Table of Contents

- Summary of Full Text

- 1. Core Judgment: LTA is not a Footnote to Price Increases, but the Primary Variable in the Valuation Framework

- 2. JPM’s LTA Analysis: Advance Payments Are the Key Difference This Cycle

- 3. Wafer Shortages: The Bottleneck for AI Server-Grade DRAM Can’t Be Fixed in One or Two Quarters

- 4. Nomura’s Demand Multiplier vs. JPM’s Contractualization: Slope vs. Sustainability

- 5. Company Ranking: Only Those Who Can Turn Shortages into Contracts Will See Valuation Rewrites

- 6. Why This Is Not “Yet Another Nomura Memory Report”

- 7. Counterpoint: Until LTA Becomes Binding, the End of the Cycle Cannot Be Declared

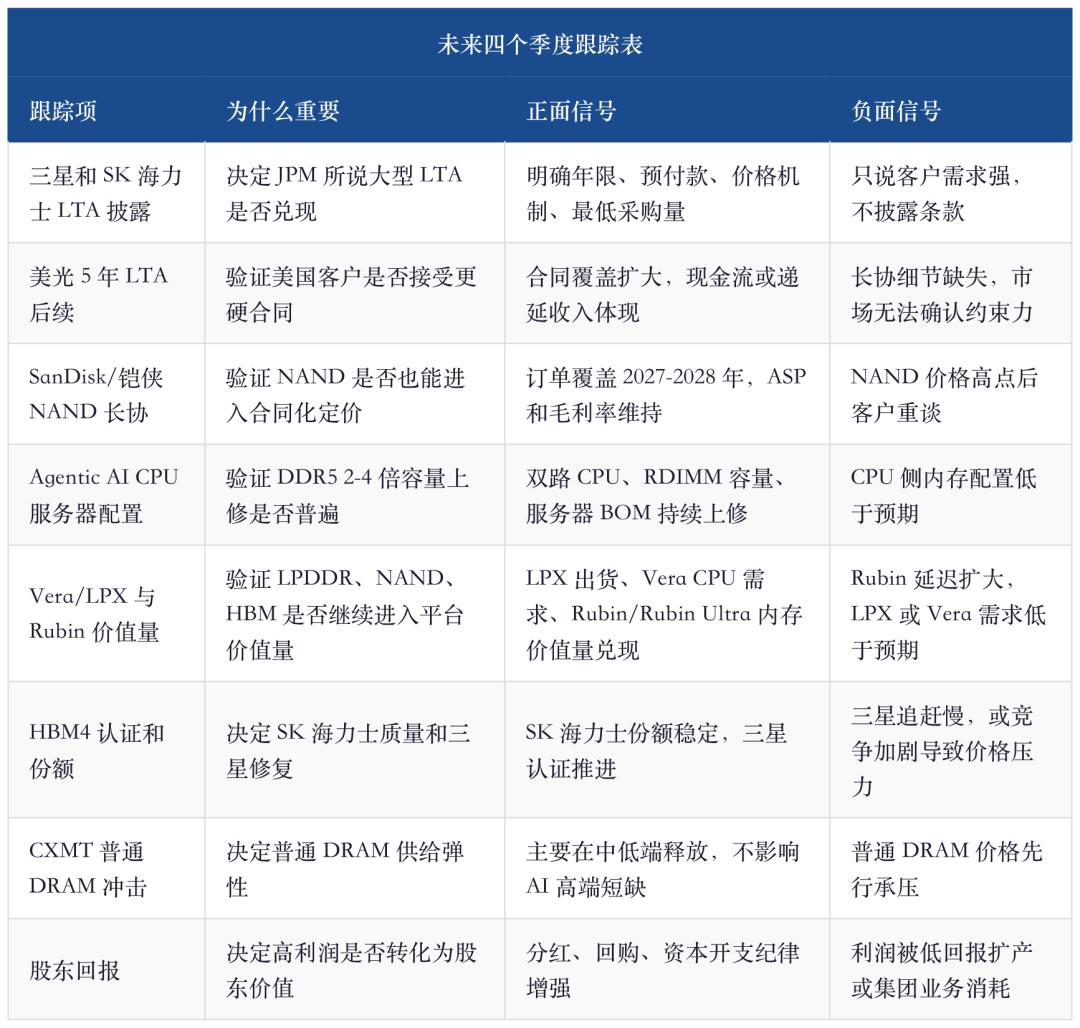

- 8. Monitoring Framework for the Next Four Quarters

- 9. Conclusion: The Second Half of the Storage Cycle is about Contract Strength, Not Just Price Slope

- Sources

Storage Is No Longer Just a Cyclical Stock: JPM LTA Dissection, Agentic AI Memory Leverage, and Samsung/SK Hynix Valuation Repricing

The key to this round of storage rally has shifted from “how much prices will rise” to “whether price increases can be contractualized.” JPM’s new report breaks LTA down into advance payments, fixed and floating pricing, take-or-pay, third-party guarantees, and capex support—providing a checklist for shifting storage stocks from cyclical assets to cash flow assets.

