Key Takeaways

- Voya Financial introduced alternative fixed income and equity CITs for DC retirement plans.

- New CITs use a multi-manager structure to broaden alternative exposure and diversify risk.

- Voya Financial sees the products supporting AUM growth and a higher-margin business mix.

Voya Financial, Inc.’s (VOYA – Free Report) asset management business, Voya Investment Management (Voya IM), introduced two new multi-manager alternative collective investment trusts (CITs) for defined-contribution (DC) retirement plans. The newly launched CITs, namely, V-ALT Multi-Manager Alternative Fixed Income and V-ALT Multi-Manager Alternative Equity, are designed to bring alternative investments into retirement plans through a structure that combines multiple specialized managers within a single vehicle.

A notable feature of the launch is the separation of investment advisory and fiduciary responsibilities. Voya IM acts as the non-discretionary adviser, providing manager research, portfolio design and allocation recommendations. Global Trust Company serves as trustee and discretionary manager, retaining authority over implementation and manager changes. This structure is intended to strengthen fiduciary oversight and governance for DC plans.

The launch extends Voya’s long-standing multi-manager investment approach. The firm has previously used multi-manager frameworks in target-date and multi-asset solutions, and these alternative CITs represent an effort to expand private-market and alternative exposure within workplace retirement plans.

The launch of Voya IM’s new multi-manager alternative CITs is important not only as a new product offering but also as a potential growth driver for the broader business. The new V-ALT Multi-Manager Alternative Fixed Income and Alternative Equity CITs give Voya access to the rapidly growing demand for alternative investments within defined-contribution retirement plans. As plan sponsors allocate a portion of retirement assets to these strategies, Voya can gather additional assets under management. By expanding its alternatives lineup, Voya can improve revenue yields on managed assets and reduce dependence on lower-margin traditional products. Most defined-contribution plans still offer predominantly public equity and bond funds. The new CITs provide exposure to alternative strategies through a diversified multi-manager structure, which Voya believes can reduce manager concentration risk and improve outcome consistency. This helps Voya differentiate itself from competitors in the retirement-plan space and position the firm as an innovator in workplace investing.

The products will support Voya’s long-term strategy of building a more diversified, higher-margin asset management business. Over time, successful adoption could become a meaningful contributor to earnings growth and valuation expansion.

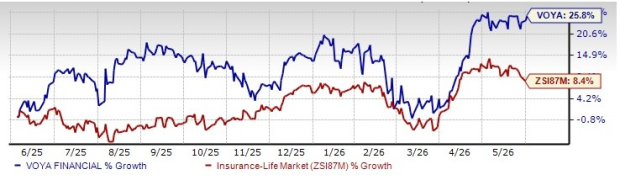

Voya’s Zacks Rank & Price Performance

Shares of this Zacks Rank #3 (Hold) life insurer have gained 25.8% in the past year, outperforming the industry’s growth of 8.4%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks from the insurance industry are First American Financial Corporation (FAF – Free Report) , Universal Insurance Holdings Inc. (UVE – Free Report) , and HCI Group, Inc. (HCI – Free Report) , each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

First American has a solid track record of beating earnings estimates in each of the trailing four quarters, with an average being 22.01%. In the past year, shares of FAF have risen 16.8%.

The Zacks Consensus Estimate for FAF’s 2026 earnings implies year-over-year growth of 12.5%, from the consensus estimate of the corresponding year.

Universal Insurance has a solid track record of beating earnings estimates in each of the trailing four quarters, with an average being 36.8%. In the past year, shares of UVE have risen 31.6%.

The Zacks Consensus Estimate for UVE’s 2026 earnings implies a year-over-year decline of 25.3%, from the consensus estimate of the corresponding year.

HCI Group has a solid track record of beating earnings estimates in each of the trailing four quarters, with an average being 42.95%. In the past year, shares of HCI have lost 8%.

The Zacks Consensus Estimate for HCI’s 2026 earnings implies a year-over-year decline of 21.5%, from the consensus estimate of the corresponding year.