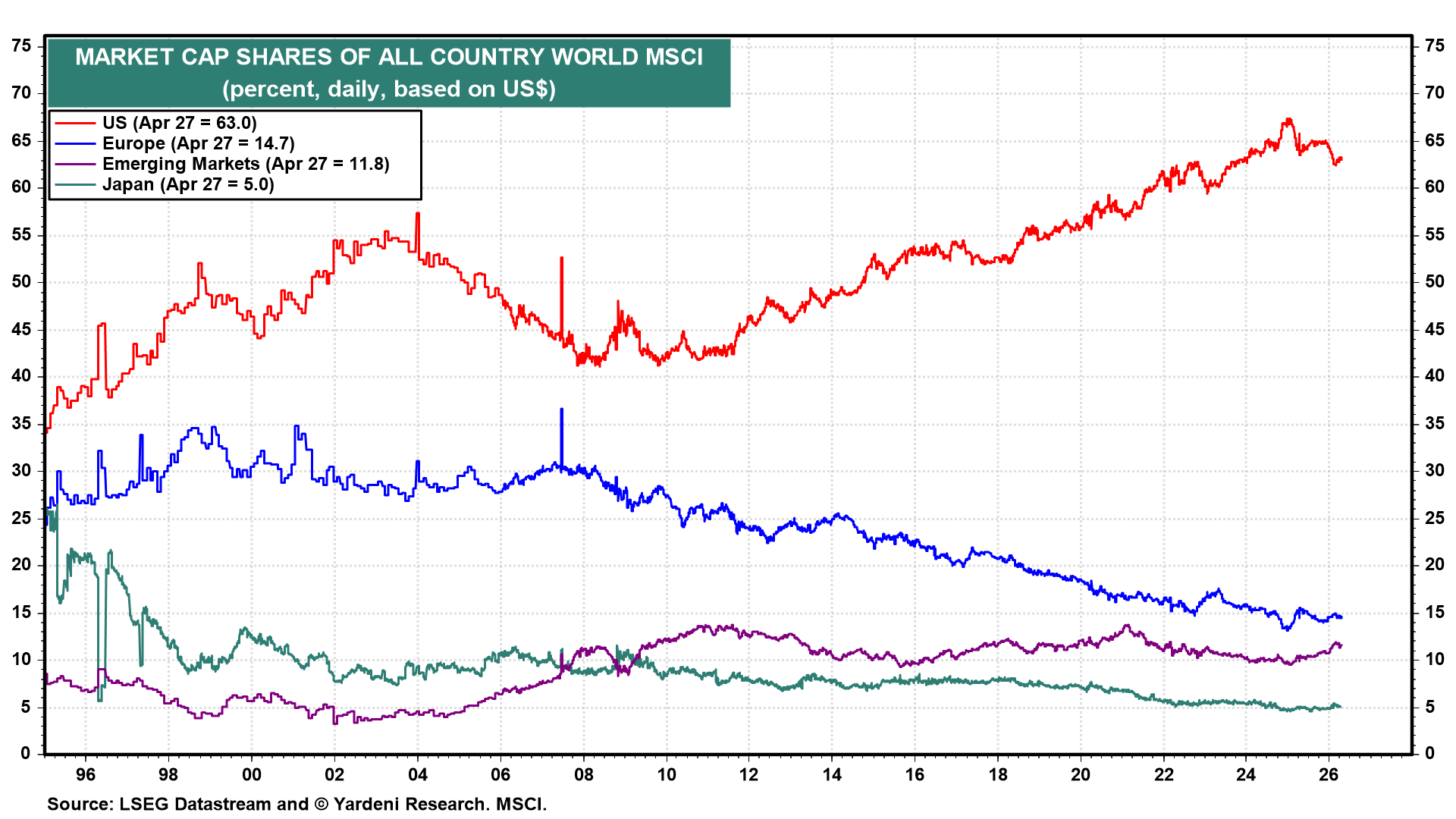

In any event, we continue to favor a Go Global investment posture. In early December last year, we recommended underweighting the US and overweighting the rest of the world in global stock portfolios. We did so because the US accounted for 65% of the ACW MSCI’s market capitalization (chart). We had favored a Stay Home posture since 2010. We reckoned it was time to rebalance overseas, especially since stocks are cheaper overseas.