Summary of Full Text

The core conclusion of this report is: AI storage is transitioning from a “price surge cycle caused by supply-demand tightness” to a “valuation framework migration caused by long-term contract-based (LTA) supply lock-in.” Nomura addresses the demand side: why Agentic AI, RAG, long-context, and inference calls will multiply storage needs with token multiplier logic; JPM addresses the contract side: why cloud providers are willing to sign 3-5 year LTAs, advance payments, price floors, take-or-pay clauses, and guarantees to secure supply; Jukan’s recent findings revise the margins: Agentic AI CPU server DDR5 usage, Vera/LPX, Rubin/LPDDR, and mobile HBM are driving up demand from HBM to mainstream DRAM, LPDDR, and NAND. The final investment conclusions: Buy SK Hynix for highest quality cash flow, Samsung for discount recovery and HBM4 catch-up, Micron as the U.S. AI memory entry point, SanDisk and Kioxia for NAND LTA elasticity, and track CXMT as a variable for generic DRAM supply.

1. Core Judgment: LTA is not a Footnote to Price Increases, but the Primary Variable in the Valuation Framework

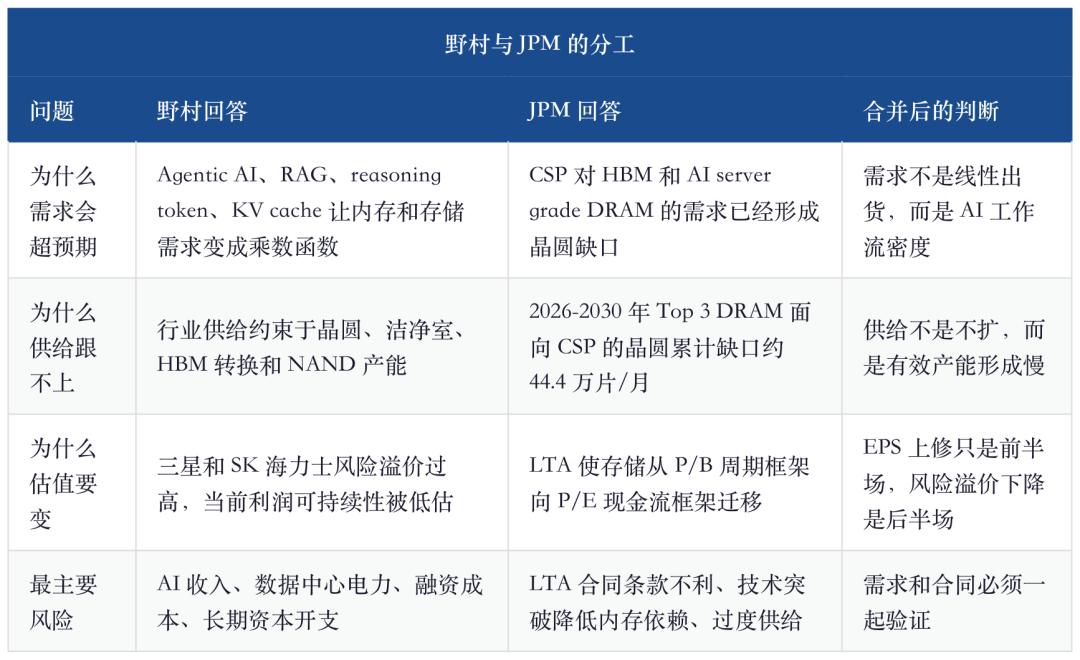

The title of JPM’s report is straightforward: detail LTA contract specifics and argue that favorable LTAs can open up new valuation frameworks for memory suppliers. Its real significance is not in re-proving DRAM, HBM, and NAND supply shortages, but in turning the industry’s most ambiguous line—“customers want long-term contracts”—into verifiable contract variables.

Historically, the market’s biggest fear with memory was profit peaks being unsustainable. The higher DRAM prices rose, the more investors worried about inventory reversal; the higher NAND margins, the more skepticism about capacity expansion; even if HBM is tight, the recurring question is “what if Nvidia changes pace?” That’s why, paradoxically, memory stocks often saw P/E fall as EPS estimates ran up, with the market assuming a cycle top.

JPM’s new angle attempts to answer “why might this time be different?” If customer commitments are only verbal, LTA is still a placebo at the cycle’s peak; if customers pay advances, accept price floors, sign take-or-pay, involve third-party guarantees, and tie capacity and order commitments together, then LTA begins to improve cash flow visibility.

“Memory is turning into a strategic asset.”

This line from JPM is the turning point of the entire report. If memory is just a commodity, fast rising prices look increasingly like cycle peaks; if it becomes a strategic asset, customers put supply certainty before price, and that’s when LTAs, prepayments, guarantees, and capex support appear. In other words, LTA isn’t a footnote to the rally—it is contract evidence of customers acknowledging prolonged shortages.

