Local governments in Korea are responsible for nearly half of the country’s total public spending, yet generate only about 20 percent of total public revenue, while the central government bridges this gap through significant transfers. How well local governments manage their resources is therefore crucial in the country’s overall fiscal performance.

The central–local fiscal relationship

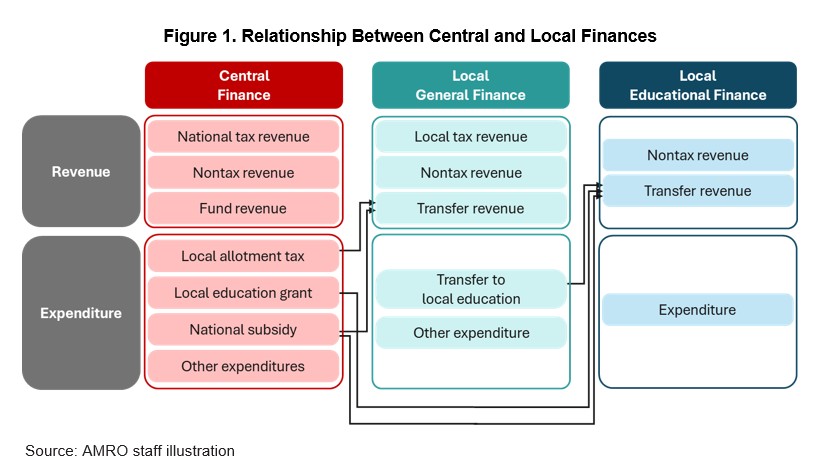

Korea’s constitution enshrines local autonomy, allowing local governments and education authorities to function independently. Nevertheless, the fiscal system remains tightly linked through four key intergovernmental transfers (Figure 1).

The local allotment tax aims to reduce regional fiscal disparities, while the local education grant ensures adequate and equitable funding nationwide. National subsidies support mandated functions and policy priorities, often requiring local matching funds. Additionally, the metropolitan and provincial governments provide education offices with funding to support local education services.

Revenue collection remains heavily centralized. The central government collects nearly 80 percent of consolidated revenue, while local authorities collect only about one-fifth. However, once transfers are allocated, local governments and education authorities together account for nearly half of consolidated public expenditure. This underscores the importance of improving the strategic resource allocation and execution of local public finances.

Resource allocation and coordination challenges

The sectoral distribution of spending broadly reflects how responsibilities are divided between the central and local governments. Most public spending areas—except for national functions such as defense, foreign affairs, unification, and communications—are shared between the central and local governments. Education, regional development, environment, and culture-related spending are largely local responsibilities, whereas science and technology, social welfare, public safety, and industrial policy are more centralized. Sectors such as transport, logistics, and agriculture are jointly financed and implemented.

Uncertainty in cost-sharing for national subsidy projects remains a persistent challenge. While local governments are often expected to share costs, few projects have legally prescribed matching rates. Most ratios are negotiated annually during the budget process, reducing transparency and predictability and complicating medium-term planning at the local level.

Structural constraints in local fiscal planning

The budget process of local governments generally mirrors that of the central government, but operates on a shorter timeline. While the central budget process involves several months of review and parliamentary deliberation, local governments typically compress all stages within a month.

This abbreviated timeline largely reflects local governments’ heavy reliance on central transfers; local budgets cannot be finalized until transfers are confirmed, often delaying approval beyond the start of the fiscal year. Consequently, some local bodies operate under provisional budgets.

Frequent supplementary budgets are common. Timing mismatches between central and local budget cycles often lead to repeated adjustments after transfer amounts are finalized. Delays in approval of the central government budget add further uncertainty. While these adjustments offer flexibility, their repeated use weakens the credibility of the original plan and may undermine spending discipline.

Weaknesses in local budget execution

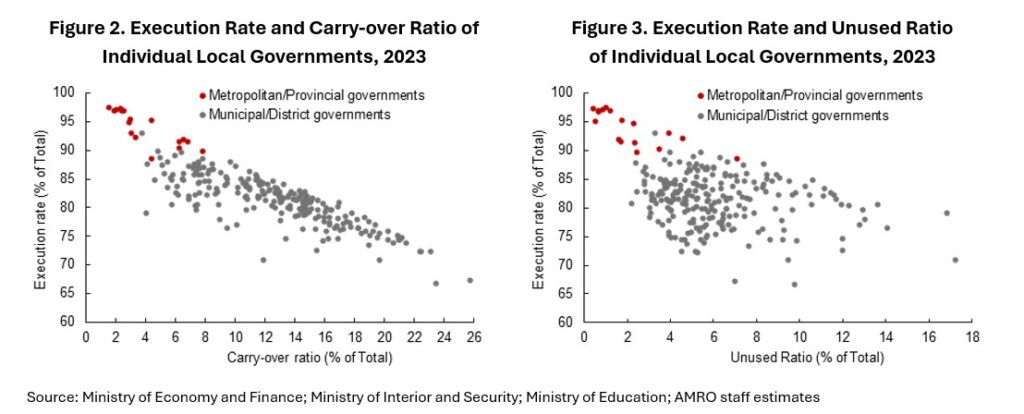

Local governments consistently trail the central government in budget execution rates, with sizeable carryovers and unused appropriations, particularly among municipal and district governments (Figures 2 and 3). Execution performance varies widely, reflecting differences in administrative and implementation capacity.

Planning and project management weaknesses further depress execution rates. Budgets are sometimes appropriated before pre-implementation procedures are completed, delaying project initiation and increasing carryovers. In other cases, full appropriations are made upfront for multi-stage projects, creating a mismatch between budget allocations and implementation capacity.

These weaknesses reduce the effectiveness and efficiency of fiscal policy by delaying spending and weakening the link between budget planning and project delivery.

Policy priorities

Improving local public financial management in Korea requires action on three main fronts:

1. Increase transparency and predictability in intergovernmental fiscal relations. Clearer cost-sharing arrangements for national subsidy projects, along with a more clearly defined division of responsibilities between central and local governments, would enhance accountability and efficiency.

2. Better synchronize central and local budgeting processes. Earlier communication of preliminary transfer estimates would improve planning certainty, reduce delays in local budget approvals, and lessen reliance on supplementary budgets.

3. Strengthen local planning and implementation capacity, particularly at the municipal and district levels. Enhanced performance management, together with stronger expertise in project appraisal, procurement, and execution management, would improve budget execution and the effectiveness of local fiscal spending.

As local governments play a pivotal role in public expenditure, strengthening their public financial management is essential to improving Korea’s overall fiscal performance, enhancing public service delivery, and supporting balanced and sustainable growth.