Sridharan also said Piramal Finance will continue to expand its newly launched gold loan business in a measured manner, targeting 200 branches by the end of the year without chasing aggressive loan growth. He added that asset quality remains stable, the legacy book continues to shrink, and the company’s planned ₹4,000 crore capital raise is meant purely to support organic growth.

Piramal Finance reported first quarter, with net interest income rising 43% year-on-year to ₹1,442 crore from ₹1,010 crore. Pre-provision operating profit jumped 89% to ₹804 crore, while net profit increased 67% to ₹461 crore from ₹276 crore in the year-ago period.

Mumbai-based Piramal Finance was listed on the NSE and BSE on November 7, 2025. The stock has gained nearly 17% over the past six months, taking the company’s market capitalisation to around ₹48,577 crore.

This is an edited transcript of the interview.Q: Piramal Finance’s AUM is now comfortably above the threshold for upper-layer NBFCs, and you’re targeting another 25% growth this year. What’s driving this outlook? Also, apart from mortgages and unsecured loans, what’s happening on the gold loan front? You’re looking to increase branches to 200 even as gold prices have corrected. How is that book performing?A: There are two or three questions in what you asked. On the overall demand environment, yes, we are seeing strong demand, and that has resulted in a solid 25% growth at the consolidated level for our business and a 32% growth in our growth businesses, which now constitute 98% of our AUM.

We have had a very strong first quarter in terms of growth, and it has been a little surprising. It is not something I would have expected going into the quarter because of concerns around the West Asia situation and emerging threats such as El Nino, which were creating uncertainty. However, as the quarter progressed, things turned out to be quite strong. Demand has remained positive across most categories, resulting in broad-based growth.

Coming to gold loans, this is a business we entered three months ago, and June was our first full month of operations. We have opened 67 branches during the first quarter and intend to end the year with around 200 branches.

You are right that gold prices have risen sharply over the past two years before correcting from their peak. Prices have moderated meaningfully from peak levels. Even so, gold loans have become the second-largest retail lending category after home loans. It is now too large a segment for any major lender to ignore.

Our approach, however, will remain conservative and measured. While we are expanding the branch network, business volumes will not be our primary focus at this stage. We are not looking to aggressively push AUM growth in this segment just yet.

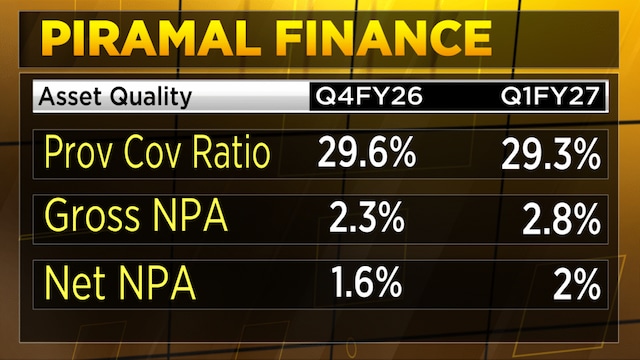

Q: Let’s talk about asset quality. While overall quality remains healthy, there has been some incremental increase in home loans and loans against property. The West Asia impact appears to have been better than expected. What is your outlook for the rest of the year?A: The first quarter surprised positively. Typically, first-quarter asset quality numbers tend to be weaker, but this year we did not see that seasonality. The numbers were actually quite strong across the board.

Q: Let’s talk about asset quality. While overall quality remains healthy, there has been some incremental increase in home loans and loans against property. The West Asia impact appears to have been better than expected. What is your outlook for the rest of the year?A: The first quarter surprised positively. Typically, first-quarter asset quality numbers tend to be weaker, but this year we did not see that seasonality. The numbers were actually quite strong across the board.

I am not seeing any significant pockets of concern. With El Nino, we will need to monitor customers whose incomes depend more on agriculture. The rains during the first few days of July have eased some of those concerns, but it is still something to watch.

Beyond that, there are no major areas of anxiety. Even the minor movement you mentioned in home loans and loans against property is largely seasonal and not something that worries us at this stage.

We share data across every product every quarter, so naturally some segments move up or down. Overall, however, the operating environment is much more benign than what we had expected earlier this year.

Q: What about the legacy book? How long will it take for a substantial resolution, and do you expect any further provisions?A: For the first time, the legacy book has now fallen below 2% of our overall AUM, and it will continue to decline as a percentage of the portfolio.

My expectation is that by the end of the year it will be around 1-1.5% of AUM, after which it will become too small to report as a separate segment.

In terms of incremental profit and loss (P&L) impact, I do not expect any net additional impact from this portfolio. That has been the case for the past four or five quarters. If you look at our consolidated profits and the profits from the growth book, they have been almost identical, which effectively means the legacy portfolio has had no meaningful impact on earnings.

That trend should continue, and if anything, it should turn positive as we move into next year.

Watch the full conversation here

Q: One final question. You’re raising ₹4,000 crore of capital, saying it’s to strengthen regulatory capital buffers. Are any acquisitions or inorganic opportunities on the table?A: No. This capital raise is entirely for organic growth and to maintain the capital we need.

Catch all the latest updates from the stock market here