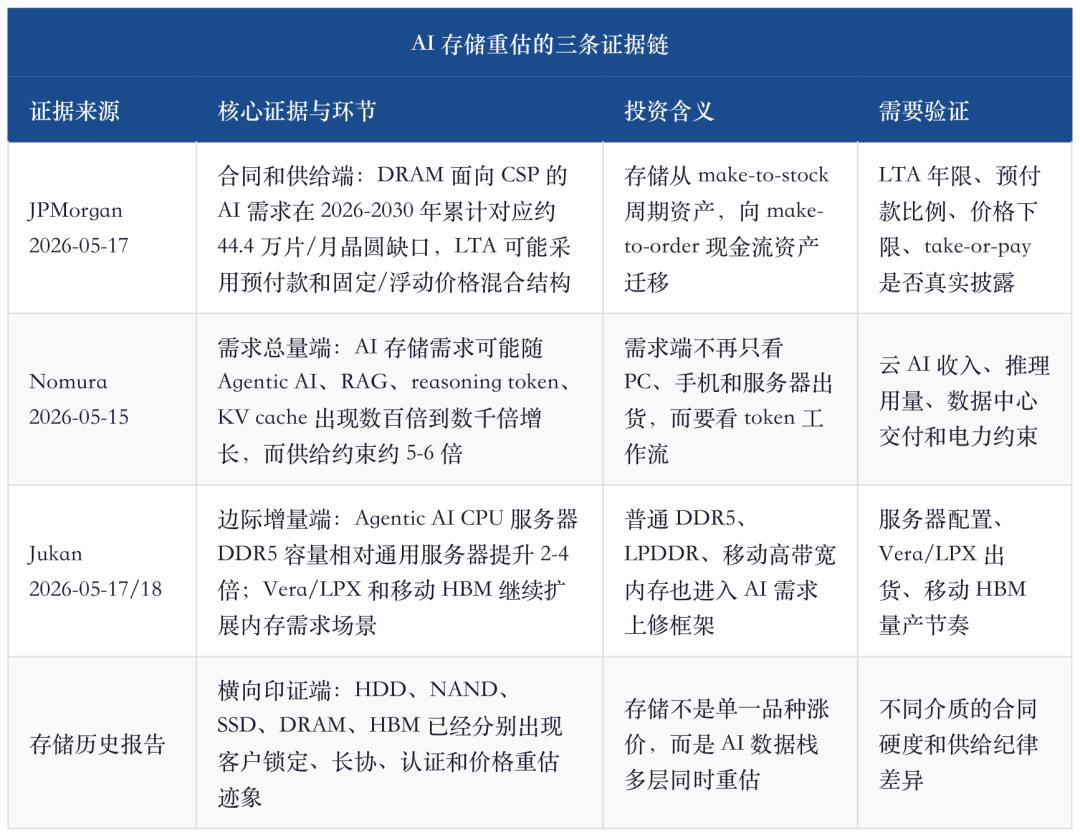

This table’s conclusion is simple: Nomura resolves “why demand may go out of control,” JPM solves “why profits may be steadier,” and Jukan provides real-time signals that models are still being revised up. Together, the narrative for storage should not be just “there will be a strong price rally in 2026,” but that “AI is rewriting storage’s demand, contracts, and valuation anchors all at the same time.”

2. JPM’s LTA Analysis: Advance Payments Are the Key Difference This Cycle

JPM notes that since 2026, LTA contracts have become one of the industry’s fiercest debates. Bulls believe LTAs improve earnings visibility, freeing memory makers from harsh cyclicality; bears doubt the contractual binding power, worrying customers will renegotiate or delay delivery whenever the cycle turns down.

The report highlights three existing cases: Micron disclosed a 5-year LTA; Nanya Technology has private placement-related LTAs; a U.S. NAND producer announced five LTAs covering over a third of its expected FY2027 bit demand. JPM also believes Samsung Electronics and SK Hynix see significant multi-year customer commitments and may disclose larger LTAs going forward.

These cases do not mean the cycle is over, but they show one thing: customers are no longer treating memory as a generic part easily replenished in the spot market. For CSPs, DRAM prices have tripled in the past year, HBM and high-end DRAM are critical to AI service quality, inference throughput, and training availability—supply risk now outweighs price risk.