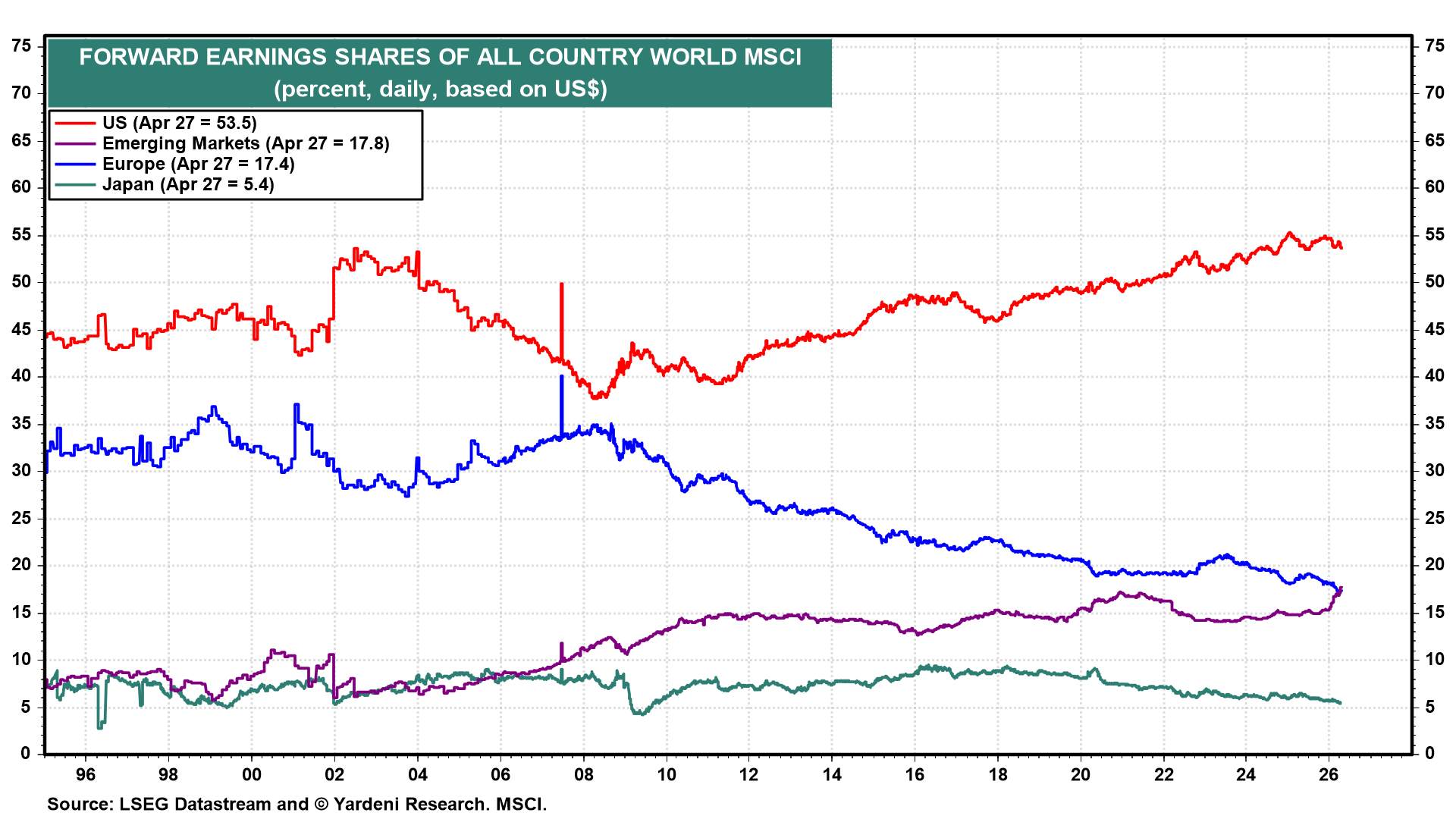

It’s true that the US has accounted for about 54% of the ACW MSCI’s forward earnings over the past couple of years (chart). But now, the Emerging Markets MSCI is starting to show a rising forward earnings share.

