The International Association of Pension Fund Supervisors (AIOS) recently published the study: Investment Portfolio Composition in AIOS Country Pension Systems (June 2026). Beyond comparing the pension systems of eight countries, the document shows how alternative investments have transitioned from being a marginal allocation to becoming a strategic component of the region’s institutional portfolios.

The growth of assets under management illustrates this evolution. Between 2020 and June 2025, pension funds in AIOS member countries increased their assets from approximately US$631 billion to US$840 billion, equivalent to a compound annual growth rate (CAGR) of nearly 6.6%.

However, market size is only part of the story. The study identifies distinct allocation patterns, among which three particularly illustrative cases stand out.

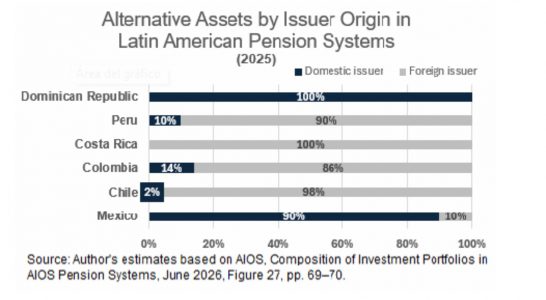

Chile, Colombia, and Peru have opted for a high internationalization of their portfolios. In these markets, nearly half of the assets are invested in foreign issuers, seeking greater geographic and currency diversification.

Mexico, on the contrary, presents a different model. Although it maintains a higher proportion of investments in domestic issuers, it has developed one of the most sophisticated regulatory frameworks to channel resources into alternative assets through structured vehicles such as CKDs and CERPIs.

The difference is relevant. Analyzing solely the issuer’s domicile can lead to underestimating the international exposure of Mexican Afores.

Mexico Retains the Largest Regulatory Leeway

One of the study’s most interesting findings is that Mexico retains the largest regulatory leeway to expand its exposure to alternative assets.

The youngest SIEFOREs can allocate up to 30% of their assets to structured instruments, a higher limit than that observed in most of the analyzed countries. In comparison, Chile will gradually raise the limit for alternative asset investments in Fund A, from 17% currently to 19% in August 2026, and a maximum of 20% in August 2027.

Although current allocations remain below those limits, the Mexican regulatory framework still offers ample room for alternative asset exposure to continue increasing in the coming years.

Alternative Assets Are Already Strategic

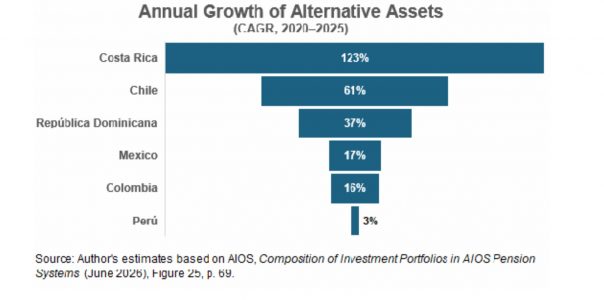

The study also shows that the growth of alternative assets is not a passing fad.

During the 2020-2025 period, practically all countries expanded their exposure to this asset class. Mexico recorded a compound annual growth rate of nearly 17%, while Chile reached approximately 61%, and Costa Rica recorded the highest growth rate (123%), albeit starting from a very small base.

In absolute terms, Mexico maintains the largest regional exposure, with approximately US$22 billion invested in private equity, US$16.5 billion in real estate, and nearly US$4.7 billion in infrastructure.

Implications for International Managers

For global private equity, infrastructure, and private credit managers, the message is clear.

The opportunity in Latin America does not rely solely on the growth of assets under management, but on the sophistication process that institutional investors are undergoing. Allocations to private markets continue to expand, regulatory frameworks continue to evolve, and portfolios are seeking greater diversification to face increasingly long investment horizons. In this context, Mexico continues to hold a prominent position within the region.

It combines the largest institutional market in Latin America with a regulatory framework that allows for significant participation of alternative assets. The challenge for international managers will no longer be demonstrating why private markets should be part of portfolios, but rather differentiating themselves in an environment where competition for institutional capital will only intensify.

Column by Arturo Hanono