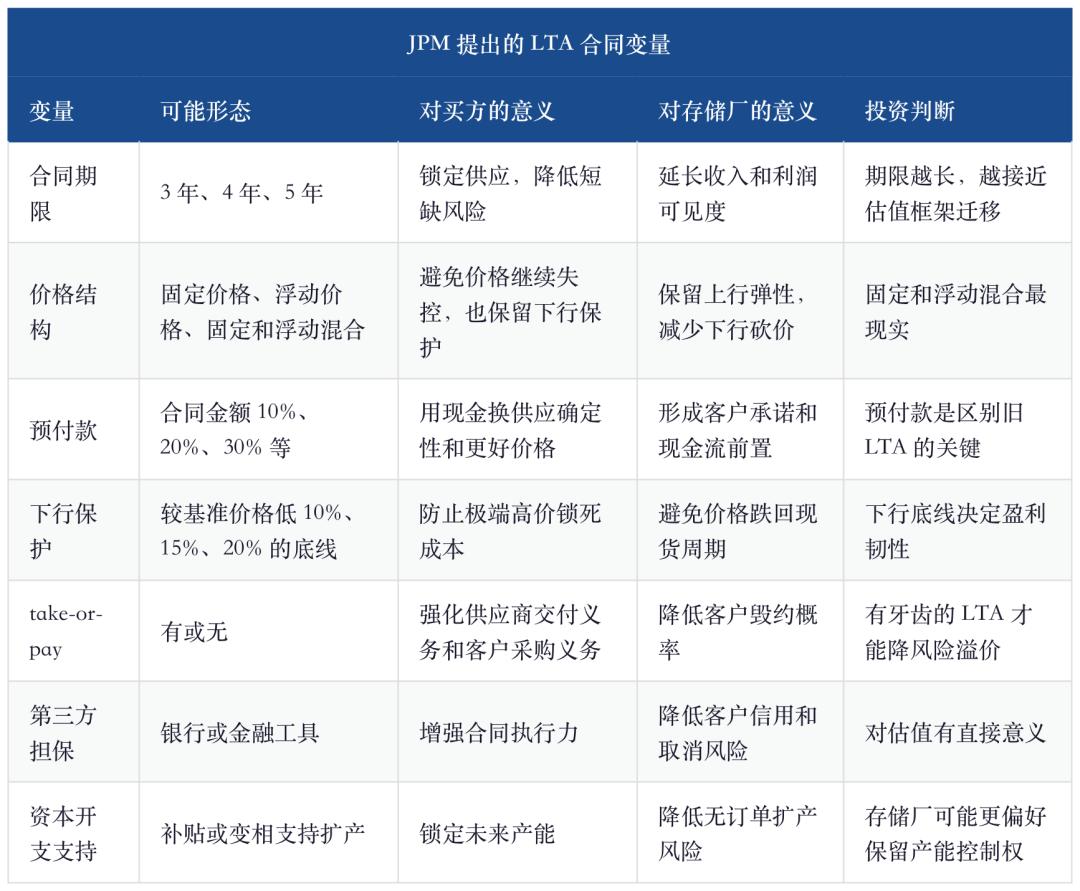

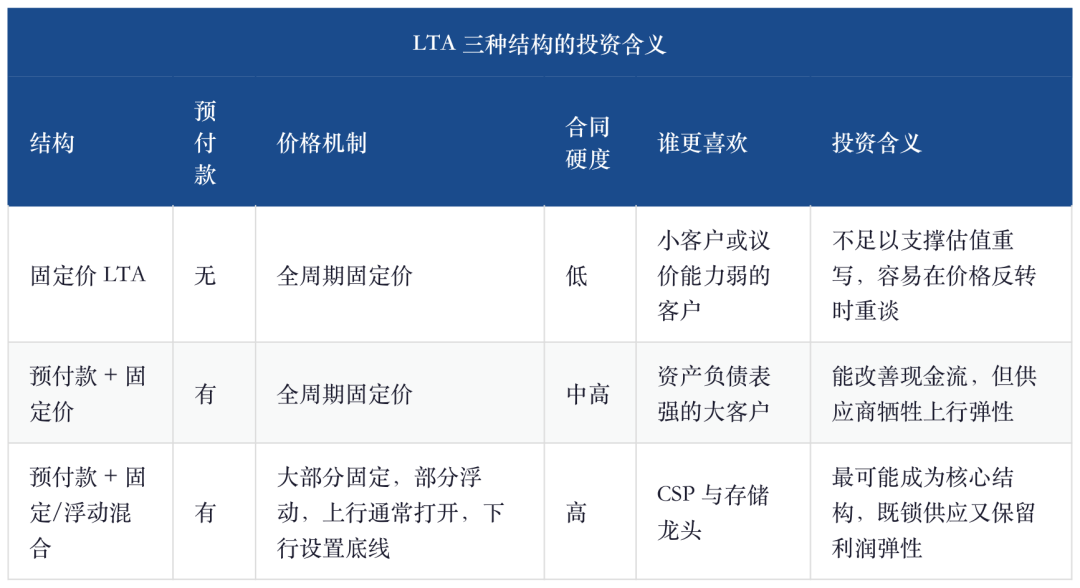

JPM’s preferred structure is not simply fixed prices. Fixed prices satisfy buyers in an upcycle, but memory suppliers are reluctant to give up price upside; in a downcycle, fixed prices make customers more eager to break contracts. The more likely structure is a combination of “advance payment + fixed quantity fixed price + partial floating quantity”: base volume provides visibility, float preserves cyclical flexibility, penalty and prepayment enhance binding force.

Here is a key judgment:LTA is not about cloud vendors getting cheaper memory, but about guaranteeing supply at all.When resources are truly scarce, price discounts come from larger guaranteed volumes and harder advance payments, not supplier concessions. For memory makers, they won’t blindly expand capacity just because an LTA is signed; JPM explicitly believes that in severe shortages, suppliers prefer high-quality contracts over unconstrained pre-expansion just for deals on expectations.

3. Wafer Shortages: The Bottleneck for AI Server-Grade DRAM Can’t Be Fixed in One or Two Quarters

The most impactful JPM chart is the back-calculation of CSP AI memory bit demand to DRAM wafer demand. The conclusion: even under aggressive capex assumptions, demand for DRAM from CSPs will cumulatively lack about 444,000 wafers/month from 2026-2030, with the supply-demand gap only gradually narrowing by 2030.

This chart’s value is not the exact wafer shortfall each year, but the point that supply constraints are continuous. DRAM capacity isn’t like software—can’t be instantly ramped with token demand. Fab construction, cleanrooms, equipment, yields, HBM conversion, advanced packaging, customer qualifications… all mean supply always lags demand.