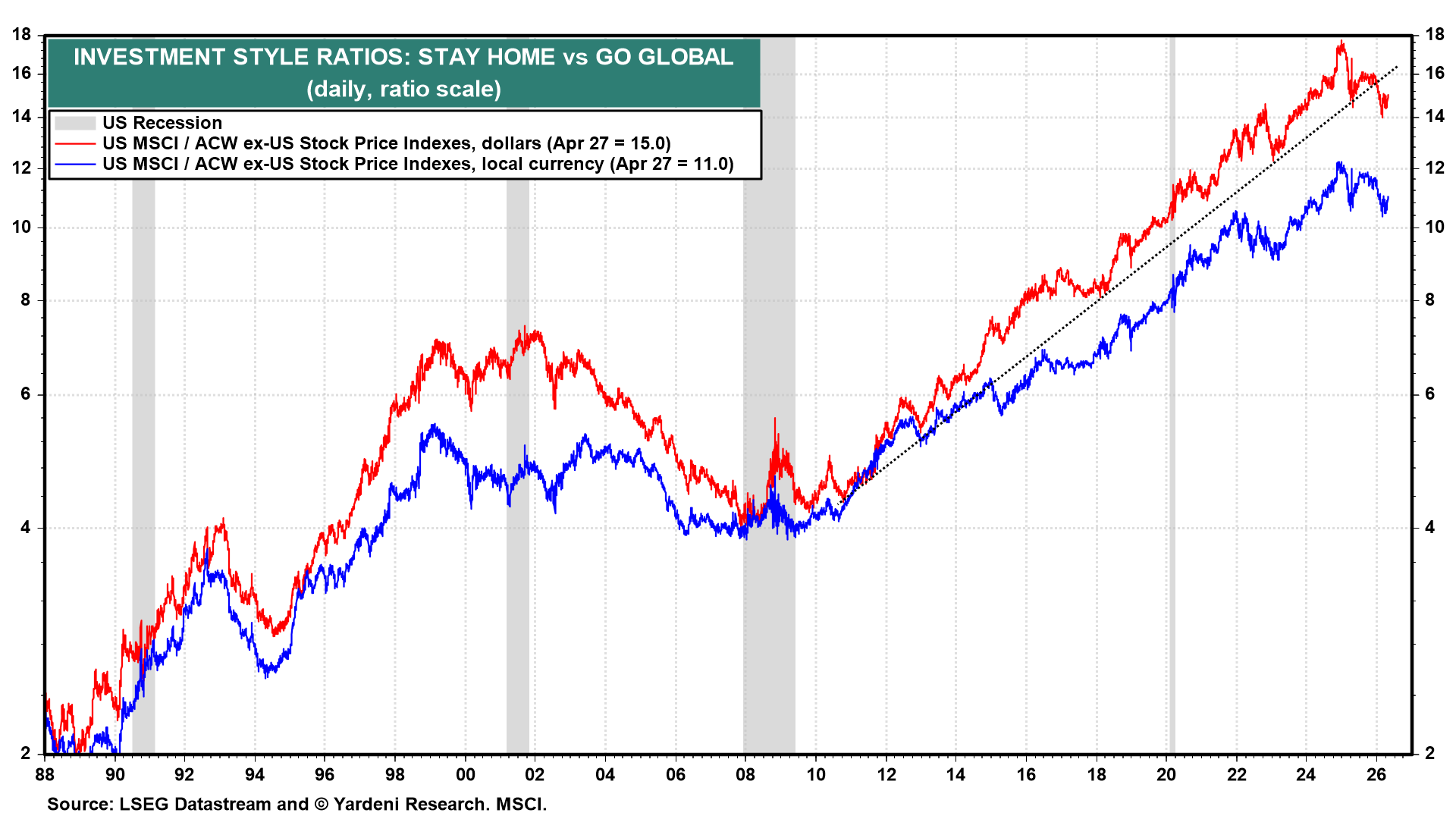

On a technical basis, the ratio of the US MSCI to the All Country World ex-US broke below its long-term uptrend line, which began in 2010, late last year (chart).

The comparable ratio comparing the US to other developed economies has been moving sideways since early 2025 (chart).