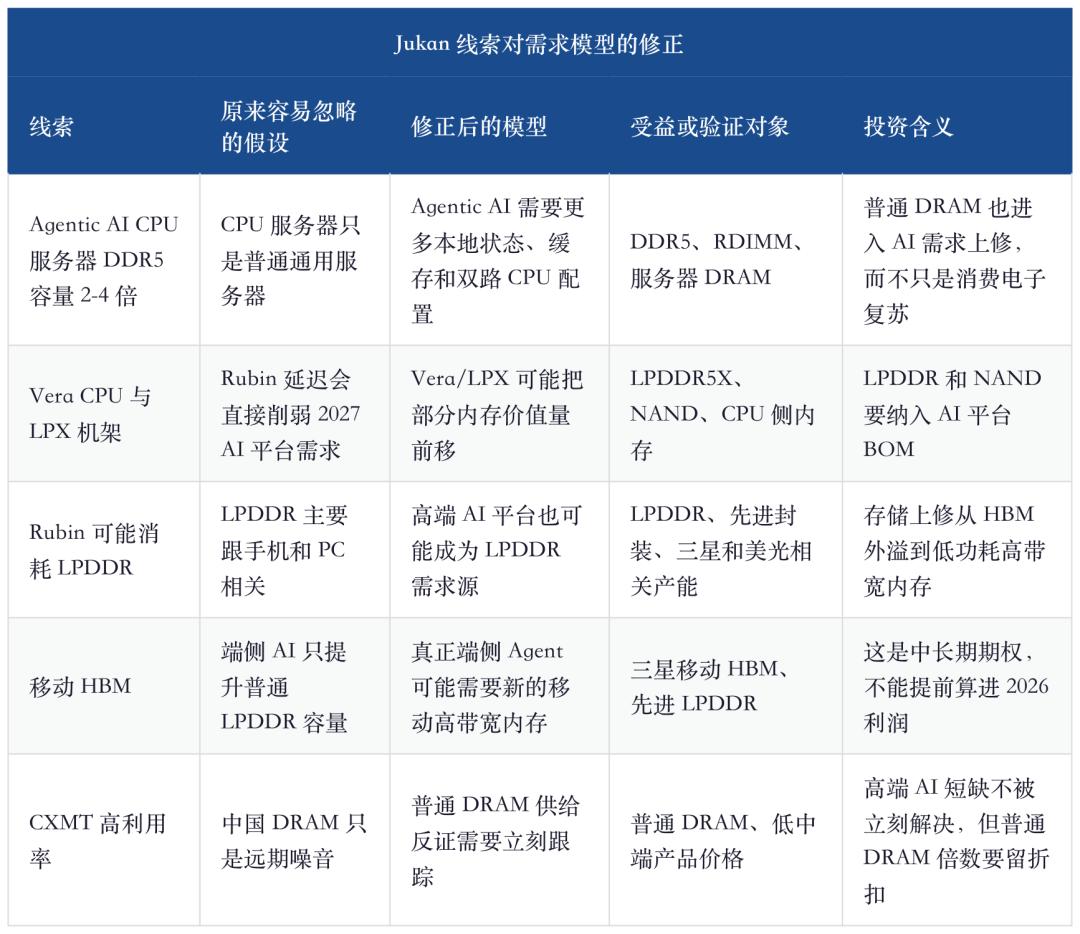

More importantly, HBM and server-grade DRAM aren’t two independent pools. HBM consumes advanced DRAM wafer and packaging capacity, and AI CPU servers increase DDR5 requirements, both squeezing available supply. Jukan (May 18, 2026) notes Agentic AI’s CPU-dedicated servers often use dual-socket configurations, with DDR5 capacity requirements 2-4x higher than generic servers. This is perfect for updating old models: previous models treated CPU server memory as standard config, but Agentic AI’s scheduling, retrieval, tool calling, and state-saving make CPU-side DRAM another bottleneck.

So, storage demand isn’t “HBM is strong, others are weak”. More accurately: HBM is the visible bottleneck, DDR5 is the hidden bottleneck being revised up by Agentic AI, and LPDDR and NAND are the next variables from new platforms and edge AI proliferation.

4. Nomura’s Demand Multiplier vs. JPM’s Contractualization: Slope vs. Sustainability

Nomura’s May 15 Global Memory report presented an aggressive demand framework: after AI shifts from training to inference, user count, time spent, task complexity, reasoning tokens, RAG calls, and Agentic AI workflows all amplify KV cache, system DRAM, HBM, SSD, and NAND demand. It even suggests AI-driven storage demand over the next five years could increase hundreds- or thousands-fold, while supply can only grow 5–6 fold.

The figure is very bullish and shouldn’t be applied mechanically, but its direction is right: demand elasticity comes from software/applications, supply elasticity from fabs and capex, and response speed is not in the same dimension.

“memory demand could rise by several thousand-fold”

This quote shouldn’t be baseline guidance, but it shows the proper research direction: don’t linearly extrapolate AI storage from PC, mobile, and traditional server shipments. The real estimates involve AI workflow density, context length, cache strategies, data retention, and model invocation frequencies. JPM’s LTA answers another question: if demand has this slope, will customers use tougher contracts to preemptively secure supply?

Here, “strong demand” and “valuation rewrite” must be separated. Strong demand only justifies EPS upgrades; only strong contracts justify lower risk premium. Many cyclical industries have seen “extremely strong demand” periods—but without contract locks, profits remain subject to cyclical discounting.

JPM compares memory to TSMC: the core is that TSMC shifted from just capital-intensive manufacturing to a P/E asset with customer preorders, process platforms, and cash flow visibility. For memory to get similar repricing, five conditions must be met: sharply reduced cyclicality, structural pricing power durability, increased LTA/HBM high-value demand share, improved capex discipline and cash returns, deepened R&D and customer joint development for differentiation.

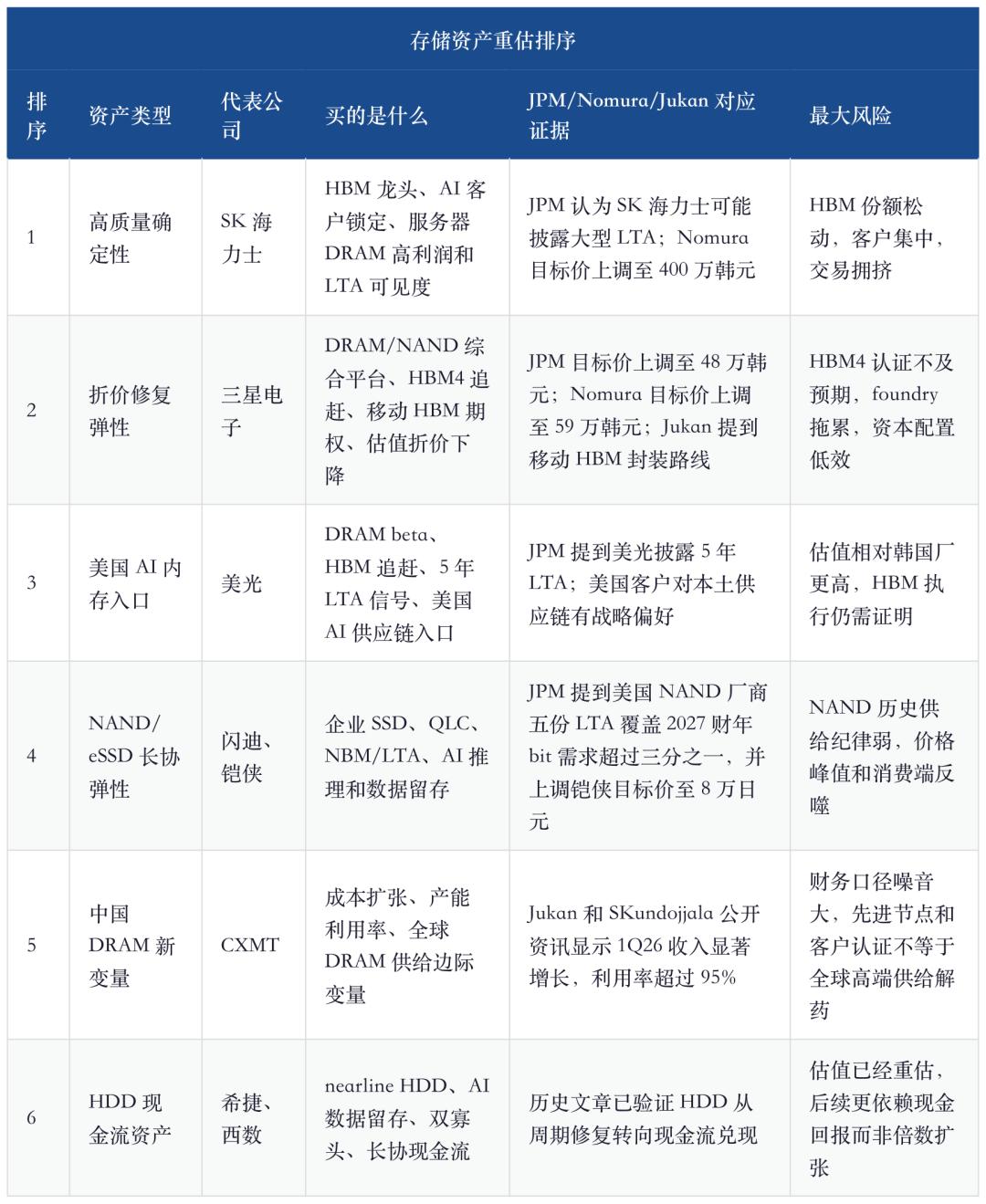

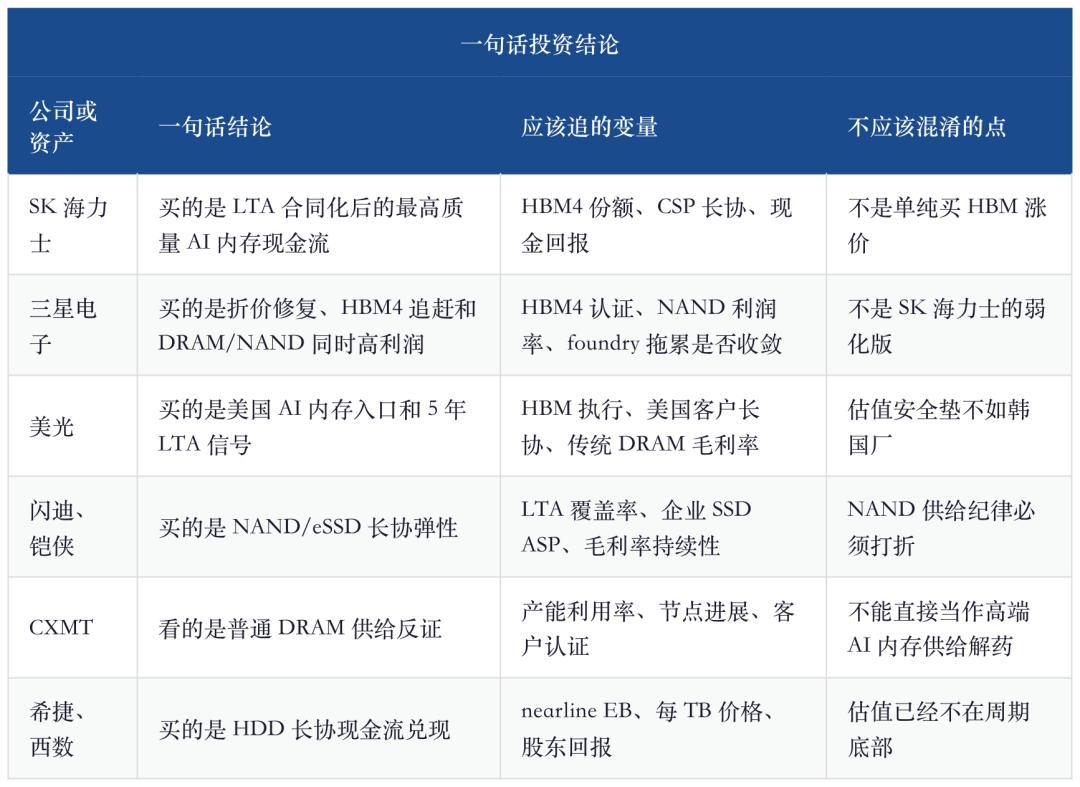

My view: Memory hasn’t fully become a TSMC-like asset, but shouldn’t be crudely regarded as the old cyclical stock, either. The right pricing method is to grant each asset a different degree of “cash flow visibility premium”—SK Hynix the highest, Samsung second, Micron with US supply chain premium, SanDisk and Kioxia needing more LTA validation in NAND, HDDs already priced for cash flows in the market.

5. Company Ranking: Only Those Who Can Turn Shortages into Contracts Will See Valuation Rewrites

You can’t treat this storage investment cycle as a basket trade anymore. AI does benefit DRAM, HBM, NAND, SSD, HDD, but contract strength, supply discipline, and valuation differ by category.

SK Hynix is still the highest-quality target. It’s not just the “HBM leader” title, but three layers: (1) HBM customer certification and yields create a clear bottleneck; (2) HBM occupies advanced DRAM capacity, which in turn supports traditional DRAM prices; (3) if major CSPs disclose LTAs, the market will be more willing to treat high ROE as sustainable cash flow.

Samsung is more complex. Nomura’s target price is more bullish; JPM also sharply raised Samsung’s target. Samsung is not a watered-down SK Hynix—it’s a value restoration story: HBM4 catch up, extended high profits for legacy DRAM/NAND, mobile HBM, improved conglomerate capital allocation—any of these will lower the risk premium. But Samsung has more variables to validate, especially HBM4 customer certification, foundry losses, and shareholder returns.

Micron is the AI memory gateway for the US, but not necessarily the cheapest asset. JPM notes Micron disclosed a 5-year LTA, which is important, showing US customers also locking in DRAM/HBM with LTAs. But Micron enjoys a US supply-chain premium over its Korean peers, so its upside depends on HBM execution, LTA terms, and a prolonged legacy DRAM cycle.

SanDisk and Kioxia represent NAND LTA elasticity. Previously, SanDisk articles described the shift from “price recovery” to “NBM and data center LTA.” JPM includes five American NAND maker LTAs in its global framework, showing NAND contractualization isn’t isolated. But historically, NAND’s weak supply discipline, strong commodity characteristics, and high price elasticity mean valuation discounts are warranted.

CXMT is a new variable to be tracked but shouldn’t be seen as a panacea for global supply. Jukan (May 17) shows CXMT’s 1Q26 revenue of $7.46bn, up 719.13% YoY, but net income is debated across reports; May 18 data says factory utilization tops 95%. This means China’s DRAM output is ramping rapidly, and the impact on generic DRAM must be tracked. But high-end AI server memory, HBM, customer certification, ecosystem security, and contract system won’t change just because one manufacturer’s revenue surges.

6. Why This Is Not “Yet Another Nomura Memory Report”

The previous Nomura report clearly outlined index-driven demand: Agentic AI turns memory demand from device shipments into a token, workflow, and data retention multiplier function. The focus then was on “why demand could be mismatched by orders of magnitude.”

This article shifts focus to “why contracts could reduce risk premiums.” Repeating “AI demand is huge, supply is slow, Samsung/SK Hynix are cheap” would just overlap. JPM’s value is breaking LTA down from a sell-side line to contractual details investors can check quarter by quarter.

So, this isn’t “JPM being bullish on memory again,” but that “the benchmarks for storage stocks in the second half of the cycle have changed.” The first half was about price and EPS, the faster the revision the better; the second half is about contracts/cash flow, the tougher the term, the higher the value.

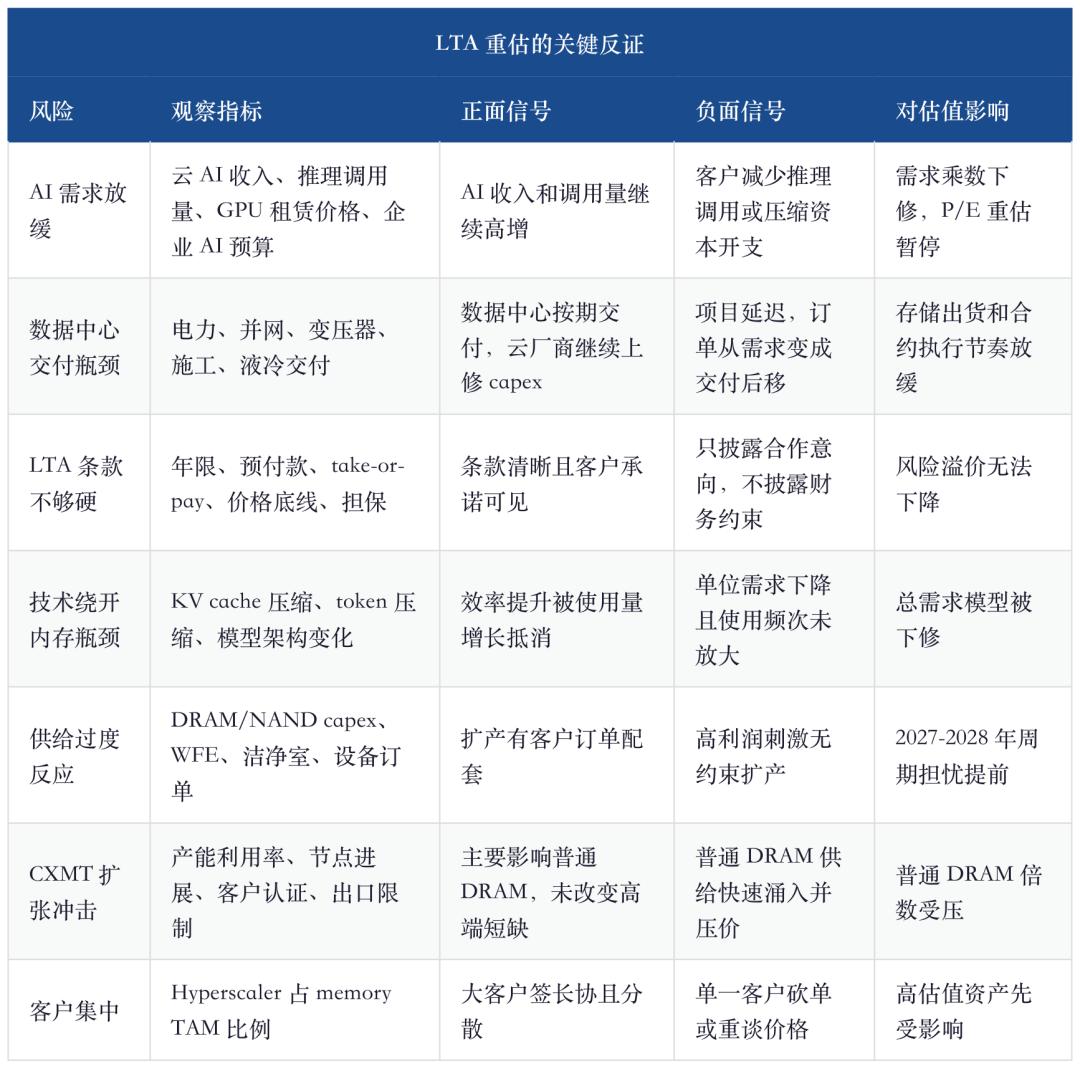

7. Counterpoint: Until LTA Becomes Binding, the End of the Cycle Cannot Be Declared

JPM isn’t mythologizing LTA as risk-free, either. The report reviews history: Post-2011-Thai-flood, large HDD LTAs helped Seagate and Western Digital shift from volatile cycles to more stable patterns; but in the 2017 DRAM shortage, forward procurement agreements didn’t hold—when demand slowed and inventory rose, DRAM prices fell over 40% within 2–3 quarters, deliveries were deferred, deals renegotiated near spot prices.

This history is crucial. It reminds us that LTA’s value is about the terms’ toughness. Without advance payments, price floors, minimum procurement, third-party guarantees, LTAs are just intent letters at the top of the cycle.

The greatest risk is a mismatch between “contract quality” and “demand realization”. Strong demand but weak contracts: you get EPS upside but no multiple expansion; strong contracts with weak demand: cash flow steady in the short term, but longer-term multiples compress. The best combination is both continuously revised-up demand and ever-tougher LTA disclosures.

8. Monitoring Framework for the Next Four Quarters

The next round of memory updates should not focus solely on contract prices. Contract price movements still matter, but JPM moves the problem up a notch: if LTA is a valuation variable, you have to track contract disclosures, advances, customer concentration, capex discipline, and cash returns.

The ideal outcome is: Samsung and SK Hynix disclose tougher LTAs in late 2026, HBM4 verification progresses, Agentic AI CPU server configs keep getting revised up, NAND/eSSD LTAs expand, and CXMT growth does not rapidly drag down high-end DRAM prices. If these all occur, the market can shift memory stocks from legacy 4–6x P/E cyclical multiples to higher cash-flow multiples.

9. Conclusion: The Second Half of the Storage Cycle is about Contract Strength, Not Just Price Slope

This JPM report makes the latter half of the memory sector’s story much clearer. Nomura’s role is to alert the market: after Agentic AI, memory demand could be scaled up by tokens, KV cache, RAG, long contexts, and data retention beyond what traditional models can explain. JPM’s role is: if demand is robust, cloud providers will lock in supply with LTA, advances, price floors, and guarantees, meaning suppliers’ profits can shift from cyclical peaks to discounted cash flows.

My conclusion has three layers.

First, keep long AI memory, but update the narrative. “DRAM/NAND/HBM are rising” alone cannot explain the second half—what matters is whether gains can be locked in as 3–5 years of visible revenue and profit via LTA.

Second, company ranking must be reordered by contract strength and technical bottlenecks. Buy SK Hynix for quality, Samsung for discount recovery, Micron for US AI entry, SanDisk/Kioxia for NAND/eSSD LTA elasticity, and watch CXMT as a supply-side tracker. All sit in this supercycle but with quite different risk/reward profiles.

Third, risk doesn’t vanish. JPM itself reminds us 2017’s DRAM long-term agreements didn’t resist the cycle reversal. Only with advances, take-or-pay, price floors, financial guarantees, and joint customer capex constraints becoming clearer, will the market truly shift memory from P/B cycle to P/E cash flow frameworks.

So, this report fits best as the “contractualization re-valuation” leg of the AI memory thesis: demand is still being revised up by Nomura and Jukan, supply by JPM’s wafer gap, and valuation by LTA clauses lowering risk premium.

The real thing to buy in the second half of the storage cycle isn’t whichever category has the highest price jump this quarter, but whoever can turn AI shortages into longer contracts, tougher customer locks, steadier cash flow, and lower risk premiums.

Sources